Is It Time To Reassess Dauch (DCH) After Its Recent Share Price Swings?

Dauch Corporation DCH | 0.00 |

- If you are looking at Dauch and wondering whether the current share price reflects its true worth, you are not alone. This article will focus on what the numbers say about value rather than short term excitement.

- The stock last closed at US$7.25, with returns of 11.7% year to date and 40.8% over the past year, even though the last 7 days and 30 days saw declines of 15.9% and 5.8%.

- Those mixed returns follow recent ongoing coverage of the company, which has kept attention on how the market is reacting to its outlook and balance of risks. This backdrop helps explain why some investors are reassessing whether the recent price levels are justified.

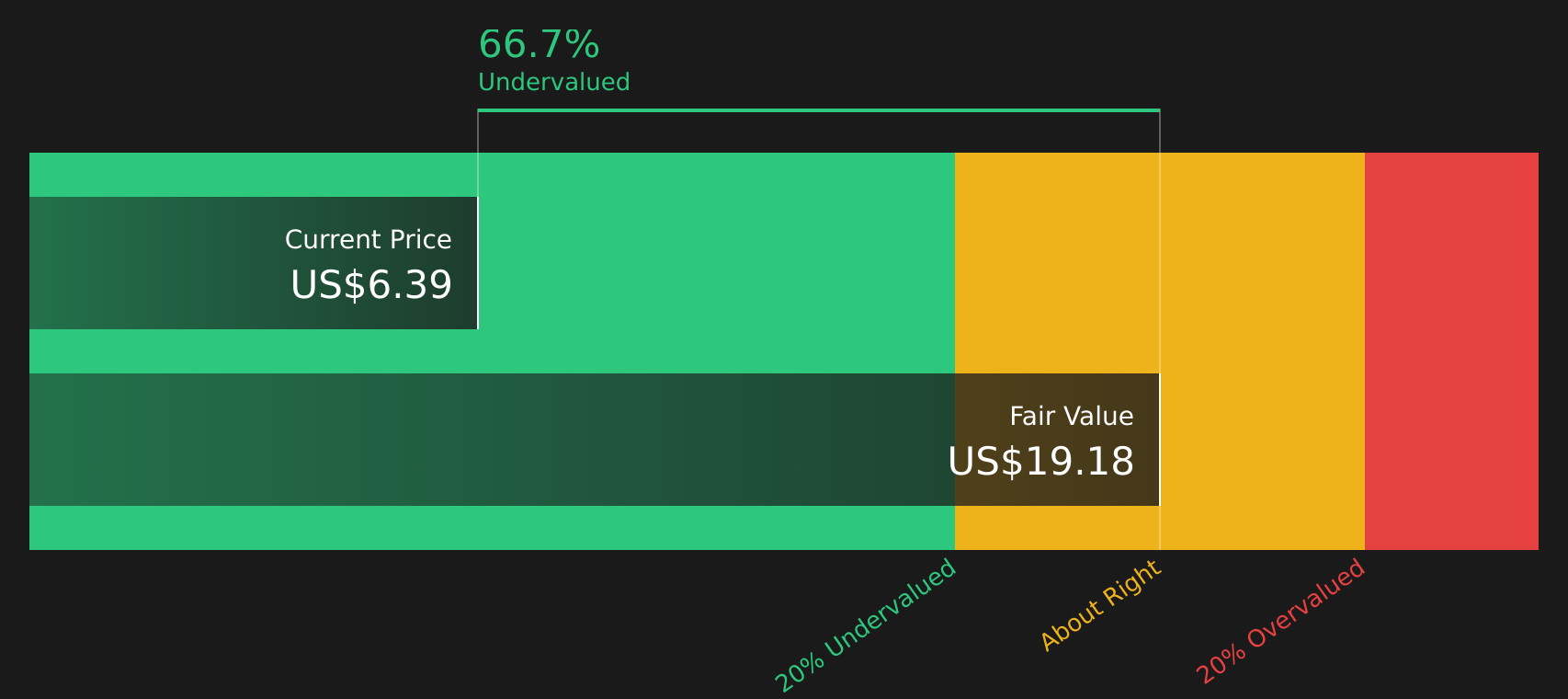

- On Simply Wall St's 6 point valuation checklist, Dauch scores a 3, reflecting that it screens as undervalued on half of the checks. Next we will walk through the main valuation methods behind that score and then finish with a more complete way to think about what the stock might be worth over time.

Approach 1: Dauch Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth by projecting its future cash flows and then discounting those back into today’s dollars using a required rate of return.

For Dauch, the model uses Free Cash Flow to Equity, which was around $183.7 million over the last twelve months, and then applies a 2 stage framework. The first stage relies on analyst estimates, with projections such as $304.05 million in 2026 and $310.03 million in 2027. Beyond that, Simply Wall St extrapolates cash flows, with projected free cash flow of $181 million in 2030. All of these figures are converted into present value using the discount rate built into the model’s assumptions.

Adding up those discounted cash flows gives an estimated intrinsic value of about US$6.82 per share, compared to the recent share price of US$7.25. That implies Dauch screens as roughly 6.2% overvalued on this DCF view, which is a relatively small gap.

Result: ABOUT RIGHT

Dauch is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

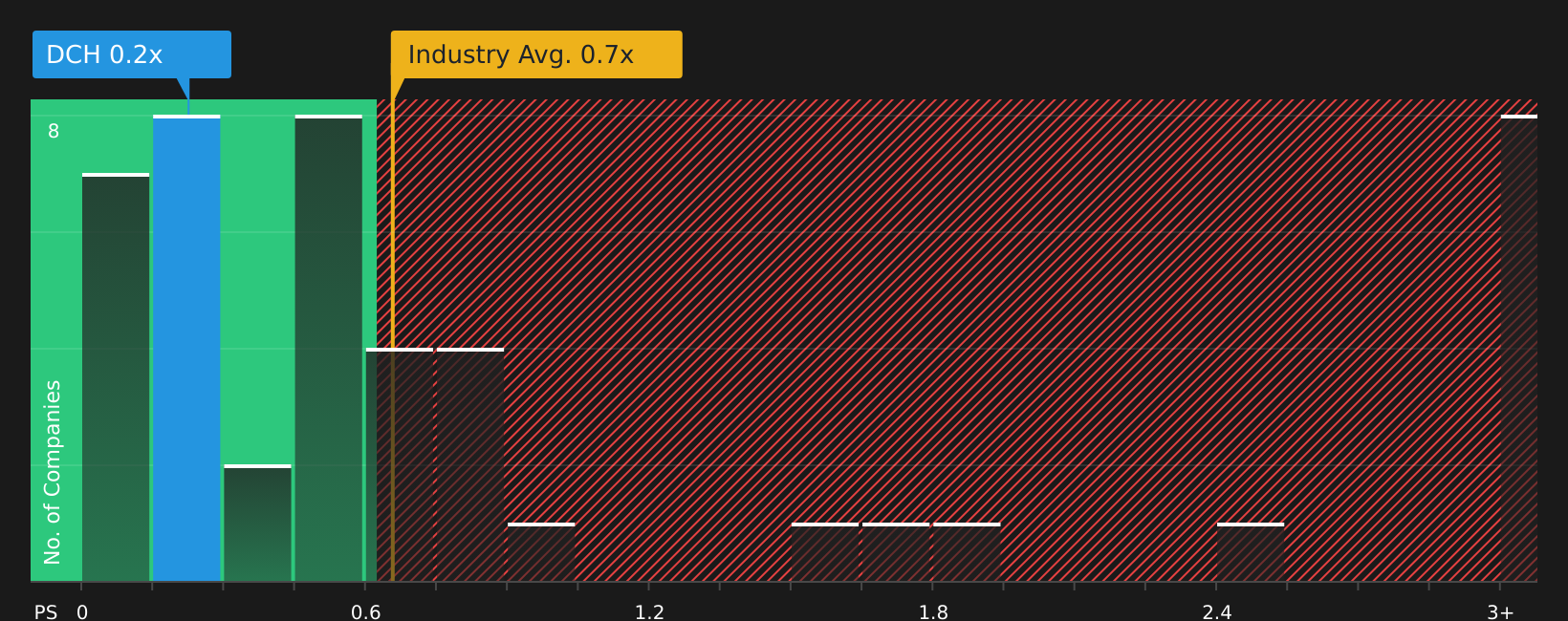

Approach 2: Dauch Price vs Sales

For Dauch, P/S is the preferred yardstick because it compares the share price to revenue, which can be useful when earnings are volatile or not the main focus. Investors usually expect faster growing and lower risk companies to justify a higher P/S multiple, while slower growth and higher risk often warrant a lower one.

Dauch currently trades on a P/S of 0.29x. That sits below the Auto Components industry average P/S of 0.83x and also below the peer average of 1.24x. On the surface, that might suggest the shares are pricing in more cautious expectations than the broader group.

Simply Wall St’s Fair Ratio for Dauch is 0.45x. This is a proprietary estimate of what a “normal” P/S could be for the company after weighing its earnings growth profile, profit margins, industry, market cap and key risks. Because it adjusts for those factors, the Fair Ratio can be more tailored than a simple comparison with peers or the industry average.

Comparing the Fair Ratio of 0.45x with the actual P/S of 0.29x, Dauch screens as undervalued on this P/S view.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Dauch Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach your own story about Dauch to the numbers by linking a view on its future revenue, earnings and margins to a financial forecast, a Fair Value, and then an explicit comparison with today’s price. Different investors in the Community page are currently sketching very different paths that range from a cautious Fair Value of about US$7.00 per share to a much higher Fair Value of roughly US$16.14. All of these update automatically as new news or earnings arrive and can help you decide whether the current price of US$7.25 lines up with the story you believe.

For Dauch, however, we will make it really easy for you with previews of two leading Dauch Narratives:

Fair value: about US$16.14 per share

Upside to this fair value: roughly 55.1% compared to the last close of US$7.25

Revenue growth assumption: 3.3% a year

- Analysts who hold this view point to recent Buy coverage, successive price target increases and supportive quarterly commentary as evidence for a higher fair value range.

- The updated model keeps the discount rate at 12.5%, while slightly lifting expected revenue growth and future P/E, and trimming the assumed net margin only modestly.

- This camp considers Dauch’s near term plans and medium term outlook strong enough to support a fair value closer to the top of recent analyst targets.

Fair value: about US$7.00 per share

Downside to this fair value: roughly 3.6% compared to the last close of US$7.25

Revenue growth assumption: 43.3% a year

- Analysts in this group recently lifted their fair value estimate to about US$7.00 after stronger Q3 results, tighter 2025 guidance and a higher required return of 12.5%.

- They still frame the shares as a Hold, citing thin projected net income, execution risk around the Dowlais combination and sensitivity to cyclical demand.

- The higher fair value reflects improved assumptions for revenue growth, margins and future P/E, while noting that much of this improvement could already be reflected in the share price.

If you want to see how these viewpoints have been built line by line from the underlying assumptions, you can move from these previews to the full narratives and risk breakdowns on Simply Wall St, then decide which story, if either, fits your own view of Dauch.

Do you think there's more to the story for Dauch? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.