Is It Time To Reassess Intuitive Surgical (ISRG) After Recent Share Price Weakness?

Intuitive Surgical, Inc. ISRG | 452.07 | -2.67% |

- If you are wondering whether Intuitive Surgical's current share price still reflects good value, you are not alone. This is especially relevant given how closely watched this stock is in the medical devices space.

- The shares last closed at US$527.44, with returns of a 6.1% decline over 7 days, a 7.9% decline over 30 days, a 6.1% decline year to date, a 12.7% decline over 1 year, and gains of 104.5% over 3 years and 105.6% over 5 years.

- Recent market attention on Intuitive Surgical has been shaped by ongoing coverage of its role in robotic assisted surgery and by how investors weigh expectations for future procedure volumes against current pricing of the stock. News around broader interest in medical technology names and the competitive backdrop in surgical robotics has also kept sentiment and valuation debates active.

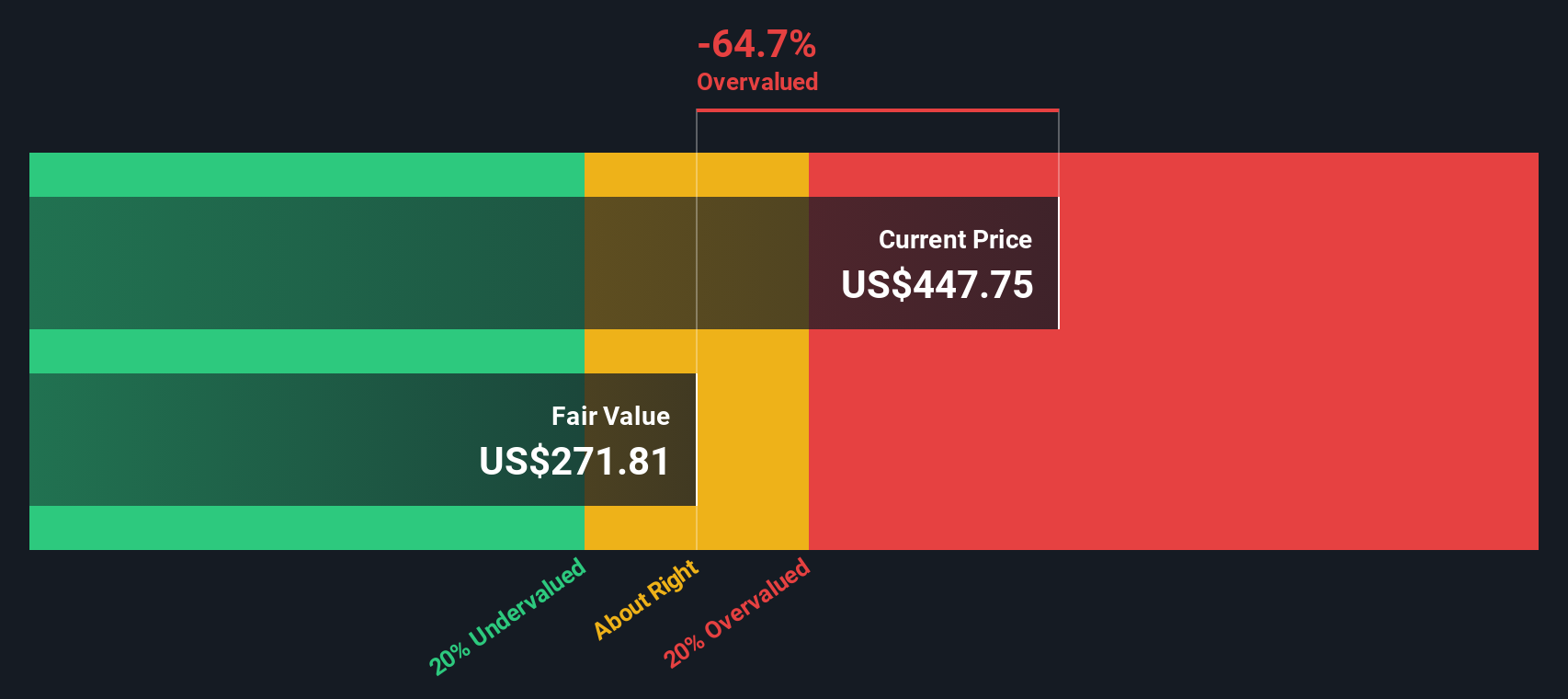

- On our valuation checks, Intuitive Surgical scores 0 out of 6 on perceived undervaluation. You can see the breakdown in this valuation summary, which we will unpack next using several methods before finishing with a different way of thinking about what the market might be pricing in.

Intuitive Surgical scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Intuitive Surgical Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today to estimate what the business could be worth right now.

For Intuitive Surgical, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow is about $1.90b. Analyst inputs and extrapolated estimates point to projected free cash flow of $5.87b by 2030, with interim projections between 2026 and 2035 ranging from roughly $3.73b to $7.70b before discounting.

When these projected cash flows are discounted back to today, Simply Wall St’s DCF model arrives at an intrinsic value of about $352.31 per share. Against the recent share price of $527.44, this implies the stock is around 49.7% above the DCF estimate, so on this cash flow view the shares screen as overvalued rather than cheap.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Intuitive Surgical may be overvalued by 49.7%. Discover 872 undervalued stocks or create your own screener to find better value opportunities.

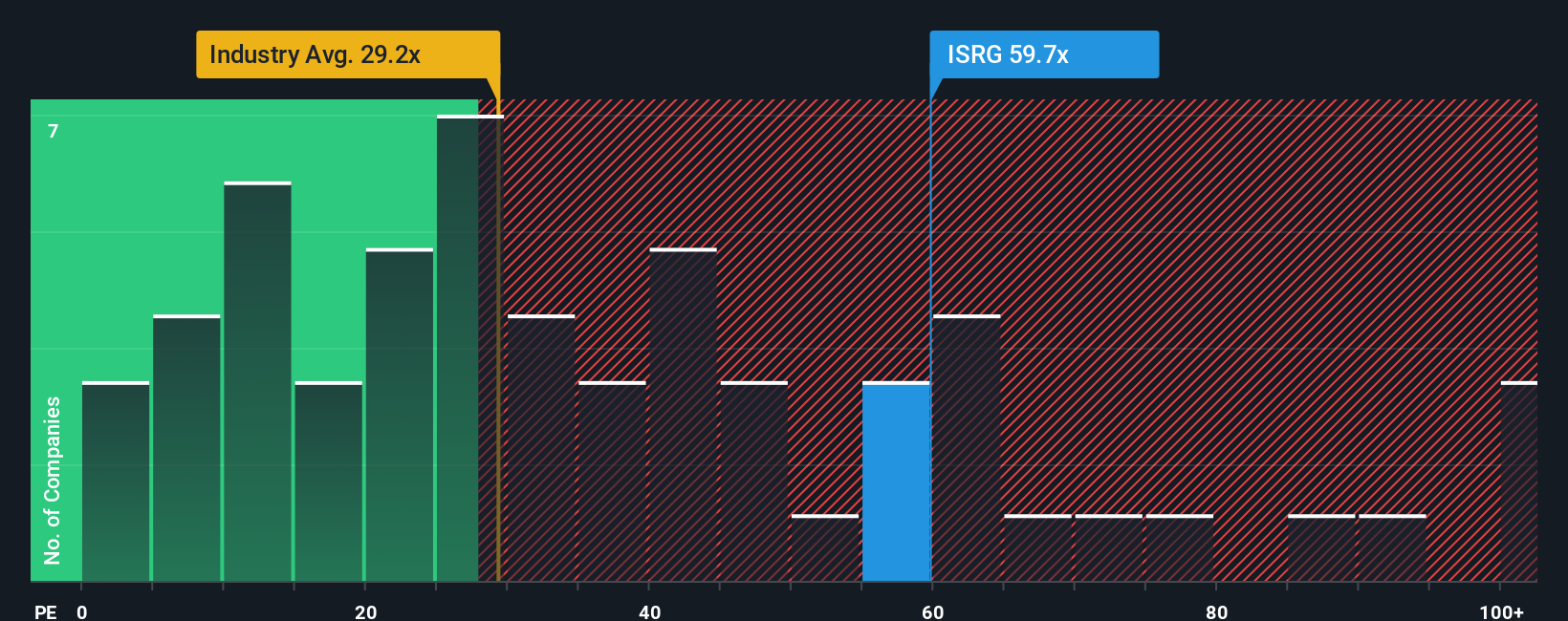

Approach 2: Intuitive Surgical Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay directly to the earnings the business is already generating. It gives a quick sense of how many dollars of price the market is assigning to each dollar of current earnings.

What counts as a “normal” P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher uncertainty usually line up with a lower one.

Intuitive Surgical is trading on a P/E of 68.07x. That is above the Medical Equipment industry average P/E of 31.23x and above the peer group average of 34.21x. Simply Wall St’s Fair Ratio framework estimates a P/E of 38.70x for Intuitive Surgical, based on factors such as its earnings profile, industry, profit margins, size and risk characteristics.

The Fair Ratio is designed to be more tailored than a simple comparison with peers or industry because it adjusts for the company’s own growth outlook, risks, profitability, sector and market cap. Compared with this Fair Ratio, the current P/E of 68.07x is higher than the modelled 38.70x, which indicates that the shares may be expensive on this earnings multiple view.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Intuitive Surgical Narrative

Earlier we mentioned that there is an even better way to think about valuation, so let us introduce Narratives. Narratives let you tell a clear story about Intuitive Surgical and then connect that story to your own revenue, earnings and margin forecasts, and finally to a fair value you can compare with the live share price.

On Simply Wall St, Narratives are available on the Community page and are used by millions of investors as an easy way to tie a company’s qualitative story to the numbers. This helps you see whether your fair value suggests Intuitive Surgical is trading at a premium or at a discount at any given time.

Each Narrative is kept current because the fair value automatically refreshes when new information comes in, such as earnings results or news. This means your story, forecast and valuation stay aligned without extra work from you.

For example, one Intuitive Surgical Narrative on Simply Wall St currently arrives at a fair value of about US$325.55 per share, while another sits near US$596.36. This shows how two investors can look at the same company, apply different growth, margin and P/E assumptions, and reach very different conclusions about whether the current price around US$527 reflects their own view of value.

For Intuitive Surgical however we will make it really easy for you with previews of two leading Intuitive Surgical Narratives:

Fair value: US$532.46

Price vs fair value: about 0.9% below this narrative fair value

Revenue growth assumption: 12%

- Frames Intuitive Surgical as a pioneer in robotic assisted surgery, with the da Vinci platform built out into a broader digital ecosystem for surgeons.

- Highlights the growing installed base and the high share of recurring revenue from instruments, services and software as key supports for the business model.

- Sees the current share price as close to fair value on this set of assumptions, while still stressing the importance of entry price and required return for each investor.

Fair value: US$325.55

Price vs fair value: about 62.0% above this narrative fair value

Revenue growth assumption: 12%

- Emphasises that Intuitive Surgical already carries a high valuation, with premium pricing that leaves little room for disappointment.

- Points to risks such as competition in surgical robotics, regulatory and reimbursement changes, and dependence on the da Vinci platform.

- Argues that if growth, margins or adoption trends fall short of expectations, the current share price could be at risk on this narrative’s fair value view.

These contrasting Narratives show how the same company can look close to fairly priced in one framework and expensive in another, depending on the assumptions you are comfortable with. They are a useful way to stress test your own view on Intuitive Surgical before you decide what to do next.

Do you think there's more to the story for Intuitive Surgical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.