Is It Time To Reassess Virtu Financial (VIRT) After Its Strong Recent Share Price Run?

Virtu Financial VIRT | 0.00 |

- If you are considering Virtu Financial at around US$49.66 and wondering whether it offers value or requires paying a premium for quality, this breakdown can help you clarify that question before committing fresh capital.

- The stock has posted returns of 7.4% over 7 days, 21.0% over 30 days, 52.3% year to date and 43.1% over 1 year, with a 3 year return of 188.3% and a 5 year return of 91.7%. These figures naturally raise questions about how the current price compares with the company’s underlying worth.

- Recent headlines have focused on Virtu Financial's role in capital markets and the broader conversation around trading firms and market liquidity. This discussion often affects how investors think about risk and reward for these kinds of businesses. This context can help you judge whether recent price action reflects lasting changes in expectations or shorter term sentiment swings.

- Simply Wall St currently gives Virtu Financial a valuation score of 5 out of 6. The next step is to look at how different valuation methods assess the stock and then consider a more complete way of thinking about valuation that will be covered at the end of this article.

Approach 1: Virtu Financial Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to earn above the return that shareholders typically require, and then capitalizes those “excess” profits into an intrinsic value per share.

For Virtu Financial, the model starts with a Book Value of US$18.63 per share and a Stable EPS of US$6.88 per share, based on weighted future Return on Equity estimates from 4 analysts. The Average Return on Equity is 34.19%, while the Cost of Equity is US$2.00 per share. That leaves an Excess Return of US$4.88 per share, indicating the business is expected to earn more than the required shareholder return on its equity base.

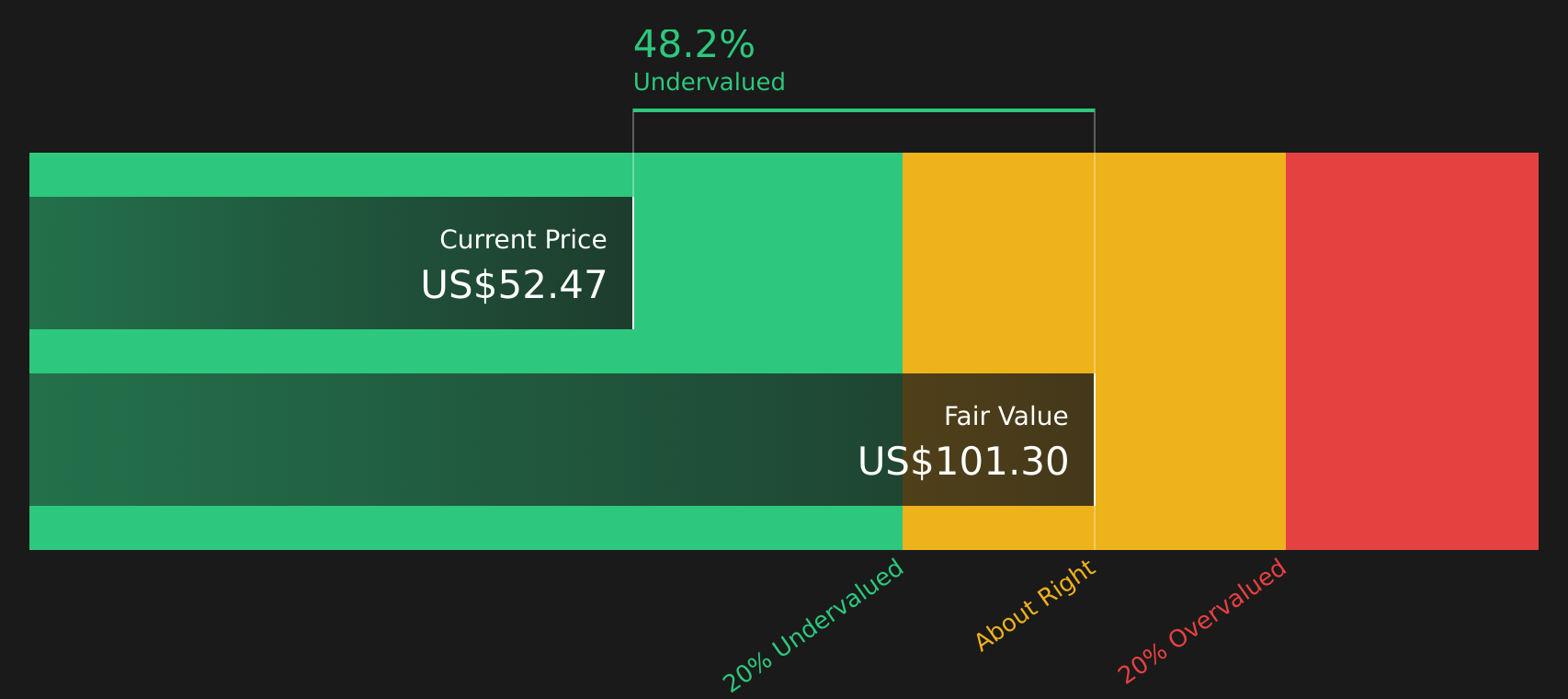

The Stable Book Value is US$20.13 per share, using weighted future Book Value estimates from 3 analysts. Combining these inputs, the Excess Returns model produces an estimated intrinsic value of about US$94.84 per share. Compared with the current share price of about US$49.66, this implies the stock is 47.6% undervalued under this framework.

Result: UNDERVALUED

Our Excess Returns analysis suggests Virtu Financial is undervalued by 47.6%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: Virtu Financial Price vs Earnings

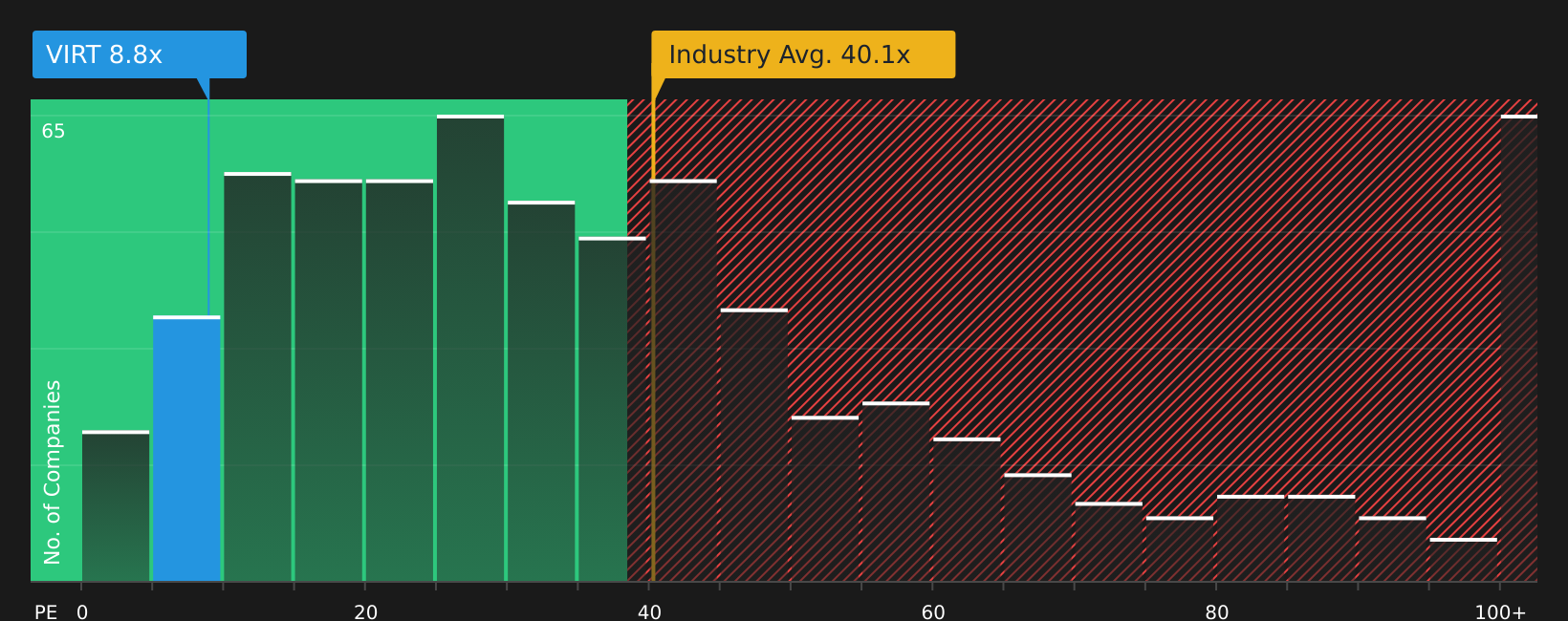

For a profitable company like Virtu Financial, the P/E ratio is a useful way to relate what you pay for the stock to the earnings it currently generates. It helps you see how many dollars investors are willing to pay today for each dollar of annual earnings.

What counts as a “normal” P/E depends on how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually lines up with a lower P/E.

Virtu Financial currently trades on a P/E of 9.82x. This is below both the Capital Markets industry average P/E of 39.09x and the peer group average of 19.63x. Simply Wall St’s Fair Ratio framework estimates a P/E of 14.39x for Virtu Financial, based on factors such as earnings growth, industry, profit margin, market cap and company specific risks. This Fair Ratio can be more informative than a simple peer or industry comparison because it tailors the expected multiple to the company’s own characteristics rather than assuming it should trade in line with broad averages.

Compared with the Fair Ratio of 14.39x, Virtu Financial’s actual P/E of 9.82x points to the shares trading below that modelled range.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Virtu Financial Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Narratives on Simply Wall St give you a simple way to set out your story for Virtu Financial, link that story to your own forecast for revenue, earnings and margins, and then translate it into a Fair Value that you can compare with the current share price. The platform already hosts very different Virtu views, from one community member who assigns a Fair Value of US$10.71 per share to analysts who publish Fair Values and price targets such as US$36.00 and US$57.00. These all update automatically as new news or earnings arrive, so you can easily see which Narrative you agree with when deciding how attractive the stock looks to you.

For Virtu Financial, here are previews of two leading Virtu Financial Narratives:

Fair value in this bullish narrative: US$57.00 per share

Gap between this fair value and the recent US$49.66 share price: about 12.9% below the narrative fair value

Revenue trend assumption in this view: 7.9% annual revenue decline

- Analysts in this camp focus on expanded electronic and multi asset trading, data services and technology products as key supports for future earnings power and higher margins.

- They build their view around assumptions for higher profit margins, a specific P/E multiple by 2028, a discount rate of about 10.5%, and share count reductions. Together, these inputs lead to the US$57.00 fair value.

- Regulation, competition, lower spreads, weaker volatility and legal or compliance costs are all highlighted as risks that could challenge this upside case.

Fair value in this more cautious narrative: US$10.71 per share

Gap between this fair value and the recent US$49.66 share price: about 364.0% above the narrative fair value

Revenue trend assumption in this view: 6.8% annual revenue decline

- This author argues that despite strong headline interest, positive cash flow and heavy use of AI and algorithmic trading, the stock price already reflects more optimism than the fundamentals justify.

- The narrative points to recent share price swings around earnings, media attention and volatility as drivers of short term moves that may not align with the long run value implied by the US$10.71 fair value.

- Readers are reminded that this is one freelance view, framed around the idea that current enthusiasm and ratings can sit well above the fair value that a more conservative model supports.

Do you think there's more to the story for Virtu Financial? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.