Is It Time To Reassess 10x Genomics (TXG) After Its 188% One Year Share Price Surge

10x Genomics TXG | 0.00 |

- If you are trying to figure out whether 10x Genomics stock is reasonably priced or stretched, the recent share moves and current valuation score give you some useful clues to start with.

- The stock last closed at US$23.98, with returns of 13.8% over the past week, a decline of 2.5% over the past month, a 44.3% gain year to date, and a 188.2% gain over the past year. Over longer periods, the stock shows declines of 54.5% over three years and 85.8% over five years.

- Recent news coverage has focused on 10x Genomics as a key player in high throughput single cell and spatial genomics tools, which has kept attention on how its technology is being adopted in research and clinical pipelines. Headlines have also highlighted ongoing interest in the broader genomics sector, giving context to the sharp share price gains over the last year and the mixed longer term returns.

- 10x Genomics currently has a value score of 3 out of 6. The next sections will walk through what different valuation methods say about the stock and why there may be an even better way to think about valuation by the end of the article.

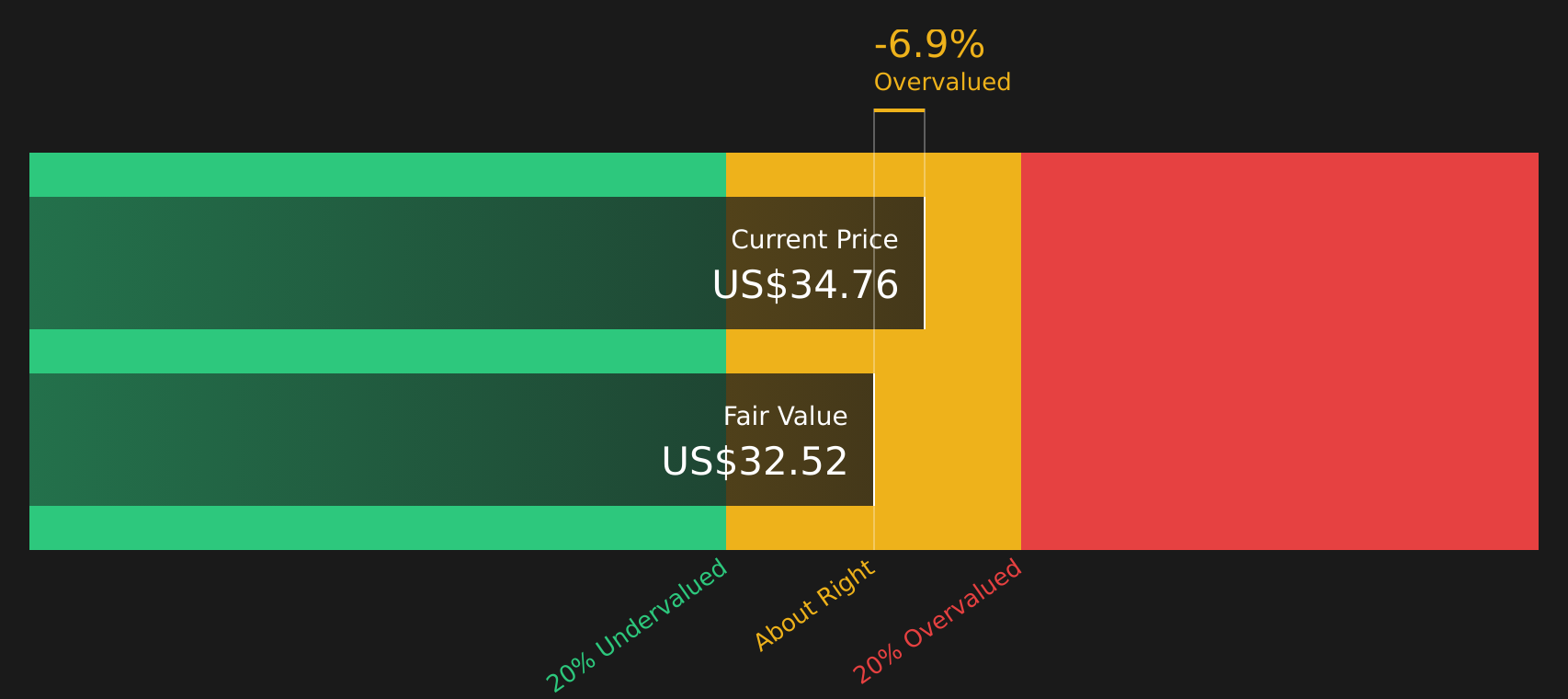

Approach 1: 10x Genomics Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and then discounting them back to today’s value using a required rate of return.

For 10x Genomics, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections rather than earnings. The latest twelve month free cash flow is reported at about US$105.54 million. Analysts provide explicit estimates through 2029, with free cash flow for that year projected at US$120 million, and Simply Wall St extrapolates further out to 2035 using gradually moderating growth assumptions.

When these projected cash flows, including US$16 million in 2026 and US$285.07 million in 2035, are discounted back to today, the model arrives at an estimated intrinsic value of about US$34.20 per share. Compared with the recent share price of US$23.98, the DCF output suggests the stock trades at roughly a 29.9% discount, indicating it screens as undervalued on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests 10x Genomics is undervalued by 29.9%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: 10x Genomics Price vs Sales

For companies where earnings are limited or volatile, the Price to Sales, or P/S, ratio is often a useful way to compare what investors are paying for each dollar of revenue. Growth expectations and risk still matter, because faster and more predictable revenue growth tends to justify a higher “normal” or “fair” multiple than slower or more uncertain growth.

10x Genomics currently trades on a P/S ratio of 4.77x. This is above the Life Sciences industry average of 3.38x, but below the peer group average of 7.70x. To add more context, Simply Wall St calculates a proprietary “Fair Ratio” of 4.49x for 10x Genomics. This is the P/S multiple that might be expected given factors such as the company’s revenue growth outlook, industry, profit margins, market cap and specific risks.

Because the Fair Ratio incorporates these company specific drivers, it can often be more informative than a simple comparison against peers or the broad industry. Relative to this 4.49x Fair Ratio, the current 4.77x P/S suggests the stock is slightly expensive on this metric.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your 10x Genomics Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as simple stories you can choose that link your view of 10x Genomics to a set of numbers, turning assumptions about future revenue, earnings and margins into a fair value that can be compared with the current share price.

On Simply Wall St, Narratives are available on the Community page and are designed so you can quickly see how a company’s story connects to a forecast and then to a fair value. The tools update automatically as new earnings, guidance or news are added, so your view does not stay static.

For 10x Genomics, for example, one investor might pick a cautious Narrative that lines up with a Fair Value of US$17.00 and modeled revenue growth of 2.7% a year. Another might align with a more optimistic Narrative that uses a Fair Value of US$32.00 and a 5.3% revenue growth rate. By comparing those Fair Values with the current share price, each investor can decide whether the stock looks expensive or cheap relative to the story they believe.

For 10x Genomics, however, we'll make it really easy for you with previews of two leading 10x Genomics Narratives:

Fair Value: US$32.00

Upside vs recent price: about 25.1% below this fair value on the bullish view

Revenue growth assumption: 5.3% a year

- Assumes faster take up of consumables and software tied to products like GEM X Flex and expanding multiomic and spatial workflows.

- Leans on quicker growth in biopharma demand, broader international uptake, and new AI supported use cases to support higher long term margins.

- Accepts higher risk from funding swings, competition, and potential market saturation, but still sees a higher fair value as reasonable if these concerns are managed.

Fair Value: US$17.00

Downside vs recent price: about 41.1% above this fair value on the bearish view

Revenue growth assumption: 2.7% a year

- Focuses on pressure from US academic and government funding, regulatory and geopolitical risks, and possible long running headwinds to genomics budgets.

- Highlights risk that high operating costs, legal expenses, and tougher competition keep margins weak even if revenue grows.

- Views the current price as demanding if instrument pricing pressure and market share risks persist, so it anchors to a lower fair value tied to more cautious earnings assumptions.

These two Narratives bracket the current analyst debate around 10x Genomics, so your job is to decide which story feels closer to how you think funding, competition, and new product adoption will play out and whether the current share price fits that view or not.

Once you are clear on which story you lean toward, you can take the next step with the full Narratives and the detailed numbers that sit behind them, rather than just relying on a single headline multiple or DCF output.Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for 10x Genomics? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.