Is It Time To Reassess Wyndham Hotels & Resorts (WH) After Recent Share Price Pullback?

Wyndham Hotels & Resorts Inc WH | 0.00 |

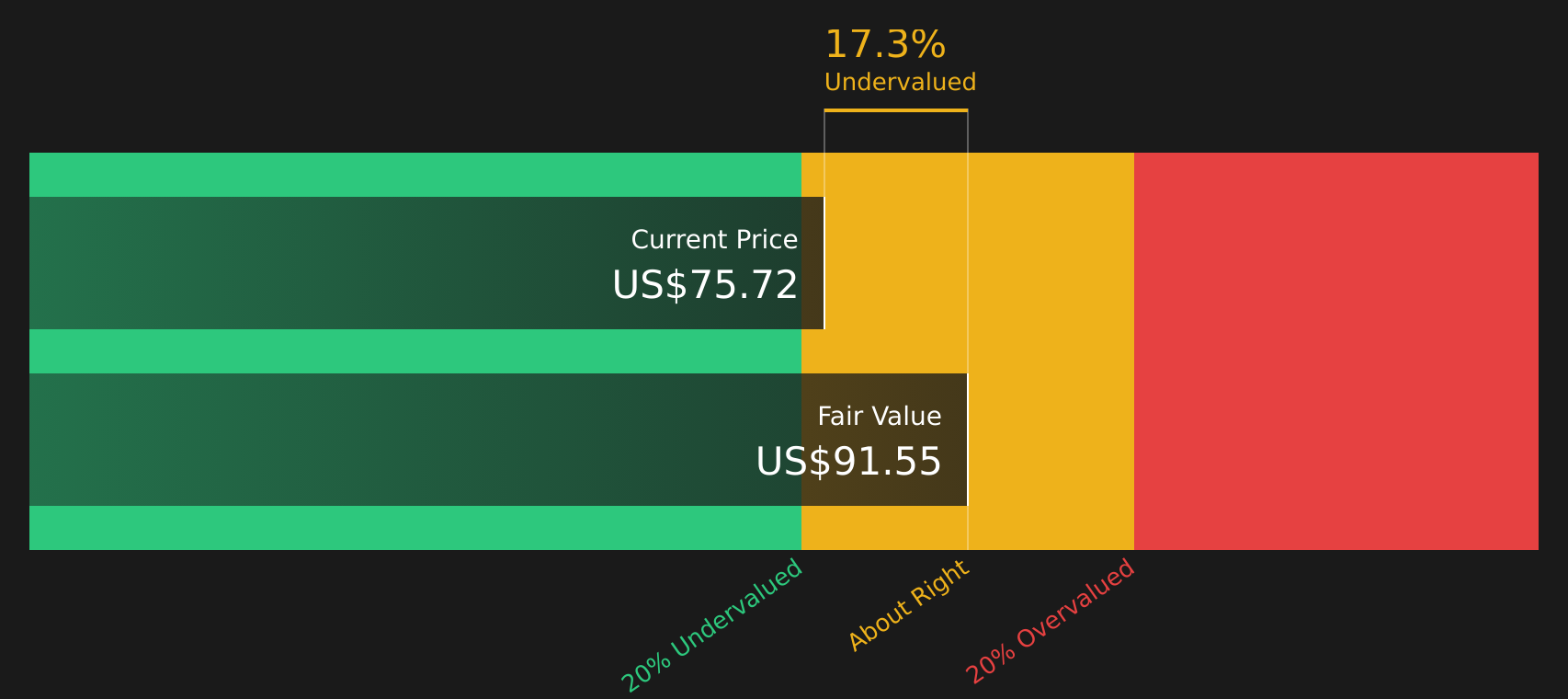

- Wondering if Wyndham Hotels & Resorts at around US$80.90 is offering fair value, a bargain, or something in between? This article walks through the numbers so you can judge for yourself.

- The stock is up 7.5% year to date but has fallen 10.0% over the past month and is down 3.4% over the past year. These moves can change how investors think about both its potential and its risks.

- Recent coverage has focused on Wyndham Hotels & Resorts as a key branded hotel player, with attention on how it manages its portfolio of properties and franchise relationships. Investors are watching how these business updates line up with the share price moves over the short and longer term.

- Right now the Simply Wall St value score for Wyndham Hotels & Resorts is 1 out of 6. The next step is to walk through how that score is built using methods like discounted cash flow, multiples and peer comparisons, and then finish with a broader way to think about valuation that goes beyond a single number.

Wyndham Hotels & Resorts scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Wyndham Hotels & Resorts Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and discounts them back to today’s dollars, aiming to estimate what the entire business could be worth right now.

For Wyndham Hotels & Resorts, the model used is a 2 Stage Free Cash Flow to Equity approach, working from last twelve months free cash flow of about $305.8 million. Analyst estimates and Simply Wall St extrapolations indicate free cash flow of $382.2 million in 2026 and $387.0 million by 2028, with further projections through 2035 all converted into today’s value.

When all these projected cash flows are discounted back, the model gives an estimated intrinsic value of $68.67 per share. Compared with the recent share price of about $80.90, the DCF output suggests the stock is trading around 17.8% above this estimate, which indicates that the shares appear overvalued on this specific cash flow model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Wyndham Hotels & Resorts may be overvalued by 17.8%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Wyndham Hotels & Resorts Price vs Earnings

For a profitable company like Wyndham Hotels & Resorts, the P/E ratio is a useful way to relate what you pay for the stock to the earnings it generates. In simple terms, higher growth expectations and lower perceived risk can justify a higher P/E, while slower growth and higher risk usually point to a lower, more cautious P/E range.

Wyndham Hotels & Resorts is trading on a P/E of 31.38x. That sits above the Hospitality industry average of 20.01x and also above the peer group average of 25.47x, which may suggest the stock is priced more expensively than many competitors on an earnings basis.

Simply Wall St’s Fair Ratio for Wyndham Hotels & Resorts is 25.67x. This is a proprietary estimate of what a reasonable P/E might be, given factors such as the company’s earnings growth profile, its industry, profit margins, market cap and specific risks. Because it adjusts for these elements, the Fair Ratio can be more tailored than a simple comparison with peers or the overall industry.

Comparing the Fair Ratio of 25.67x with the current P/E of 31.38x points to the stock trading above this tailored fair value range.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Wyndham Hotels & Resorts Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives take your view of Wyndham Hotels & Resorts, link its business story to a set of revenue, earnings and margin forecasts, convert that into a Fair Value, and then keep updating that view on Simply Wall St’s Community page as new information arrives. This allows you to compare Fair Value with the current share price and see, for example, how one investor might set a Fair Value around US$105.80, while another aligns closer to the more cautious US$71.00 or the more optimistic US$115.00. It is an easy tool that helps you decide whether the stock appears attractively or richly priced for your own preferred story.

For Wyndham Hotels & Resorts, here are previews of two leading Wyndham Hotels & Resorts narratives:

Fair value used in this bullish narrative: US$105.80

Implied valuation gap vs last close around US$80.90: about 23.5% below the narrative fair value, so the stock is framed as undervalued in this view.

Revenue growth assumption used in this narrative: 13.23%

- Highlights Wyndham’s asset light franchising model across about 8,300 hotels and 847,000 rooms in over 100 countries, with fees and royalties at the core of the business.

- Emphasises high margins, a large and growing loyalty base of around 120 million members and ancillary revenue from co branded cards as key supports for profitability.

- Points to a sizeable development pipeline, ongoing share repurchases and dividends as reasons the author sees fair value at US$105.80.

Fair value used in this bearish narrative: US$71.00

Implied valuation gap vs last close around US$80.90: about 13.9% above the narrative fair value, so the stock is framed as overvalued in this view.

Revenue growth assumption used in this narrative: 4.05%

- Focuses on the risk that a softer U.S. economy and midscale RevPAR, plus slower progress back to a 2% to 3% RevPAR trend, could hold back fee related revenue and EBITDA growth.

- Flags potential pressure on margins and cash flow if technology spending, development advances and exposure to lower RevPAR regions are not fully offset by higher FeePAR and ancillary income.

- Builds a fair value of US$71.00 using analyst assumptions for mid single digit revenue growth, margin expansion, share count reductions and a future P/E of 14.8x.

Do you think there's more to the story for Wyndham Hotels & Resorts? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.