Is It Time To Reassess Owens Corning (OC) After Mixed Returns And Sector Headlines

Owens Corning OC | 0.00 |

- If you are wondering whether Owens Corning stock offers good value at its current price, it is important to understand what the recent share performance and fundamentals are really saying about the business.

- The stock last closed at US$124.24, with returns of 7.0% over 7 days, 0.2% over 30 days, 8.8% year to date, a decline of 5.9% over 1 year, and gains of 21.0% over 3 years and 29.6% over 5 years. Taken together, this gives a mixed picture of recent momentum and longer term results.

- Recent headlines around Owens Corning have focused on the broader building materials sector and changing expectations for construction related demand, which often influence how investors think about this stock's risks and prospects. This context can help explain why short term price moves occasionally look out of step with the longer term record.

- Owens Corning currently has a valuation score of 4 out of 6. The next sections will walk through the key valuation approaches behind that score, followed by a toolkit that can help you assess value even more effectively on your own.

Approach 1: Owens Corning Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash Owens Corning is expected to generate in the future and discounts those projections back to today, aiming to estimate what the stock could be worth based on those cash flows.

Owens Corning’s latest twelve month Free Cash Flow is about $991.5 million. Analyst forecasts and subsequent extrapolations suggest Free Cash Flow of about $712.0 million in 2026 and $926.6 million in 2027, with Simply Wall St extending the projections out to 2035. By 2035, the model assumes Free Cash Flow of roughly $934.9 million, all in $ and all discounted using a 2 Stage Free Cash Flow to Equity framework.

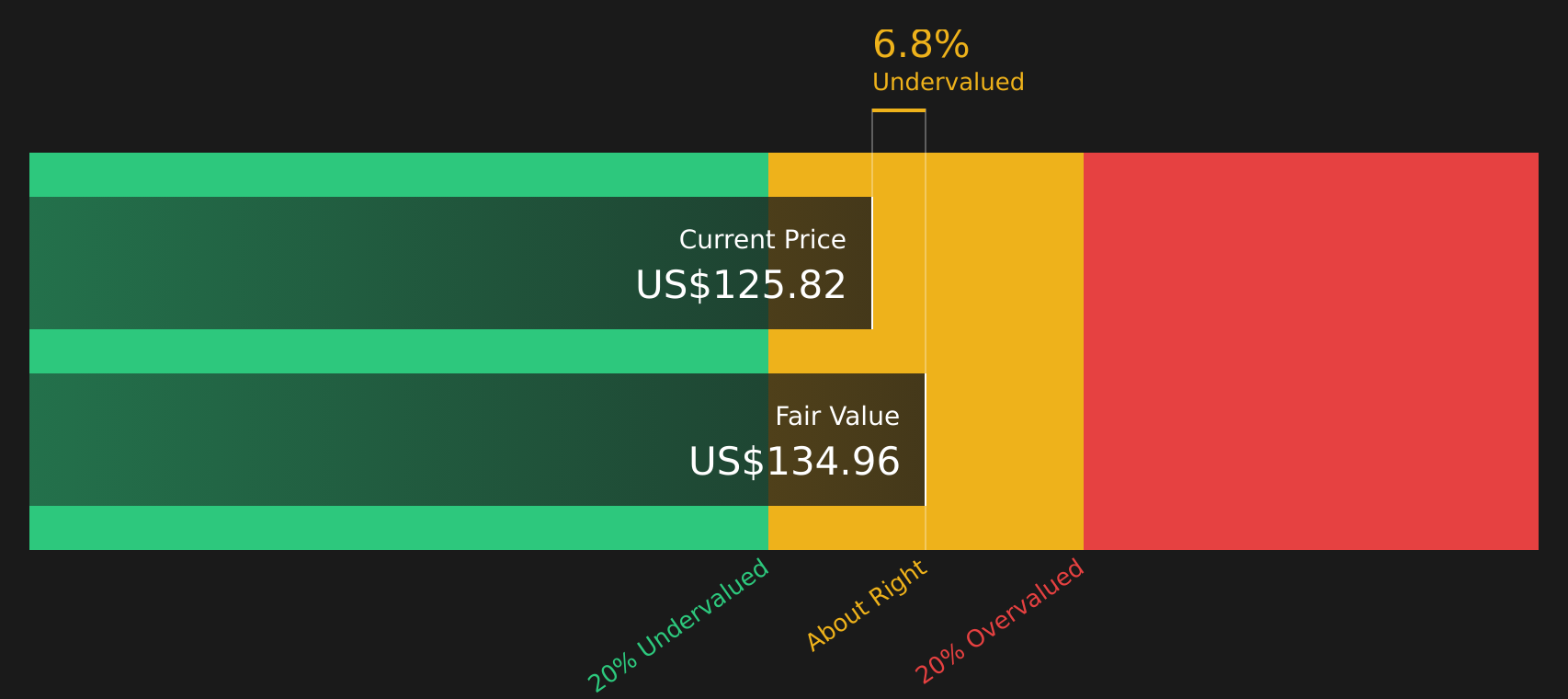

When these discounted cash flows are added up, the model indicates an estimated intrinsic value of about $134.36 per share, compared with the recent share price of $124.24. That implies the stock is around 7.5% below the DCF estimate, which sits within a range that many investors would see as close to fair value.

Result: ABOUT RIGHT

Owens Corning is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Owens Corning Price vs Sales

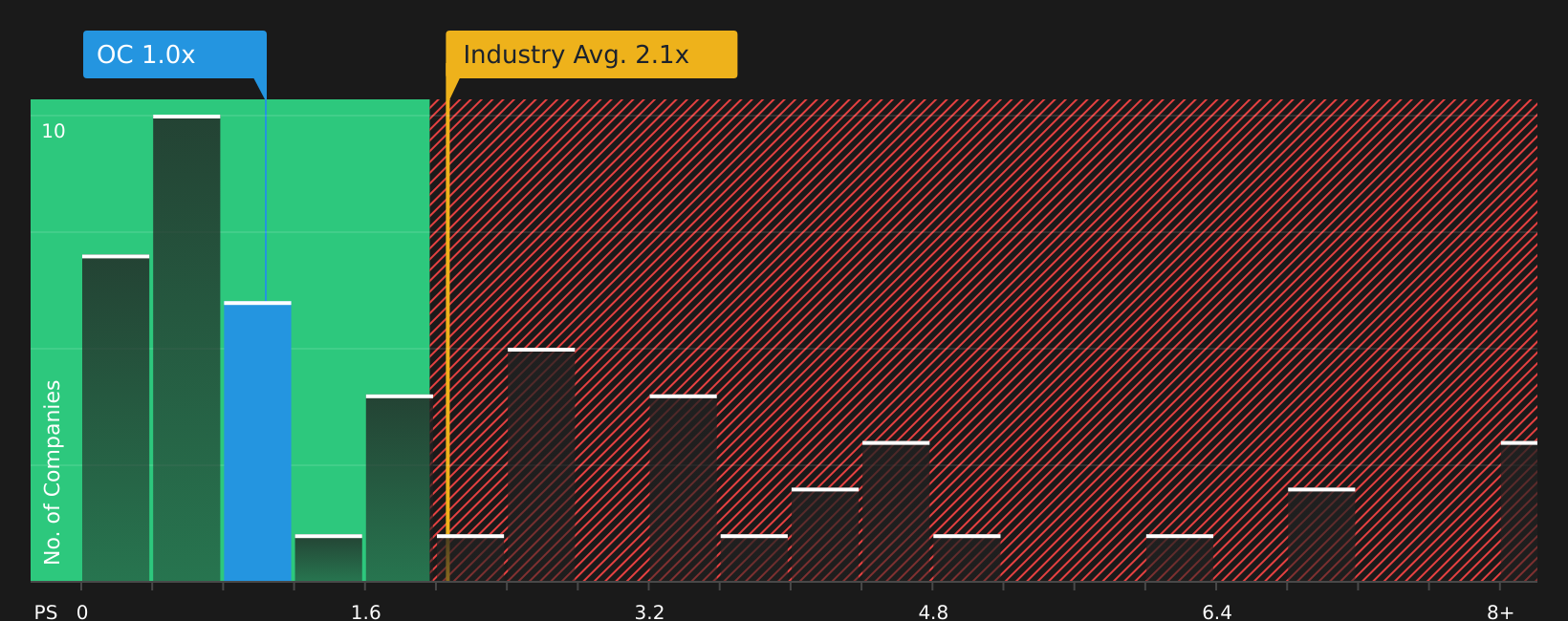

For companies that are profitable and generate meaningful revenue, the P/S ratio is a straightforward way to see how much investors are paying for each dollar of sales, without getting caught up in short term swings in earnings.

What counts as a reasonable P/S ratio often reflects how investors see a company’s growth potential and risk profile. Higher expected growth or lower perceived risk can justify a higher multiple, while lower growth or higher risk usually line up with a lower P/S.

Owens Corning currently trades on a P/S ratio of 1.02x. This compares with an industry average P/S of 2.01x for Building stocks and a peer average of 3.51x. Simply Wall St’s Fair Ratio for Owens Corning is 1.69x. This is a proprietary estimate of the P/S multiple that might be expected after considering factors such as earnings growth, profit margins, industry, market cap and risk indicators.

Because the Fair Ratio is tailored to Owens Corning’s own fundamentals, it can be more informative than a simple comparison with peers or the broader industry. With the current P/S of 1.02x sitting below the Fair Ratio of 1.69x, the stock screens as undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Owens Corning Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives on Simply Wall St let you attach a clear story to your numbers by linking your view on Owens Corning’s future revenue, earnings and margins to a forecast and then to a fair value. Because these Narratives sit in the Community page and update automatically when new earnings or news arrives, you can quickly see how your chosen fair value compares with the live share price and decide whether you see Owens Corning as closer to the more optimistic US$166.0 view, the more cautious US$110.0 view, or somewhere around the US$144.8 consensus in between.

For Owens Corning however we will make it really easy for you with previews of two leading Owens Corning Narratives:

Fair value used in this bullish narrative: US$144.80

Gap to this fair value based on the latest close of US$124.24: about 14.2% below the narrative fair value

Revenue growth assumption used in the narrative: 2.94%

- Analysts in this narrative are building on guidance for 2026 and completed buybacks, linking them to expectations for future earnings power and capital returns.

- The story leans on investments in capacity, technology and higher margin products, along with exposure to repair and remodel markets in North America and Europe.

- Key risks centre on divestitures, cyclicality in construction markets, potential oversupply in insulation and roofing, cost inflation, tariffs and competition for contractor loyalty.

Fair value used in this bearish narrative: US$110.00

Gap to this fair value based on the latest close of US$124.24: about 12.9% above the narrative fair value

Revenue growth assumption used in the narrative: 6.67%

- This more cautious view focuses on the risk that cost inflation, production curtailments and slower housing and remodel activity could weigh on margins and free cash flow for longer.

- It highlights execution risks around new capacity, possible delays in nonresidential projects and pressure on the Doors segment from tariffs and weaker discretionary spending.

- On valuation, the narrative works back from a US$110.00 price target and lower revenue expectations, using a 9.92% discount rate and a 6.0x P/E on projected 2028 earnings, while still flagging that some analysts hold much higher targets.

Those two narratives frame the current debate around Owens Corning. The next step is to decide which assumptions feel closer to your own view on construction demand, margin resilience and how much you are willing to pay for the stock’s future cash flows.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Owens Corning on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Owens Corning? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.