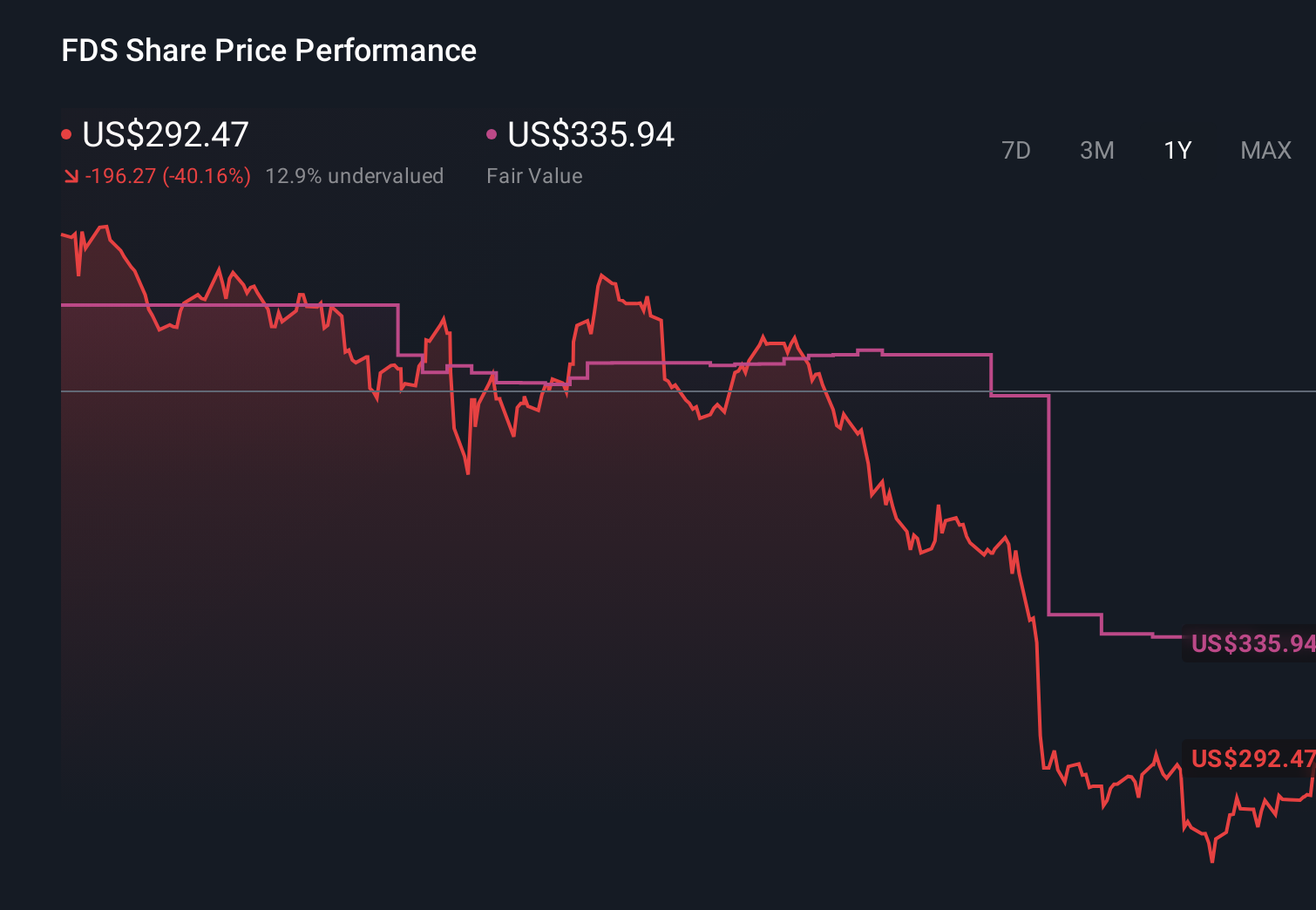

Is It Time To Reassess FactSet (FDS) After Its 36.9% One-Year Share Price Decline?

FactSet Research Systems Inc. FDS | 227.68 | +1.25% |

- If you are wondering whether FactSet Research Systems at around US$288.60 is priced fairly or not, you are not alone. This article is designed to help you make sense of that question.

- The stock has been fairly flat over the last month with a 0.0% 30-day return. However, the 1-year return of a 36.9% decline and the 5-year return of a 5.5% decline may have some investors reassessing its growth potential and risk.

- Recent share price moves sit against a backdrop of ongoing attention on financial data and analytics providers, as investors weigh how subscription-based, information-rich business models fit into their portfolios. For FactSet, that context helps explain why some investors are now revisiting whether the current share price lines up with what the underlying business could be worth.

- On our checklist-based valuation framework, FactSet scores 3 out of 6. Next, we will compare a few common valuation approaches before finishing with a more rounded way to think about what the stock might be worth in your portfolio.

Approach 1: FactSet Research Systems Excess Returns Analysis

The Excess Returns model asks a simple question: after paying shareholders a required return, how much profit is left over on each dollar of equity, and how long can that continue?

For FactSet Research Systems, the model starts with a Book Value of $58.21 per share and a Stable Book Value estimate of $67.04 per share, based on weighted future book value estimates from 6 analysts. On that equity base, the company is expected to earn Stable EPS of $19.28 per share, sourced from weighted future return on equity estimates from 4 analysts.

The implied Average Return on Equity is 28.75%, compared with a Cost of Equity of $5.66 per share. That gap produces an Excess Return of $13.61 per share, which is what this model capitalizes into today’s intrinsic value.

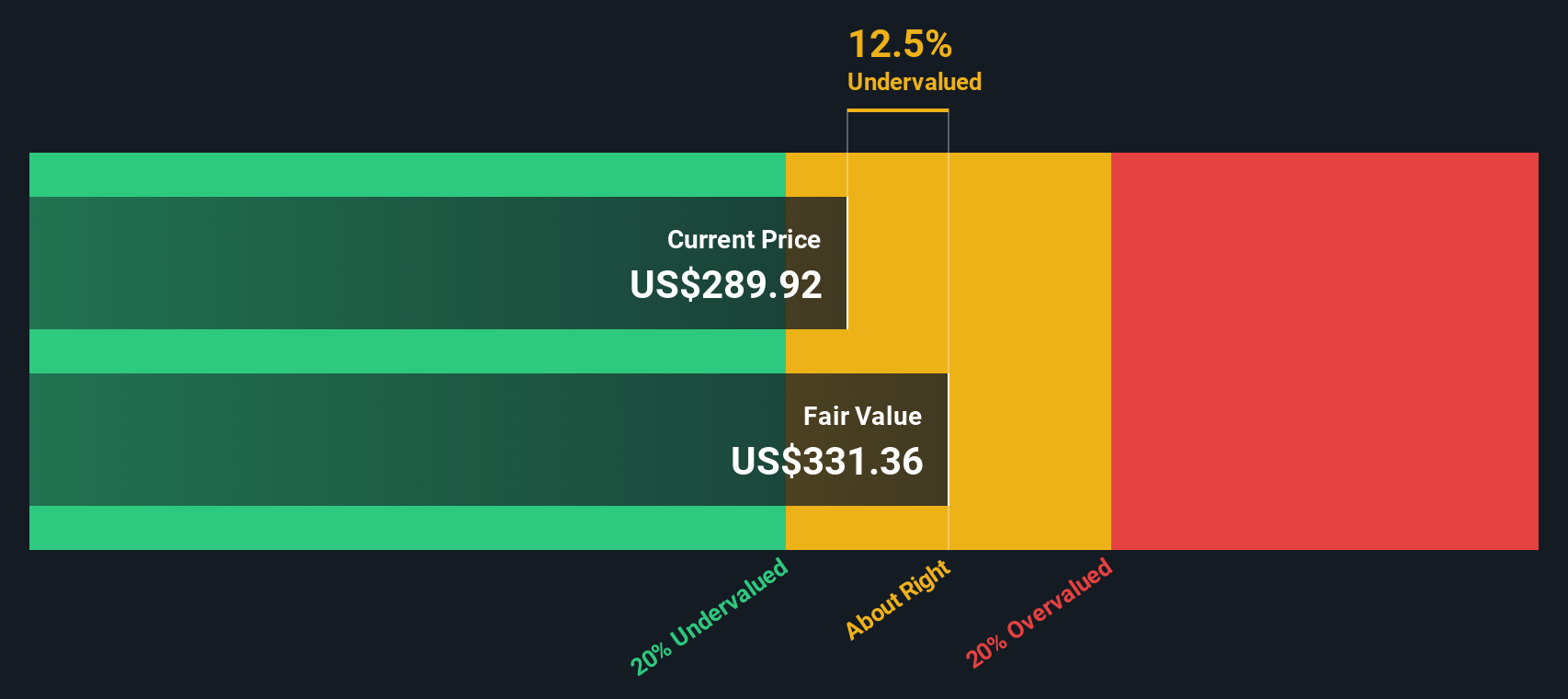

Putting it together, the Excess Returns valuation points to an intrinsic value of about $329.58 per share, compared with the current price around $288.60. Within this framework, that difference implies the shares are 12.4% undervalued.

Result: UNDERVALUED

Our Excess Returns analysis suggests FactSet Research Systems is undervalued by 12.4%. Track this in your watchlist or portfolio, or discover 871 more undervalued stocks based on cash flows.

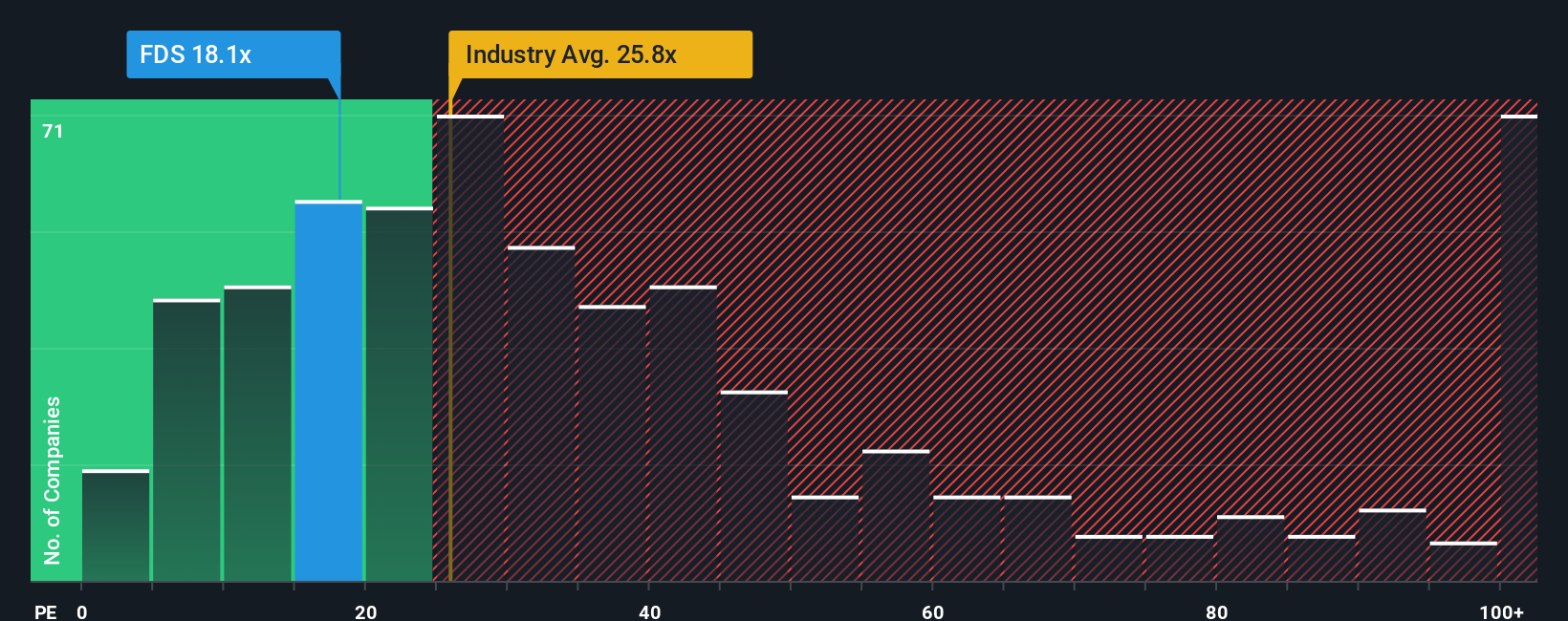

Approach 2: FactSet Research Systems Price vs Earnings

For a profitable business like FactSet Research Systems, the P/E ratio is a useful way to relate what you are paying per share to the earnings the company is generating today. It gives you a quick sense of how many dollars investors are currently willing to pay for each dollar of earnings.

What counts as a normal or fair P/E depends a lot on expectations for future earnings growth and the level of risk. Higher expected growth and lower perceived risk can justify higher P/E multiples, while slower growth or higher uncertainty typically line up with lower P/E levels.

FactSet is trading on a P/E of 17.86x. That sits below the Capital Markets industry average P/E of 25.78x and the peer group average of 29.63x. Simply Wall St’s proprietary Fair Ratio for FactSet is 14.75x, which reflects company specific factors such as earnings growth outlook, profit margins, risk profile, size and its industry.

The Fair Ratio can be more informative than a simple peer or industry comparison because it attempts to adjust for differences in growth, risk, profitability and market cap, rather than assuming all companies deserve the same multiple. Compared with FactSet’s actual P/E of 17.86x, the Fair Ratio of 14.75x suggests the shares are trading above that implied level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose Your FactSet Research Systems Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your own story about a company linked directly to your assumptions for future revenue, earnings and margins, and then turned into a fair value that you can compare with the current share price to decide whether it belongs in your buy, hold or sell bucket.

On Simply Wall St, Narratives sit inside the Community page and give you an easy way to connect what you believe about a business with a structured forecast and a fair value, without needing to build a full spreadsheet or model yourself.

Narratives are also refreshed as new information comes in, such as news, earnings or guidance updates, so your fair value view does not stay frozen while the facts are changing.

For FactSet Research Systems, one investor might focus on catalysts like GenAI products, wealth partnerships and data distribution deals and land closer to the higher analyst price target of US$500. Another investor might focus on risks such as technology costs, asset management and banking headwinds or margin pressure and sit nearer the lower target of US$355. Narratives let you see and compare both viewpoints side by side.

Do you think there's more to the story for FactSet Research Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.