Is It Time To Reassess Watts Water Technologies (WTS) After Recent Price Strength

Watts Water Technologies, Inc. Class A WTS | 0.00 |

- If you are wondering whether Watts Water Technologies at around US$296 per share is still fairly priced or starting to look stretched, you are not alone.

- The stock is up 6.3% year to date and 22.3% over the last year, although it has slipped 1.3% over the past week and 2.1% over the past month, which may have some holders reassessing the balance of risk and reward.

- Recent news coverage has focused on Watts Water Technologies in the context of broader interest in industrial and infrastructure related stocks, as investors pay closer attention to companies tied to building efficiency, water systems, and related equipment. These themes help frame how the market is currently thinking about the stock and may be influencing short term price moves.

- The Simply Wall St value score for Watts Water Technologies is 2 out of 6, and the rest of this article will walk through the different valuation methods behind that figure, before finishing with a way to look at value that goes beyond any single model.

Watts Water Technologies scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Watts Water Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth today by taking projected future cash flows and discounting them back to a present value.

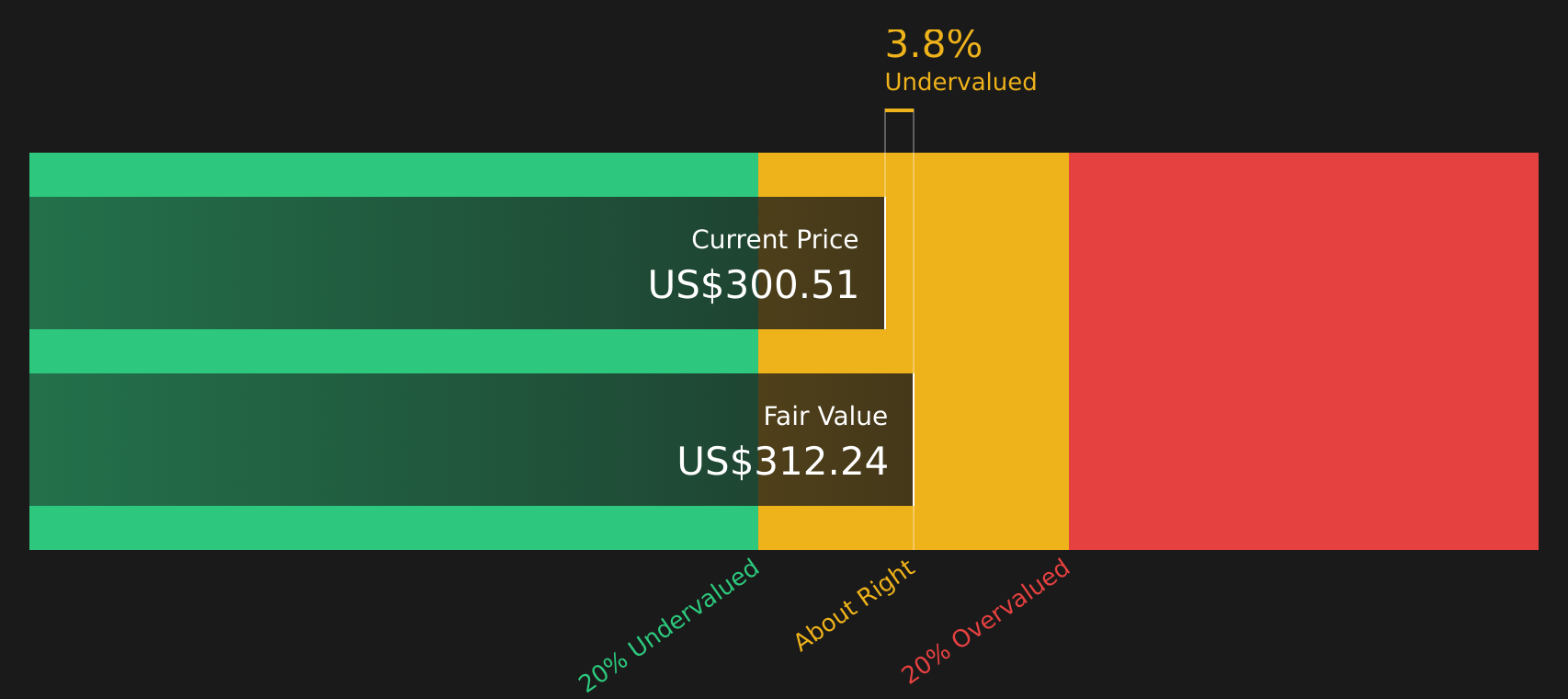

For Watts Water Technologies, the model uses last twelve months Free Cash Flow of about $321.7 million and then applies a 2 Stage Free Cash Flow to Equity approach. Analysts provide explicit forecasts out to 2029, with projected Free Cash Flow of $539.9 million in that year, and Simply Wall St extrapolates estimates beyond that using gradually moderating growth assumptions.

Across the 10 year projection period from 2026 to 2035, each year’s estimated cash flow is discounted back to today using a required return, then summed to arrive at an intrinsic value. On this basis, the DCF model produces an estimated fair value of about $312.85 per share.

Compared with the current share price of roughly $296, the model implies a discount of about 5.4%. This suggests the stock is around fair value with a slight lean to the cheap side.

Result: ABOUT RIGHT

Watts Water Technologies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

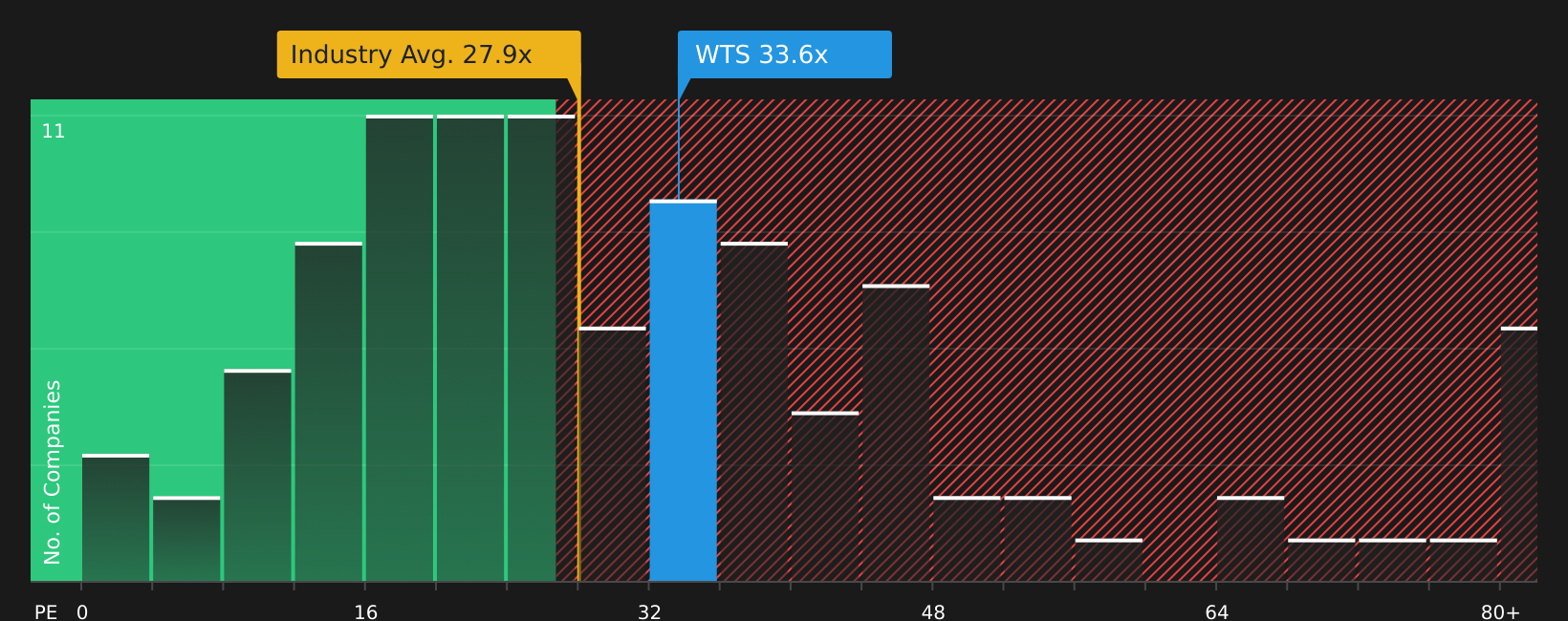

Approach 2: Watts Water Technologies Price vs Earnings

For a profitable company, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings. It captures the market’s expectations, with higher P/E ratios often linked to stronger growth outlooks or lower perceived risk, and lower P/E ratios more commonly associated with lower expected growth or higher risk.

Watts Water Technologies currently trades on a P/E of about 27x. That sits above the Machinery industry average of roughly 26.1x and below the peer average of about 29.1x, which places the stock somewhere in the middle of its listed comparables.

Simply Wall St’s Fair Ratio for Watts Water Technologies is 23.4x, which is its proprietary estimate of what the P/E might be given factors such as earnings growth, profit margins, industry, market cap and risk profile. This Fair Ratio can be more tailored than a simple comparison with industry or peer averages because it adjusts for company specific characteristics rather than treating all stocks in the group as identical. Since the current P/E of 27x is higher than the Fair Ratio of 23.4x, the stock screens as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Watts Water Technologies Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you connect your view of Watts Water Technologies as a business to a clear forecast and a Fair Value estimate. You can then compare that to today’s price to decide whether the stock looks attractive or not for you. Each Narrative lives on the Community page, updates automatically as new earnings or news arrive, and reflects very different viewpoints. For example, there is a more optimistic Narrative with a Fair Value of about US$379 that assumes revenue of roughly US$3.1b, earnings of about US$501.1m and a future P/E of around 32.4x by 2029. There is also a more cautious Narrative with a Fair Value near US$279.87 that is built around revenue of about US$3.0b, earnings of roughly US$484.8m and a future P/E near 24.4x. This structure helps you see which story, numbers and price relationship fit your own assumptions best.

For Watts Water Technologies, here are previews of two leading Watts Water Technologies narratives to help frame the discussion:

Fair value: US$379.00

Share price vs this fair value: around 21.9% below that narrative fair value

Revenue growth assumption: 7.15%

- Analysts backing this view see I-CON Systems integration, vertical integration, and automation as key drivers for higher EBITDA margins and earnings over time.

- This camp expects revenue of about US$3.1b and earnings of roughly US$501.1m by 2029, with the stock trading on a P/E of 32.4x at that point.

- The bullish case focuses on Watts Water Technologies using its balance sheet, water management capabilities, and digital offerings to act as a long term consolidator in an ongoing infrastructure upgrade cycle.

Fair value: US$279.87

Share price vs this fair value: around 5.8% above that narrative fair value

Revenue growth assumption: 6.99%

- Analysts behind this view highlight reliance on mature North American and European markets, plus potential pressure from more efficient technologies, as headwinds for long term revenue growth.

- This group works with earnings of about US$484.8m by 2029 and a lower future P/E of 24.4x, which they see as more in line with a moderated expectation for growth and profitability.

- The bear case also flags competition, ESG related costs, and uneven infrastructure spending as factors that could limit how much the current share price is supported by future cash flows.

Once you have looked at both, the key step is to decide which story, set of numbers, and implied price relationship aligns more closely with your own expectations for Watts Water Technologies.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Watts Water Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Watts Water Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.