Is It Time To Reassess Shift4 Payments (FOUR) After Its 54% One Year Share Price Fall

Shift4 Payments FOUR | 0.00 |

- With Shift4 Payments trading at around US$43.29, this article examines whether the current market price may be pointing to a potential recovery or further weakness, and what that might imply about value.

- The stock has inched up about 1.2% over the last week, but remains down about 4.2% over the last month, about 30.9% year to date and about 54.5% over the past year.

- Recent headlines have focused on Shift4 Payments within broader discussions of payments and fintech stocks. These have drawn attention to how investors are reassessing risk and growth expectations across the sector. News coverage has also highlighted how some investors are looking more closely at balance sheets and business models after such a steep 1 year share price decline.

- Against this backdrop, Shift4 Payments currently scores just 1 out of 6 on Simply Wall St's valuation checks. The next sections will unpack what different valuation methods say about the stock today and then finish with a broader way to think about value beyond the usual ratios.

Shift4 Payments scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

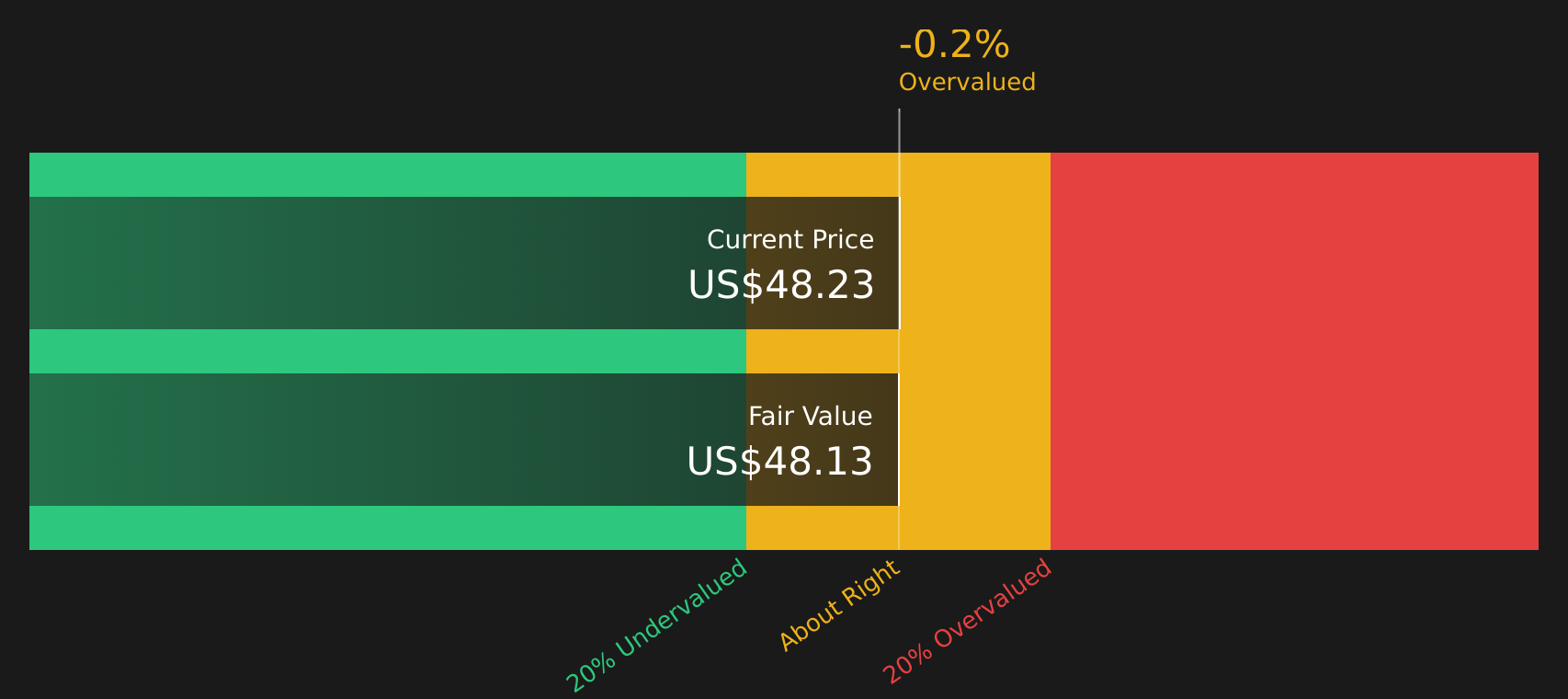

Approach 1: Shift4 Payments Excess Returns Analysis

The Excess Returns model looks at how much value Shift4 Payments creates over and above the return that equity investors typically require. Instead of focusing on cash flows, it compares the company’s return on equity to its cost of equity and then projects how this gap might compound over time.

For Shift4 Payments, book value is $8.17 per share, while stable earnings per share are estimated at $3.64, based on the median return on equity from the past 5 years. The cost of equity is estimated at $2.38 per share, which implies an excess return of $1.26 per share. The average return on equity used in the model is 14.47%, and analysts see stable book value moving toward $25.14 per share using weighted future estimates from three analysts.

Putting these inputs together, the Excess Returns model arrives at an intrinsic value of about $46.45 per share. Against the current share price of about $43.29, this suggests the stock is roughly 6.8% undervalued, which is a modest gap.

Result: ABOUT RIGHT

Shift4 Payments is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Shift4 Payments Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it tells you how much you are paying for each dollar of earnings. It naturally reflects what the market thinks about a company’s prospects and risk profile.

Higher growth expectations and lower perceived risk typically support a higher “normal” P/E, while slower growth or higher risk usually align with a lower multiple. So context matters when comparing any single P/E to a benchmark.

Shift4 Payments currently trades on a P/E of 55.39x. That is well above the Diversified Financial industry average of 17.73x and also above the peer average of 24.93x. Simply Wall St’s proprietary Fair Ratio for Shift4 Payments is 23.42x, which is an estimate of what the P/E might be given factors such as earnings growth, industry, profit margin, market cap and specific risks.

The Fair Ratio can be more informative than a simple peer or industry comparison because it attempts to tailor the multiple to the company’s own profile rather than assuming all companies should trade on the same benchmark.

Comparing the Fair Ratio of 23.42x with the actual P/E of 55.39x suggests the stock is trading above what would be considered a fair multiple on these inputs.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Shift4 Payments Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a clear story behind the numbers by linking your view on Shift4 Payments, such as how its acquisitions, crypto payments and sector exposure might play out, to a set of revenue, earnings and margin estimates that roll up into a Fair Value. You can then compare that Fair Value with today’s share price to help you judge whether the stock looks cheap or expensive on your assumptions. The platform’s Community page shows a range of Narratives, from more cautious views that line up with an implied Fair Value around US$40 to more optimistic cases closer to about US$121 or US$66. All of these automatically refresh when new earnings, news or guidance are added so you can quickly see how fresh information might affect your own investment decisions.

For Shift4 Payments, however, we will make it really easy for you with previews of two leading Shift4 Payments Narratives:

Fair value: US$65.73 per share

Implied discount to this fair value: about 34% below the narrative fair value

Revenue growth assumption: 17.19% a year

- Analysts in this camp anchor on international acquisitions, value added services and cross selling as key drivers for higher revenue and margins.

- They factor in continued expansion of digital and cashless payments across hospitality, sports, entertainment and luxury retail.

- Their fair value reflects confidence in pulling together growth, margins and acquisition synergies, while still acknowledging execution, leverage and technology risks.

Fair value: US$40.00 per share

Implied premium to this fair value: about 8% above the narrative fair value

Revenue growth assumption: 13.59% a year

- The more cautious view leans on slower assumed revenue growth and more modest margin gains, even with new markets and crypto payment capabilities.

- It places more weight on leverage, refinancing needs around the Global Blue deal and macro pressures on consumer spending.

- Here, valuation is anchored closer to the lower end of analyst targets, with a tighter gap between the narrative fair value and the current share price.

If you want to see how these different assumptions, risks and earnings paths come together in full, including detailed forecasts and valuation math, See what the community is saying about Shift4 Payments.

Do you think there's more to the story for Shift4 Payments? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.