Is It Time To Reassess Iridium Communications (IRDM) After This Year’s Strong Share Price Rebound

Iridium Communications Inc. IRDM | 0.00 |

- Wondering whether Iridium Communications' share price reflects its true worth, or if the market is missing something that you could be seeing instead?

- The stock last closed at US$23.95, with recent returns of 6.5% over 7 days, 22.1% over 30 days and 34.9% year to date. The 1‑year return sits at an 18.8% decline, and the 3‑ and 5‑year returns are 57.3% and 39.2% declines respectively.

- Recent attention on Iridium Communications has been driven less by a single headline and more by ongoing interest in satellite connectivity and how operators are positioned within that space. This backdrop helps frame the strong short‑term returns against the weaker multi‑year record that investors are weighing up today.

- On our checks, Iridium Communications scores 2 out of 6 on valuation, which you can see in more detail through its valuation score. Next, we will walk through the usual valuation approaches before touching on a broader way to think about what fair value really means for this stock.

Iridium Communications scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Iridium Communications Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash a company could generate in the future and discounts those amounts back to today to arrive at an estimated intrinsic value per share.

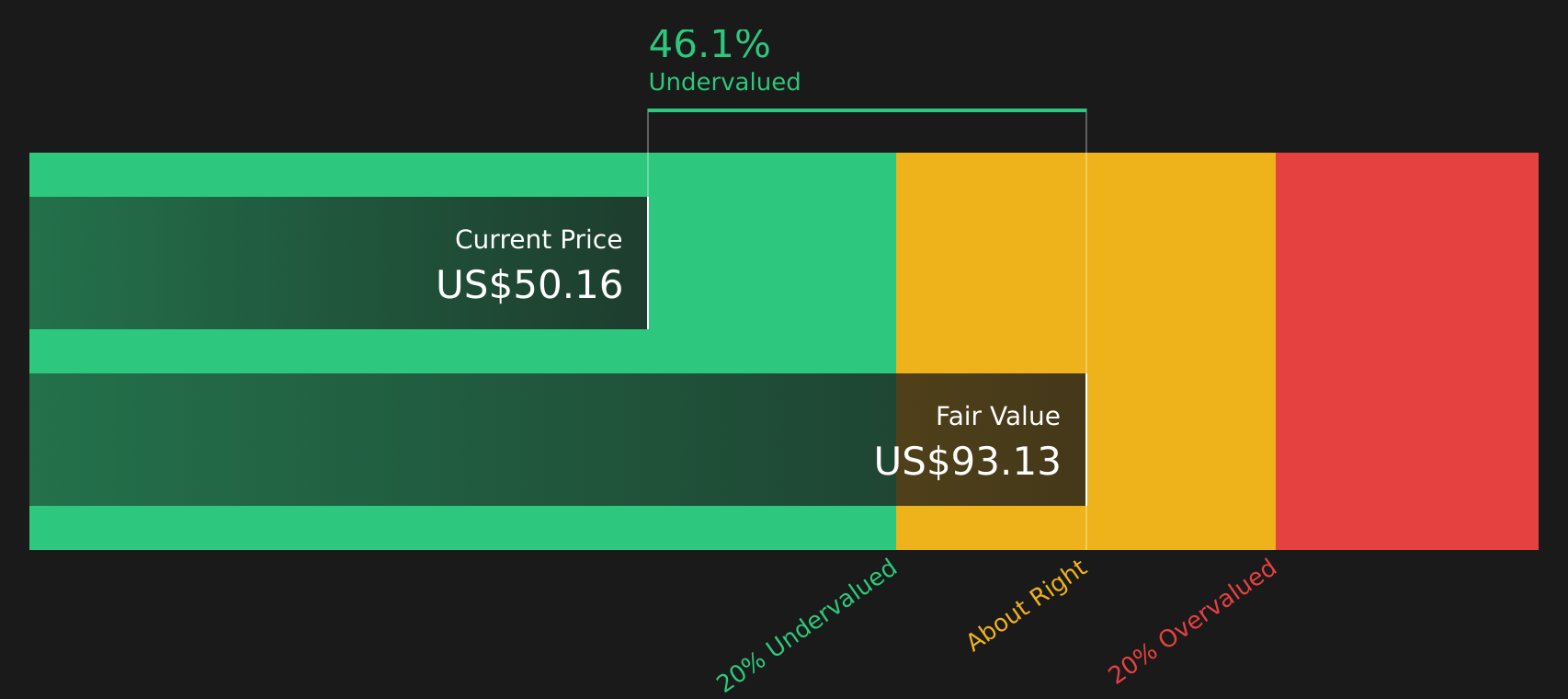

For Iridium Communications, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow sits at about $314.9 million, and analyst and extrapolated estimates put annual free cash flow around $316.8 million in 2026, rising to a projected $430.6 million in 2035. Simply Wall St uses analyst inputs where available, then extends the projections beyond the analyst horizon using its own assumptions.

On this basis, the DCF output suggests an intrinsic value of about $69.07 per share. Compared with the recent share price of $23.95, that implies the shares trade at roughly a 65.3% discount to this intrinsic value under these specific assumptions and cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Iridium Communications is undervalued by 65.3%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Iridium Communications Price vs Earnings (P/E)

For a profitable company, the P/E ratio is a useful shorthand for how much investors are willing to pay for each dollar of earnings. It links directly to what you are getting today in earnings terms for the price you pay per share.

What counts as a “normal” P/E depends on how the market views a company’s growth outlook and risk profile. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually points to a lower one.

Iridium Communications currently trades on a P/E of 22.0x. That sits above the telecom industry average of about 16.7x and above the peer group average of 8.1x. This indicates that investors are currently paying a higher price per dollar of earnings than for many comparable names.

Simply Wall St’s Fair Ratio of 15.6x is a proprietary estimate of what Iridium Communications’ P/E might be given its earnings growth profile, industry, profit margins, market cap and risk factors. This tailored yardstick can be more informative than a simple peer or industry comparison because it adjusts for the company’s specific characteristics rather than relying on broad averages.

Comparing the current P/E of 22.0x with the Fair Ratio of 15.6x indicates that Iridium Communications is trading above this modelled fair multiple.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Iridium Communications Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, which are short, plain English stories that tie your view of Iridium Communications to specific numbers like your fair value, revenue and earnings estimates and margins. You can then compare that fair value to today’s price while the platform keeps everything updated when fresh news or earnings arrive. For example, one Iridium Narrative might lean toward the higher US$45.0 fair value by focusing on faster growth in PNT and direct to device services. Another could sit closer to the US$16.0 view by stressing competition, regulatory risk and softer guidance. Your task is simply to pick or adjust the story that best matches what you believe.

For Iridium Communications however we will make it really easy for you with previews of two leading Iridium Communications Narratives:

Here is how a more optimistic and a more cautious story line up side by side so you can see which one feels closer to your own view.

Fair value in this bullish narrative: US$38.60 per share

Implied discount to that fair value at US$23.95: about 38% undervalued

Revenue growth assumption used in this narrative: 3.87%

- Focuses on Satelles and positioning, navigation and timing services as a way to build on Iridium Communications existing satellite network without large extra capital outlay.

- Highlights management share buybacks around US$27 to US$28 as a signal that they see the stock as attractive relative to intrinsic value and future plans through roughly 2030.

- Suggests watching PNTS adoption, IoT and service revenue trends, margins, cash flow and capital allocation decisions as the key checks on whether this upside story is staying on track.

Fair value in this bearish narrative: US$16.00 per share

Implied premium to that fair value at US$23.95: about 50% overvalued

Revenue growth assumption used in this narrative: 2.12%

- Flags pressure from terrestrial networks and large low Earth orbit constellations as a risk to Iridium Communications addressable market, pricing power and long term growth.

- Points to regulatory and contract related uncertainty, capital needs for future satellites and softer 2026 guidance as possible constraints on margins and free cash flow.

- Frames the US$25 analyst bearish target as close to the recent share price, with the view that current expectations may already bake in benefits from spectrum optionality that are still early.

If you want to see these viewpoints in full and decide which one fits your own assumptions, you can use the Community Narratives as a starting point, adjust the fair values and drivers, and build a version of the Iridium Communications story that you are comfortable anchoring your decision to.

Do you think there's more to the story for Iridium Communications? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.