Is It Time To Reassess Coupang (CPNG) After Its Recent Share Price Rebound?

Coupang, Inc. Class A CPNG | 0.00 |

- Wondering if Coupang at around US$20.72 is a bargain or just fairly priced? This article walks through what that number might really mean for you.

- The stock has returned 8.0% over the last 7 days and 12.3% over the last 30 days, while year to date it is at an 11.3% loss and the 1 year return sits at a 3.5% loss, compared with a 30.6% gain over 3 years and a 51.4% loss over 5 years.

- Recent headlines around Coupang have focused on its role as a major Korea based e commerce platform and how its position in online retail continues to attract attention from investors looking at growth and scale. These stories frame the share price moves as investors reassess what they are willing to pay for that exposure.

- Coupang currently has a valuation score of 4 out of 6. The next sections will compare different valuation methods and then finish with a way to think about value that goes beyond the usual ratios.

Approach 1: Coupang Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth today by projecting its future cash flows and then discounting those back to a single present value figure.

For Coupang, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month Free Cash Flow sits at about $601.3 million. Analyst and extrapolated estimates then project Free Cash Flow out to 2030, where it is expected to reach about $2.9b, with intermediate years ranging from hundreds of millions to several billions in the later stages, all discounted back to today.

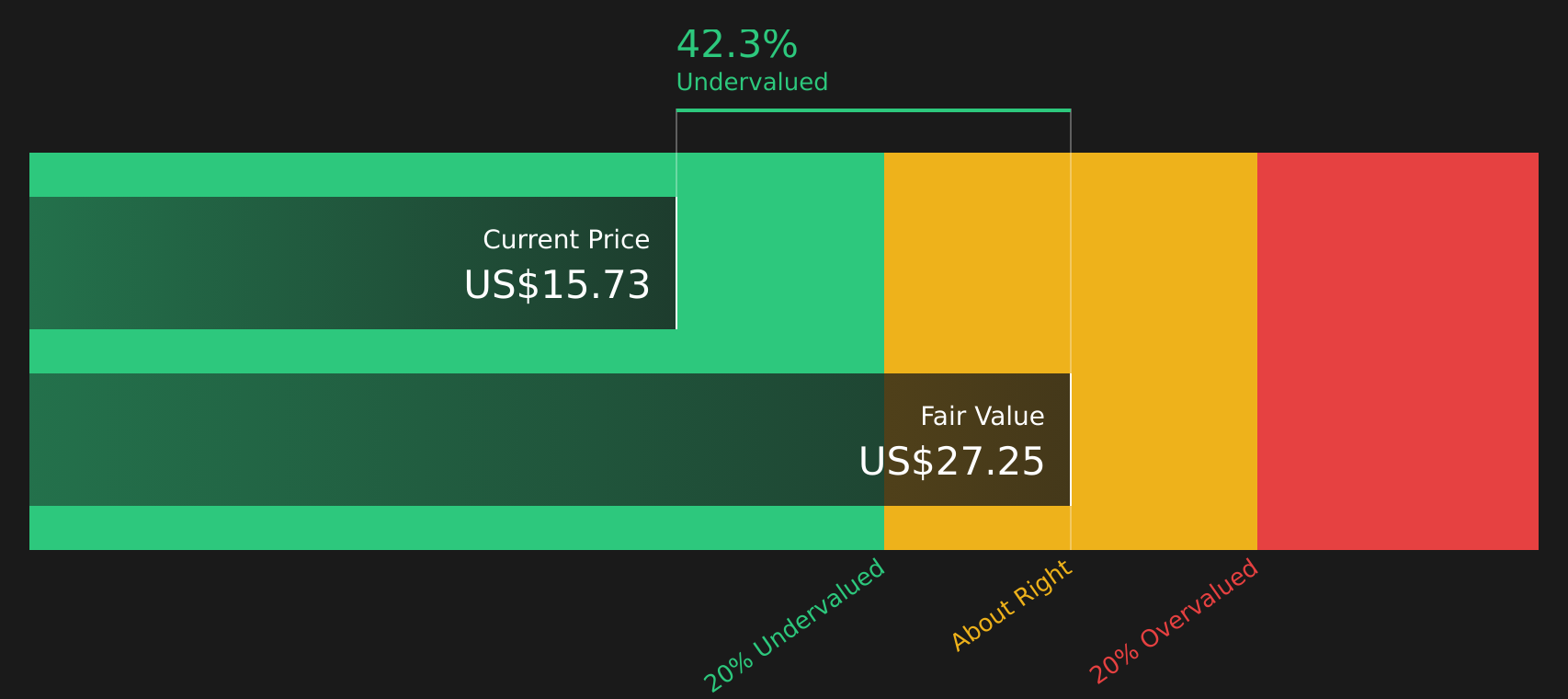

When Simply Wall St aggregates these discounted cash flows, the result is an estimated intrinsic value of about $28.85 per share. Compared with a recent share price around $20.72, the DCF suggests an intrinsic discount of roughly 28.2%, which points to Coupang trading at a meaningful gap to this modelled value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coupang is undervalued by 28.2%. Track this in your watchlist or portfolio, or discover 57 more high quality undervalued stocks.

Approach 2: Coupang Price vs Sales

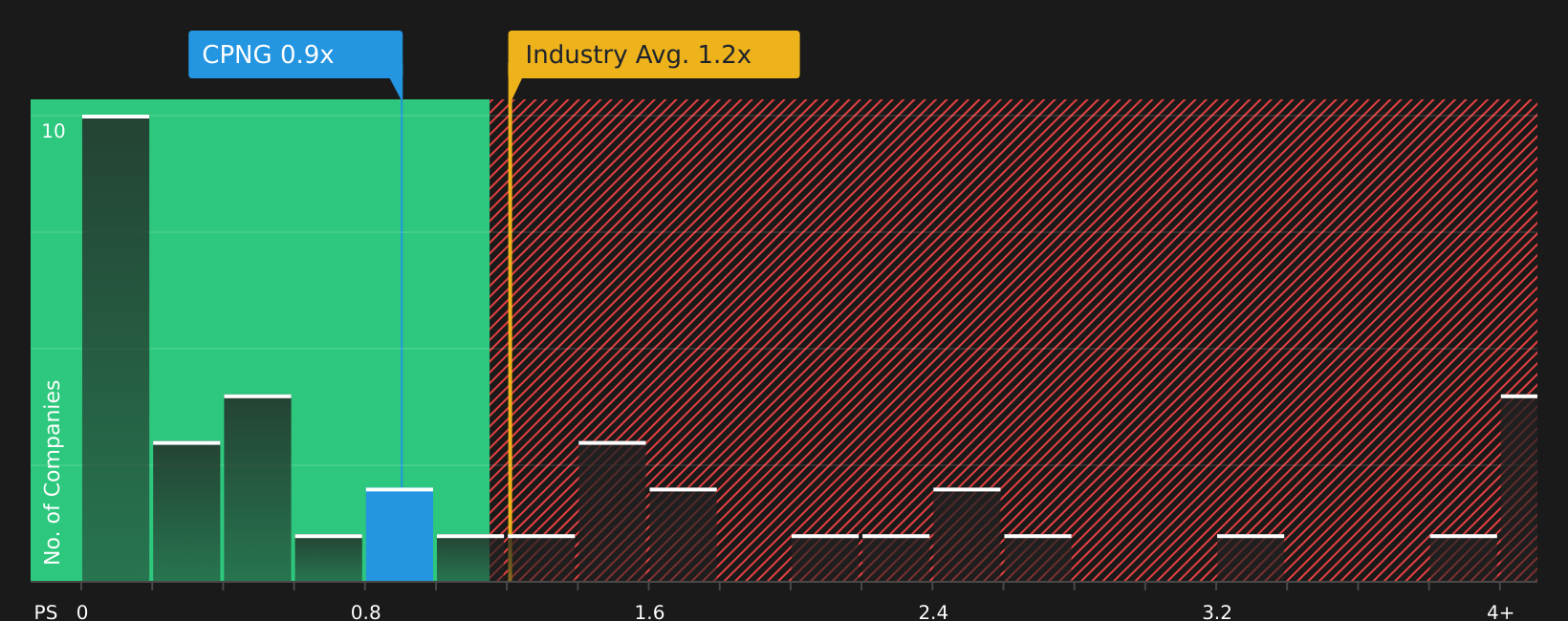

For companies where earnings can be less stable, the P/S ratio is often a useful way to judge what you are paying for each dollar of revenue. It sidesteps short term noise in profit figures and focuses on how the market values the business relative to its sales base.

Expectations for future growth and the risk around those expectations usually influence how high or low a P/S multiple investors are willing to pay. Higher expected growth or lower perceived risk can support a higher multiple, while lower growth or higher risk can justify a lower one.

Coupang currently trades on a P/S of 1.10x. This sits close to the Multiline Retail industry average of 1.07x, and below the peer group average of 2.43x. Simply Wall St’s Fair Ratio for Coupang is 1.31x, which is its proprietary estimate of what the P/S could be given factors such as revenue growth, margins, industry, market cap and risk profile.

The Fair Ratio adds context that a simple comparison with peers or the industry cannot, because it adjusts for company specific qualities rather than assuming all retailers deserve the same multiple. Comparing 1.10x with the 1.31x Fair Ratio suggests Coupang is trading below that model based reference point.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Coupang Narrative

Earlier it was mentioned that there is an even better way to think about value. Narratives are simply your own story for Coupang that links what you believe about its business to a set of revenue, earnings and margin estimates, and then to a Fair Value that you can compare with today’s price.

On Simply Wall St’s Community page, Narratives let you plug in your assumptions in an accessible way so you can see how the numbers change when you think Coupang’s e commerce position in Korea and Taiwan will be stronger or weaker. The platform then updates that Fair Value automatically whenever new news or earnings arrive.

For Coupang, for example, one investor might align with the more cautious community views that cluster around a Fair Value near US$17.01, while another might lean toward more optimistic views that sit closer to US$40.00. Seeing those different stories side by side helps you decide whether, for you, Coupang looks closer to a buy, a hold, or a sell at the current market price.

For Coupang, however, we will make it really easy for you with previews of two leading Coupang Narratives:

Fair value: US$27.27

Gap to this fair value vs the recent US$20.72 price: about 24.0% below that narrative fair value

Revenue growth assumption: 10.26% a year

- Backers of this view focus on technology-led efficiency gains in automation, AI and logistics that are expected to support margin expansion over time.

- They see rising spend per customer, new geographies such as Taiwan, and additional verticals such as FLC and Eats as important for broadening Coupang's revenue base.

- The key swing factors are how quickly early stage markets and new services reach better unit economics and how manageable regulatory and tax headwinds prove to be.

Fair value: US$17.01

Gap to this fair value vs the recent US$20.72 price: about 21.8% above that narrative fair value

Revenue growth assumption: 4.98% a year

- This camp is more wary about rising labor costs in South Korea, ongoing capital spending and tighter regulation, all of which could keep pressure on long-term margins and free cash flow.

- They expect international expansion, including Taiwan, to involve prolonged periods of weaker profitability and higher earnings volatility at group level.

- Competition from global and local e-commerce players is viewed as a risk to market share and pricing power, which feeds into a lower assumed fair value even with growth in core operations.

These two narratives sit on opposite sides of the fair value range and provide a clear set of assumptions to stress test against your own view of Coupang's data breach risks, Korea and Taiwan exposure, and long-term margin potential. If you want to see the full versions and how the numbers connect all the way through to valuation, use the Community Narratives tools to build or customize a Coupang story that fits how you see the stock today. See what the community is saying about Coupang

Do you think there's more to the story for Coupang? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.