Is It Time To Reassess SentinelOne (S) After The Recent Share Price Slide?

SentinelOne S | 0.00 |

- Wondering if SentinelOne's current share price reflects its true worth, or if the recent volatility has left the stock mispriced.

- The stock closed at US$14.79, with returns that are roughly flat year to date at 1.0%, while the price has fallen about 9.3% over the last week, 9.4% over the last month, and 17.7% over the last year.

- Recent headlines around SentinelOne have focused on its position in the cybersecurity sector and how investors are reassessing growth-focused software stocks. This helps frame these price moves. For you as a shareholder or potential buyer, this context matters because sentiment around future growth and risk can swing valuations quickly.

- SentinelOne currently has a valuation score of 3/6. The rest of this article will walk through what that means across different valuation methods and then finish with a more holistic way to think about what the stock could be worth.

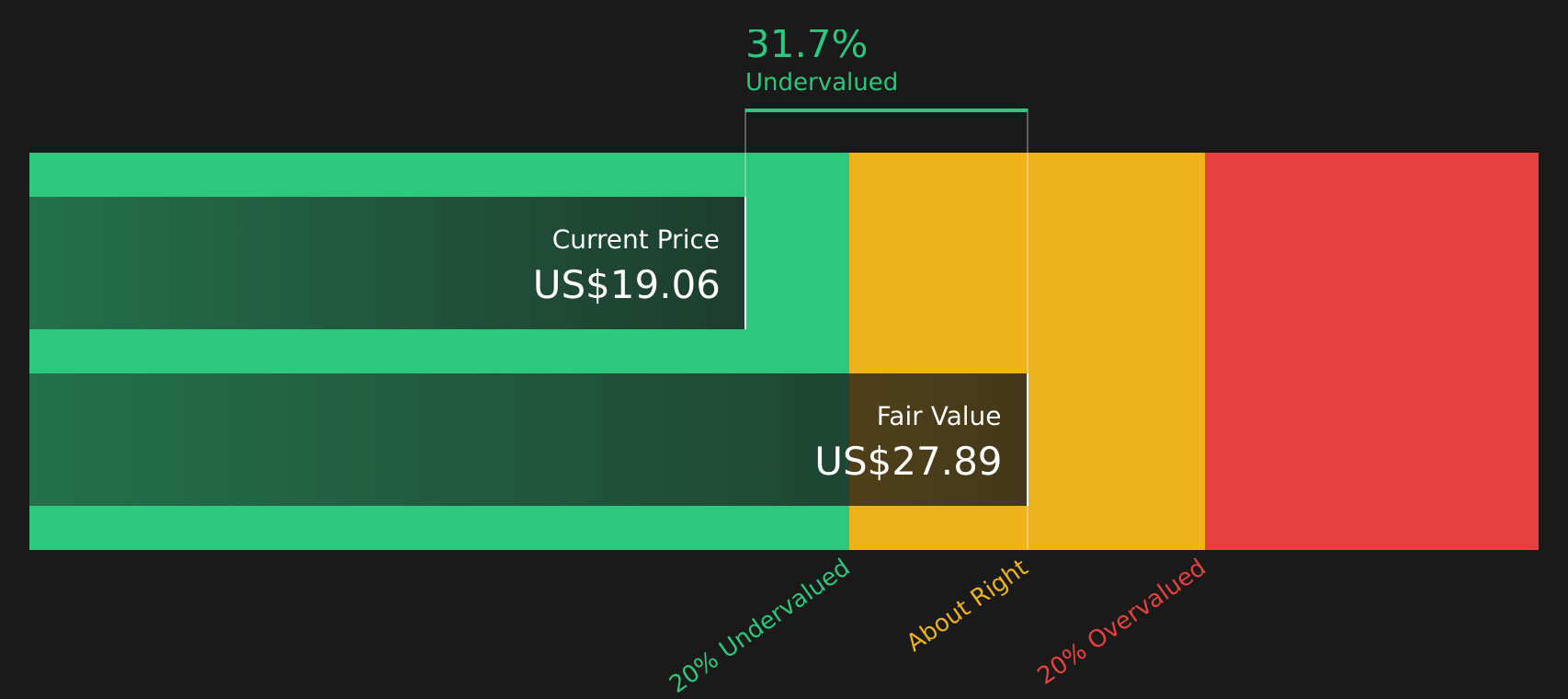

Approach 1: SentinelOne Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and then discounting those back to today’s value.

For SentinelOne, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $32.38 million, and analysts plus extrapolated estimates point to free cash flow of $284.19 million in 2029 and $655.13 million by 2035. Simply Wall St converts these annual figures into today’s dollars using a discount rate, producing a per share intrinsic value estimate of $23.58.

Compared to SentinelOne’s recent share price of $14.79, this DCF output implies the stock trades at a discount of about 37.3%, which indicates it screens as undervalued on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests SentinelOne is undervalued by 37.3%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: SentinelOne Price vs Sales

For companies where earnings are not yet a steady guide, the Price to Sales, or P/S, ratio is often a useful way to think about valuation, because it links the stock price to current revenue instead of profits.

Growth expectations and risk both influence what feels like a reasonable P/S ratio. Faster, more predictable growth and lower perceived risk can support a higher multiple, while slower or less certain growth, or higher risk, usually points to a lower one.

SentinelOne currently trades on a P/S ratio of 4.83x. That sits above the Software industry average of 3.47x and also above the peer group average of 3.81x. On headline numbers alone, the stock appears more expensive than many listed software peers.

Simply Wall St’s Fair Ratio for SentinelOne is 5.31x. This is a proprietary estimate of what the P/S multiple could be given the company’s growth profile, profit margins, industry, market cap and risk factors. Because it blends these company specific inputs, it can be more informative than a simple comparison with peers or the broad industry.

Comparing the Fair Ratio of 5.31x with the current P/S of 4.83x indicates that the stock screens as undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your SentinelOne Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as your way to attach a clear story about SentinelOne, including your assumptions for future revenue, earnings, margins and fair value. You can then link that story to a financial forecast and a fair value estimate that you can easily compare with the current share price on Simply Wall St’s Community page.

Because Narratives on the platform update when new information such as news or earnings is added, you can see in real time how different viewpoints translate into numbers. For example, this might be a more optimistic SentinelOne view with a Fair Value around US$24.81, or a more cautious stance closer to US$14.00. This shows how reasonable investors can look at the same company, interpret the outlook differently and reach very different conclusions about what the stock is worth today.

For SentinelOne however, we will make it really easy for you with previews of two leading SentinelOne Narratives:

Fair value: US$19.15

Gap to current price: around 22.8% below this narrative fair value

Revenue growth used in this view: 18.14% a year

- Assumes continued adoption of AI driven security products and multi product bundles, with revenue and margins benefiting from Purple AI, the AI native SIEM platform and the Flex licensing model.

- Builds in ongoing expansion into areas such as cloud security, identity and data protection, supported by partnerships with hyperscalers and managed security providers.

- Accepts risks around partner dependency, regulation, international execution and industry consolidation, but still treats the stock as broadly aligned with analyst consensus fair value at around US$19.15.

Fair value: US$14.00

Gap to current price: around 5.3% above this narrative fair value

Revenue growth used in this view: 17.93% a year

- Emphasizes pressure from rising compliance and localization demands, which may push up costs and make scaling international revenue harder.

- Focuses on competition, product commoditization and the spread of open source tools that could weigh on pricing power, margins and long run earnings.

- Uses a lower fair value of US$14.00 that lines up with the more cautious end of analyst targets, assuming slower revenue progress and a more modest earnings path than the bullish view.

Side by side, these Narratives give you clear bookends on what SentinelOne might be worth, the growth that would need to show up and the key risks that could shift the story either way, so you can decide which version feels closer to your own expectations.

Do you think there's more to the story for SentinelOne? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.