Is It Time To Reassess United Parcel Service (UPS) After Recent Logistics Sector Concerns?

United Parcel Service, Inc. Class B UPS | 0.00 |

- Investors may be wondering whether United Parcel Service stock is offering fair value right now or if the price is out of line with what they receive for it.

- The stock last closed at US$101.97, with returns of 5.3% over the past week, down 4.7% over the past month, up 0.9% year to date, up 11.7% over 1 year, and down 29.2% and 40.1% over 3 and 5 years respectively.

- Recent coverage around parcel volumes, pricing conditions, and broader logistics sector sentiment has kept attention on how dependable UPS's cash flows and market position might be viewed by investors. At the same time, commentary on competition and cost pressures has been shaping expectations around what kind of valuation investors are willing to pay.

- On Simply Wall St's valuation checks, UPS scores a 4 out of 6. The rest of this article explains what different valuation methods indicate about that number and then points to a more complete way to think about value at the end.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of future cash that a company may generate and discounts those amounts back to today using a required rate of return. The result is an estimate of what the entire stream of future cash flows could be worth in today’s money.

For United Parcel Service, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow stands at about $4.03b. Analyst inputs and Simply Wall St extrapolations suggest free cash flow projections such as $5.73b in 2026, $7.10b in 2027, and extending out to $9.70b by 2035, all in $ terms. These future figures are then discounted back to reflect their value today.

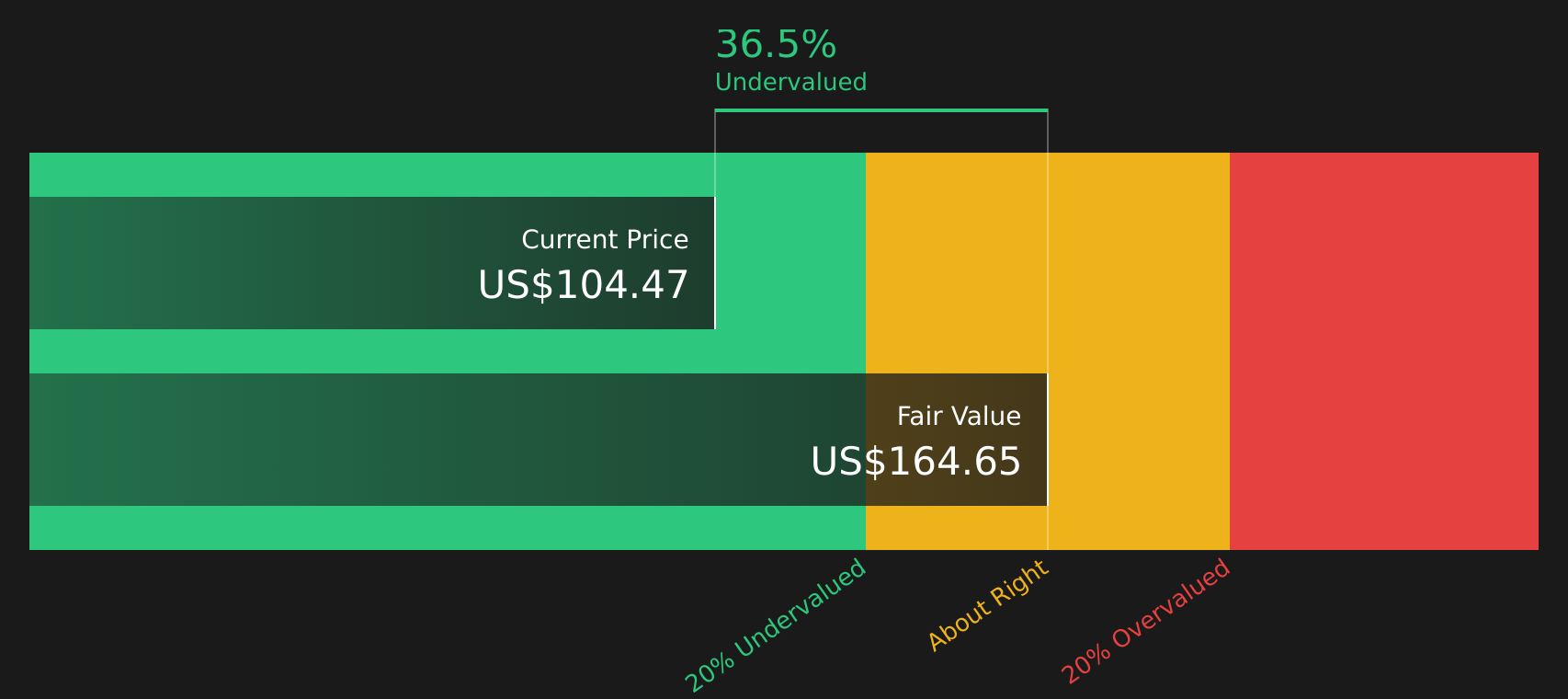

Pulling this together, the DCF model produces an estimated intrinsic value of $165.93 per share. Compared with the recent share price of $101.97, this suggests the stock screens as around 38.5% undervalued based on these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 38.5%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For a profitable company like United Parcel Service, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It ties the stock price directly to earnings, which many investors treat as a core driver of long term value.

What counts as a “normal” P/E depends on how the market views a company’s growth outlook and risk profile. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher uncertainty usually point to a lower multiple. United Parcel Service trades on a P/E of 16.51x, compared with a Logistics industry average of 15.42x and a broader peer group average of 23.57x.

Simply Wall St’s Fair Ratio for United Parcel Service is 22.43x. This is a proprietary estimate of what the P/E might be given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it incorporates these elements instead of relying only on broad peer or industry comparisons, the Fair Ratio can give a more tailored view of what investors are paying. With the current P/E of 16.51x below the Fair Ratio of 22.43x, the stock screens as undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier the article mentioned that there is an even better way to understand valuation. Narratives step in as your way to attach a clear story about United Parcel Service to the numbers such as fair value estimates and expectations for future revenue, earnings and margins. This links what you believe about the business directly to a financial forecast and then to a fair value that you can compare with the current share price.

On Simply Wall St’s Community page, Narratives are presented as easy to use templates that show how different assumptions feed into fair value. They help you decide if the current price looks attractive or stretched for your view, and they refresh automatically when new information like earnings or news headlines arrives, so your story and valuation stay aligned with the latest data.

For United Parcel Service, one investor might choose a cautious Narrative that aligns with a fair value around US$84.58, based on assumptions of flatter revenue and lower margins. Another might choose a more optimistic Narrative that aligns with a fair value around US$135.00, based on higher revenue growth and margins. By comparing each of these fair values with today’s share price, you can see which story fits your own expectations and risk tolerance.

For United Parcel Service however we will make it really easy for you with previews of two leading United Parcel Service Narratives:

Fair value: US$135.00

Implied discount versus last close: the shares screen as about 24.5% below this fair value based on the recent price of US$101.97.

Revenue growth assumption: 4.38% a year

- Focuses on UPS using automation, cost reduction and network reconfiguration to improve margins, cash flow and revenue per piece.

- Highlights the healthcare logistics business and global trade routes as key areas for higher margin, recurring growth.

- Flags competition, labor costs, trade volatility, new delivery models and sustainability rules as important risks to those earnings and cash flow expectations.

Fair value: US$95.21

Implied premium versus last close: the shares screen as about 7.1% above this fair value based on the recent price of US$101.97.

Revenue growth assumption: 1.75% a year

- Emphasizes higher costs, sustainability questions and internal challenges, with Efficiency Reimagined and new debt raising as key tests for future profitability.

- Points to labor disputes, shareholder governance concerns and higher wage commitments as potential drags on margins and flexibility.

- Notes that partnerships like PeriShip and AMEX could help, but recent revenue and EPS trends and execution risk around the network overhaul keep the stance cautious.

If you want to see how these narratives are built line by line, including the detailed earnings paths and risk checks, See what the community is saying about United Parcel Service.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.