Is It Time To Reassess Lennar (LEN) After Its Recent Share Price Slide

Lennar Corporation Class A LEN | 0.00 |

- If you are wondering whether Lennar’s current share price reflects its real worth, you are not alone. This article focuses on what the numbers say about value rather than short term market noise.

- The stock recently closed at US$86.20, with returns of a 6.6% decline over 7 days, a 0.3% decline over 30 days, a 17.3% decline year to date and a 17.3% decline over 1 year, putting recent price moves firmly on investors’ radar.

- Recent coverage has highlighted Lennar in the context of broader housing and construction sentiment, with investors reassessing how interest rates and demand for new homes might influence longer term expectations for the stock. This backdrop provides useful context for understanding why the share price and valuation have been in focus.

- Lennar currently scores 4/6 on a set of valuation checks. The next sections look at what different valuation approaches say about that score and finish by pointing to a way of assessing value that goes beyond a single framework.

Approach 1: Lennar Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Lennar is expected to generate in the future, then discounts those projections back to a single value in today’s dollars. It is essentially asking what that stream of future cash flows is worth right now.

For Lennar, the latest twelve months free cash flow is a loss of $81.99m. Analysts provide explicit forecasts out to 2027, where free cash flow is projected at $1.85b. Beyond that, Simply Wall St extrapolates further, with ten year projections that stay in the billions of dollars each year, all in US$ and all discounted using a 2 Stage Free Cash Flow to Equity model.

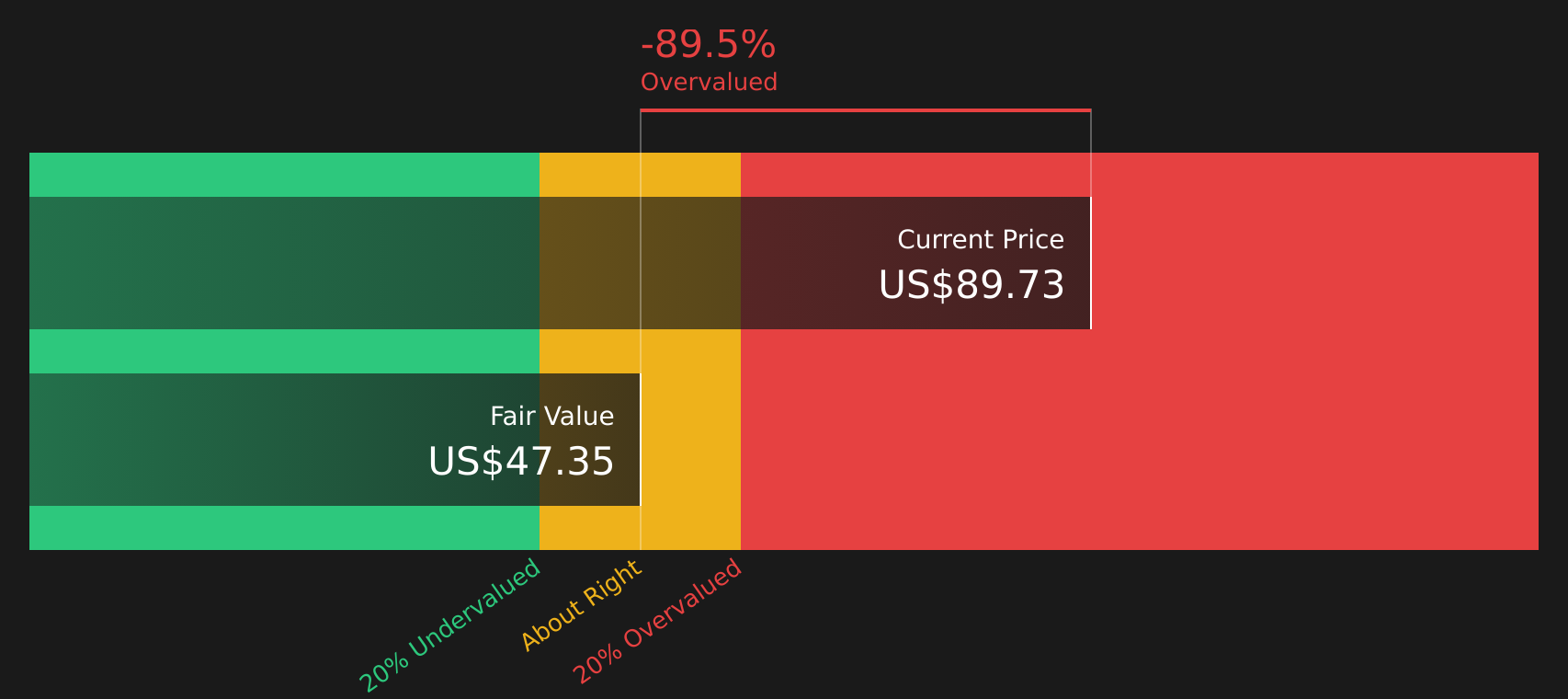

Pulling those projections together, the model estimates an intrinsic value of about $165.79 per share. Compared with the recent share price of $86.20, the DCF implies a 48.0% discount, which indicates that Lennar stock appears materially undervalued on this cash flow view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Lennar is undervalued by 48.0%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Lennar Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a straightforward way to relate the stock price to the earnings that support it. You are essentially asking how many dollars investors are currently willing to pay for each dollar of earnings.

What counts as a "normal" or "fair" P/E can depend on how fast earnings are expected to grow and how risky those earnings are. Higher growth and lower perceived risk can support a higher multiple, while lower growth or higher risk can support a lower one.

Lennar currently trades on a P/E of 11.99x. That sits close to the Consumer Durables industry average P/E of 11.55x and below a peer group average of 14.18x. Simply Wall St’s Fair Ratio for Lennar is 21.30x, which is its proprietary estimate of what the P/E might be given factors such as earnings growth, industry, profit margins, market cap and key risks.

The Fair Ratio is more tailored than simple peer or industry comparisons because it adjusts for company specific traits rather than assuming all companies deserve similar multiples. Comparing Lennar’s current 11.99x P/E with the 21.30x Fair Ratio indicates that the stock is trading below the level implied by those fundamentals.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Lennar Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St’s Community page let you attach a clear story about Lennar to specific assumptions for future revenue, earnings and margins, link that story to a forecast and Fair Value, and then compare that Fair Value with today’s share price. You can decide whether you side with a higher fair value view around US$162.49 that assumes revenue growth of about 5.67%, a 10.0% profit margin and a future P/E of 11.6x, or a lower fair value view around US$74.00 that assumes slower revenue growth of about 2.67%, a 4.21% profit margin and a future P/E of 13.40x. Each Narrative updates automatically as new earnings, news or guidance are fed into the platform, so you can quickly see how the story and valuation you agree with stack up against the current market price.

For Lennar, however, we will make it really easy for you with previews of two leading Lennar Narratives:

Both are built from explicit assumptions for revenue, margins, P/E and discount rates, but they reach very different conclusions about what the stock is worth. Lining them up side by side helps you see exactly which story your own expectations are closer to.

Fair value: US$162.49

Implied discount to this fair value: 46.9% based on the recent US$86.20 share price

Assumed revenue growth: 5.67%

- Views Lennar as benefiting from a structural US housing shortfall of an estimated 3 to 5 million units, with particular focus on affordable homes in high demand regions such as the Sun Belt and Texas.

- Builds a fair value around revenue growing at 5.67% a year and a 10.0% profit margin, with the stock supported by a future P/E of 11.6x and a fair value of US$162.49 per share.

- Sees the recent homebuilding pullback and weaker demand as a period where valuation has reset closer to underlying revenue trends, with the stock framed as discounted relative to this long term housing thesis.

Fair value: US$74.00

Implied premium to this fair value: 16.5% based on the recent US$86.20 share price

Assumed revenue growth: 2.67%

- Starts from weaker assumed revenue growth of 2.67% a year and thinner profit margins of about 4.21%, reflecting pressure from high mortgage rates, buyer affordability constraints and higher sales incentives.

- Argues that to justify a US$74.00 fair value, Lennar would need to earn around US$1.5b by about 2029 and trade on a future P/E of about 13.40x, which is higher than the current industry multiple cited in the narrative.

- Highlights concerns around land banking costs, margin compression and the risk that the current share price embeds expectations that are too optimistic if these lower growth and margin assumptions play out.

Together, these previews give you a clear range for what engaged Lennar followers think the stock could be worth based on different, explicit sets of assumptions. Once you have a sense of which revenue and margin path feels more realistic to you, it becomes easier to judge whether today’s US$86.20 share price lines up more closely with the higher or lower fair value story, or whether you sit somewhere in between.

If you want to see how other investors are framing the trade off between growth, margins and valuation for Lennar, you can start by checking the See what the community is saying about Lennar.

Do you think there's more to the story for Lennar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.