Is It Time To Reassess United Parcel Service (UPS) After Recent Share Price Rebound

United Parcel Service, Inc. Class B UPS | 98.18 | +0.28% |

- If you are wondering whether United Parcel Service shares are offering fair value at around US$118, you are not alone. This article is designed to help you size up what you are really paying for.

- The stock has returned 1.3% over the last 7 days, 10.8% over the last 30 days, 16.9% year to date, 9.1% over 1 year, while the 3 year and 5 year returns sit at 25.9% and 10.5% declines.

- Recent attention on UPS has been shaped by broader debates around parcel volumes, cost inflation and how the company is positioned against e commerce trends. These themes have kept investors focused on whether current conditions are already reflected in the share price or if the stock still carries a margin of safety.

- On Simply Wall St's 6 point valuation checklist, UPS scores a 4 out of 6. Next we will walk through what that means using approaches such as multiples and discounted cash flow, then finish with a way to think about valuation that pulls all of these pieces together.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash a business could generate in the future and discounts those amounts back to today, giving you a single figure for what the equity might be worth right now.

For United Parcel Service, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $4.27b, and Simply Wall St extends analyst style projections out over the next decade. For example, free cash flow for 2026 is modeled at $6.20b and for 2029 at $7.59b, with further values out to 2035 based on extrapolated estimates.

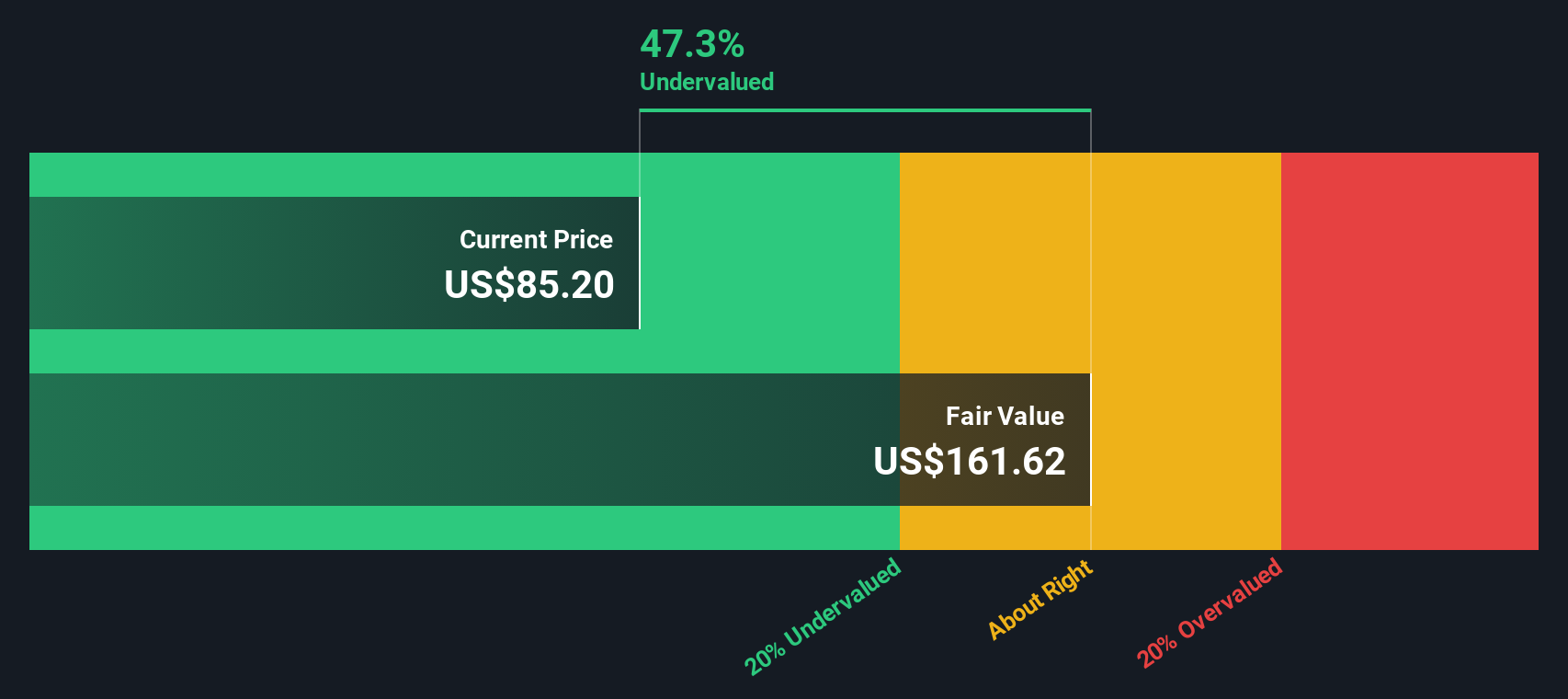

Bringing all of those projected cash flows back to today produces an estimated intrinsic value of US$162.78 per share. Against a share price around US$118, the model implies a 27.5% discount, which suggests the stock screens as undervalued on this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 27.5%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For a profitable company like United Parcel Service, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It connects directly to what many investors focus on, which is how quickly those earnings might grow and how reliable they appear to be.

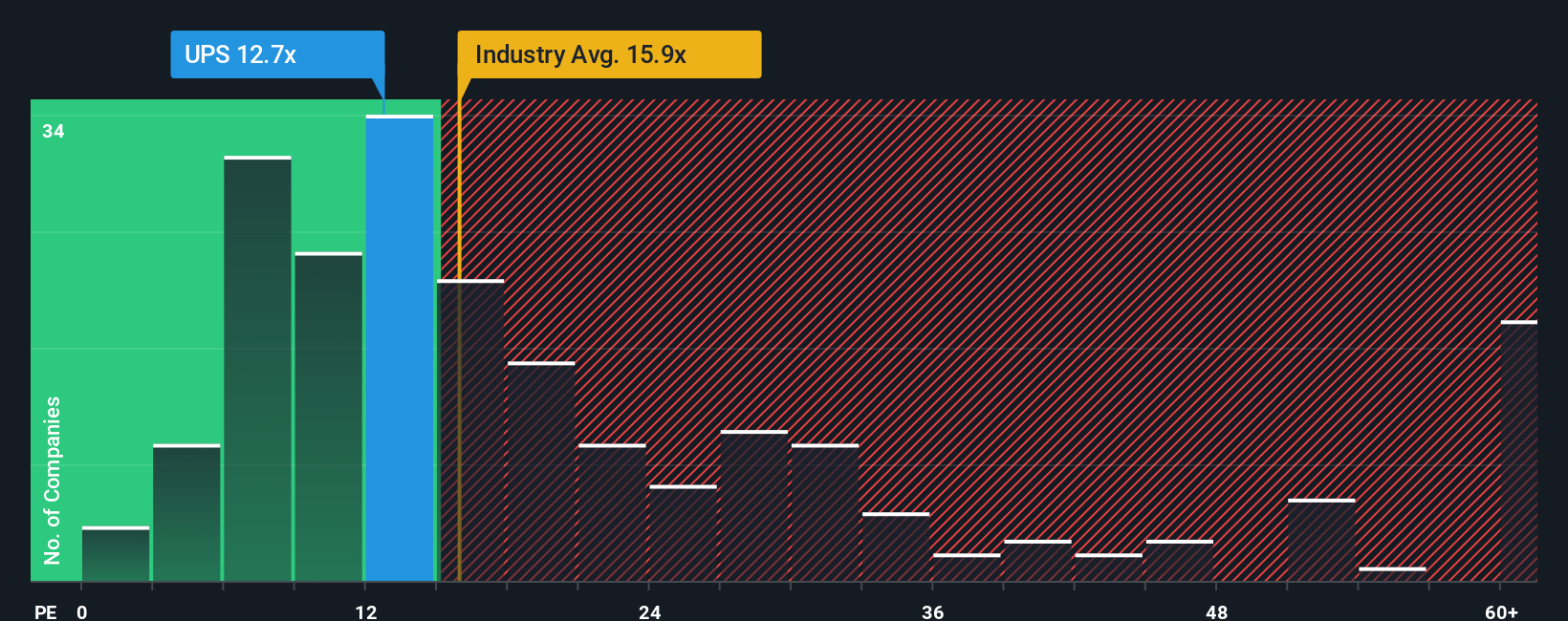

In general, higher growth expectations and lower perceived risk tend to support a higher “normal” or “fair” P/E, while slower growth and higher risk usually mean a lower one. UPS currently trades on a P/E of 18.0x. That sits above the Logistics industry average of 16.7x but below the peer group average of 22.7x, so the simple comparisons send a mixed signal.

Simply Wall St’s Fair Ratio for UPS is 21.7x. This is a proprietary estimate of what the P/E might look like given factors such as earnings growth, profit margins, industry, market cap and specific risks. Because it blends these elements rather than relying only on broad peer or sector averages, it aims to be more tailored to the company’s own profile.

Comparing the Fair Ratio of 21.7x with the current 18.0x suggests UPS trades at a discount on this metric, which indicates that the shares may be undervalued on a P/E basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a feature on Simply Wall St's Community page that lets you attach a clear story about United Parcel Service to your own forecast for revenue, earnings, margins and fair value. You can then compare that fair value with the current share price to decide whether the stock looks attractive or stretched based on your view. Each Narrative updates automatically as new earnings or news arrive. Very different perspectives on UPS are visible today, from one community member who sees fair value near US$76 to another closer to US$132, showing you in one place how cautious and optimistic investors can look at the same business and reach very different but clearly explained conclusions.

For United Parcel Service however we will make it really easy for you with previews of two leading United Parcel Service Narratives:

Fair value in this bullish Narrative: US$122.00

Implied pricing vs that fair value: around 3.2% below the Narrative fair value at the recent US$118.07 share price

Revenue growth assumption: 2.14% a year

- Automation, cost efficiencies and product mix changes are expected to support higher margins, stronger cash generation and better revenue per piece over time.

- Growth in healthcare logistics, cold chain and global trade routes is seen as a way to build more diversified, recurring and higher margin revenue streams.

- The author highlights competitive threats, labor and regulatory costs, new delivery models and sustainability requirements as key risks that could weaken profitability if they prove more demanding than expected.

Fair value in this cautious Narrative: US$95.21

Implied pricing vs that fair value: around 24.0% above the Narrative fair value at the recent US$118.07 share price

Revenue growth assumption: 1.75% a year

- The author focuses on higher costs, sustainability questions and internal pressures, with concerns that these headwinds and recent declines in revenue and earnings per share could keep profitability under pressure.

- They point to the Efficiency Reimagined program, facility closures, job cuts and new products as important, but see execution risk, added debt and higher interest costs as constraints on future financial flexibility.

- Union tensions, governance concerns and shareholder proposals are framed as signs of weaker sentiment, with new partnerships viewed as helpful but not yet enough to shift the overall picture.

Together, these Narratives show how investors looking at exactly the same UPS data can reach very different conclusions about what the shares are worth. If you want to see the full assumptions behind each view, including the detailed earnings paths, margin profiles and valuation math, you can read the complete Narratives and other community views on UPS on Simply Wall St.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.