Is It Time To Reassess Globus Medical (GMED) After Its Recent 1 Year Rally

Globus Medical Inc Class A GMED | 0.00 |

- Wondering if Globus Medical at around US$90.74 is priced for opportunity or already reflects the story? This article walks through the numbers so you can see how its current tag lines up with its fundamentals.

- The share price has moved by 3.9% year to date, with a 30 day return of 8.3% and a 1 year return of 25.5%, even after a recent 7 day decline of 3.3%.

- Recent coverage has focused on Globus Medical as a medical devices company in the healthcare sector and how its position in that space shapes expectations around growth, competition and capital needs. This context helps explain why the stock has seen periods of stronger momentum alongside shorter term pullbacks as sentiment adjusts.

- On Simply Wall St's valuation framework, Globus Medical records a 5 out of 6 valuation score. This sets up a closer look at how metrics like discounted cash flow, earnings multiples and asset based measures compare, before turning to an approach later in the article that can help you see valuation in an even broader way.

Approach 1: Globus Medical Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today to estimate what the business might be worth right now. It focuses on cash the company can generate for shareholders rather than just accounting earnings.

For Globus Medical, the model used is a 2 Stage Free Cash Flow to Equity approach built on cash flow projections. The latest twelve month Free Cash Flow is about $603.6 million. Simply Wall St uses analyst inputs where available, then extends them further out. For example, Free Cash Flow is projected at $536.5 million in 2026 and $677.1 million in 2027, with additional estimates carrying out to 2035, all in dollars.

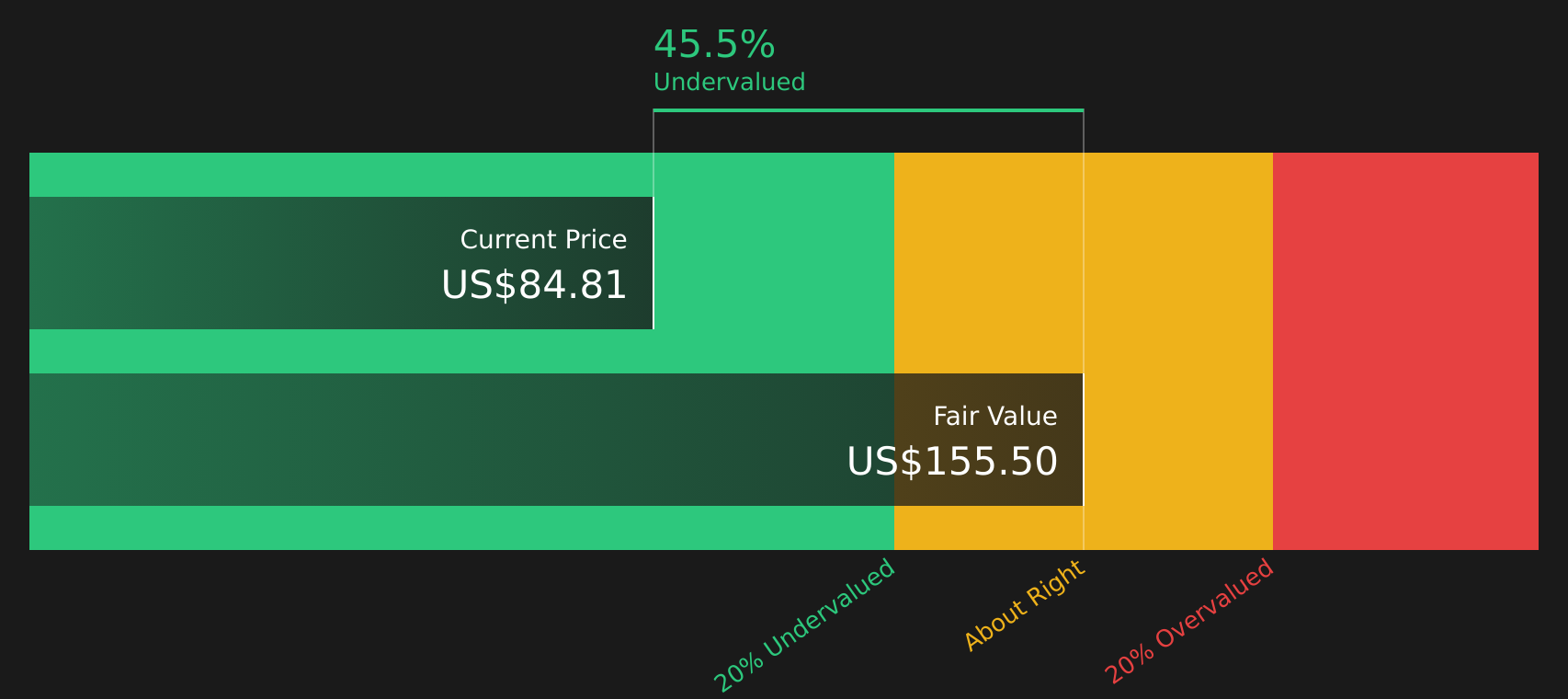

When those projected cash flows are discounted back and combined, the DCF indicates an estimated intrinsic value of about $132.19 per share. Compared with the recent share price of around $90.74, the model suggests the stock is 31.4% undervalued on this cash flow view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Globus Medical is undervalued by 31.4%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Globus Medical Price vs Earnings

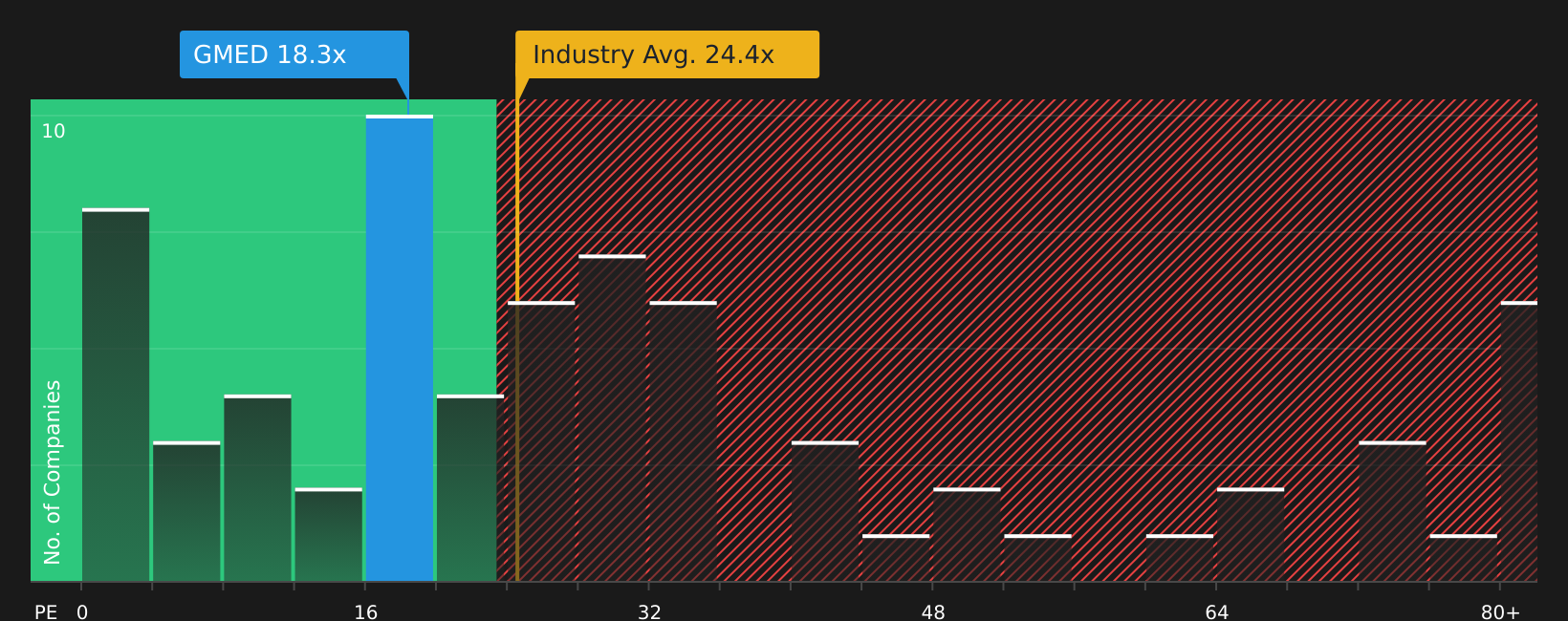

For profitable companies, the P/E ratio is a useful check because it links what you pay for the stock to the earnings the business is currently generating. Investors generally accept paying a higher P/E when they expect stronger growth and lower risk, and a lower P/E when growth expectations are modest or risks are higher.

Globus Medical trades on a P/E of 22.9x. This sits close to the Medical Equipment industry average P/E of 24.0x and is well below the peer group average of 43.0x. Simply Wall St also provides a proprietary “Fair Ratio”, which is the P/E level suggested for Globus Medical based on factors such as its earnings growth profile, profit margins, industry, market cap and risk characteristics. For Globus Medical, this Fair Ratio is 22.4x.

Compared with broad peer or industry comparisons, the Fair Ratio aims to be more tailored because it adjusts for company specific traits rather than treating all peers as equal. With the current P/E at 22.9x and the Fair Ratio at 22.4x, the stock screens as slightly more expensive than this tailored reference point, but not by a wide margin.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Globus Medical Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and on Simply Wall St that shows up as Narratives. With Narratives, you choose a story for Globus Medical, link it to specific assumptions for revenue, earnings and margins, and let the platform turn that into a Fair Value that you can compare to the current share price to help inform a buy, hold or sell decision. Narratives sit inside the Community page and are designed to be easy to use. You can select or edit assumptions instead of building a spreadsheet, and the Fair Value updates automatically when new data such as results or news are added. For Globus Medical, one investor might align with a higher Fair Value of US$123.00 with assumptions like earnings of US$632.9m and a P/E of 32.9x by 2029. Another might lean toward a lower Fair Value of US$90.00 with assumptions closer to earnings of US$462.2m and a P/E of 22.8x by 2028. Both viewpoints are visible side by side so you can decide which story feels closer to how you see the company.

For Globus Medical however we will make it really easy for you with previews of two leading Globus Medical Narratives:

Fair Value: US$123.00

Upside vs last close: 26.3%

Revenue growth assumption: 8.6%

- Analysts in this camp focus on margin progress, especially from cost actions, manufacturing automation and NuVasive and Nevro integration, as a key driver for higher earnings power.

- They see strong potential in technologies such as the Excelsius ecosystem and XR headset alongside global demand for musculoskeletal care and international expansion to support higher revenue.

- This view lines up with a Fair Value at the upper end of analyst targets and assumes a higher future P/E than the current US Medical Equipment industry level, so the bar for execution is set fairly high.

Fair Value: US$90.00

Downside vs last close: 0.8% overvalued

Revenue growth assumption: 6.9%

- Analysts here focus on integration complexity, supply chain issues and extended sales cycles as factors that could weigh on both revenue consistency and margin progress.

- They highlight pricing pressure, value based care and reliance on surgical volumes as risks that could limit long term revenue expansion and profitability, even if headline growth remains solid.

- This view anchors to the lowest analyst Fair Value in the range and assumes a more moderate future P/E, reflecting caution around execution and competitive pressure.

If you want to see these stories with full earnings, margin and valuation paths laid out for you, move from reading about narratives to testing them against your own expectations with the Community tools on Simply Wall St.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Globus Medical on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Globus Medical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.