Is It Time To Reassess ZTO Express (NYSE:ZTO) After Its Recent Share Price Strength

ZTO Express (Cayman) Inc. Sponsored ADR Class A ZTO | 0.00 |

- Wondering whether ZTO Express (Cayman), at around US$25.73, is still offering value or already pricing in high expectations? This article walks you through what the current valuation actually signals.

- The stock has returned 2.5% over the last 7 days, 6.9% over the last 30 days, 19.9% year to date, 39.1% over 1 year, 2.2% over 3 years, and has declined 10.0% over 5 years, giving plenty of data points for you to weigh short-term enthusiasm against a longer track record.

- Recent market attention on large-cap logistics names, changing investor views on Chinese American depositary receipt listings, and ongoing discussion around parcel volume trends in China have all added context to ZTO Express (Cayman)'s price moves. These themes provide useful background when assessing whether the current share price lines up with what you think the business is worth.

- ZTO Express (Cayman) currently has a valuation score of 5 out of 6. The next sections break down how different valuation methods arrive at that result and point to a broader way of thinking about valuation that ties everything together later on.

Approach 1: ZTO Express (Cayman) Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash ZTO Express (Cayman) is expected to generate in the future and then discounts those cash flows back to today to estimate what the business might be worth now.

For ZTO, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow sits at about CN¥5.0b. Analysts provide explicit forecasts up to a point, with Simply Wall St extending the curve so that projected free cash flow reaches CN¥15.8b in 2035, all kept in the reporting currency, CN¥.

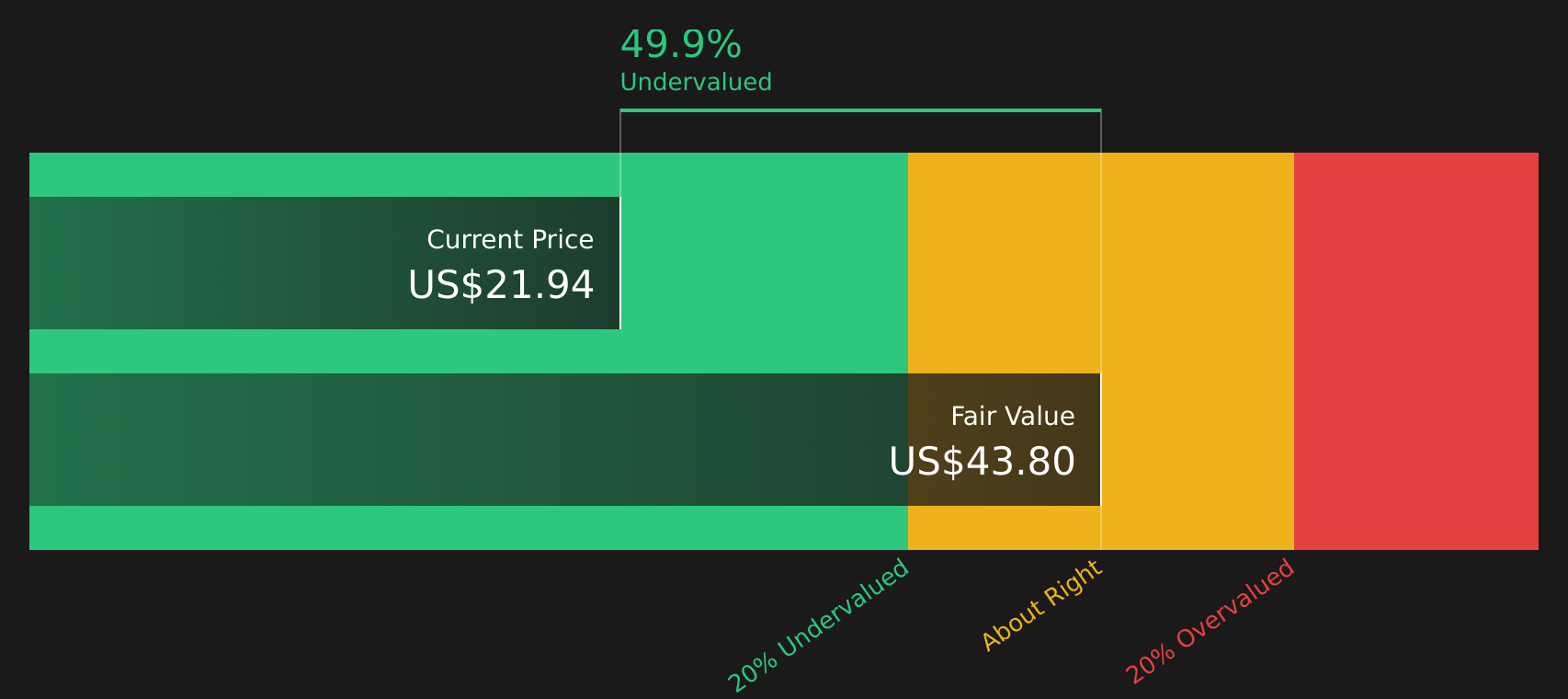

When those projected cash flows are discounted back and summed, the DCF output suggests an intrinsic value of about US$42.56 per share. Compared with the recent share price of around US$25.73, this implies that the stock trades at a 39.5% discount to this DCF estimate, indicating a sizable difference between the market price and this cash flow based value marker.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ZTO Express (Cayman) is undervalued by 39.5%. Track this in your watchlist or portfolio, or discover 54 more high quality undervalued stocks.

Approach 2: ZTO Express (Cayman) Price vs Earnings

For a profitable business, the P/E ratio is a useful shorthand because it links what you pay per share to the earnings that support that price. Investors usually accept a higher P/E when they expect stronger growth or perceive lower risk, and a lower P/E when growth expectations are more modest or risks feel higher.

ZTO Express (Cayman) currently trades on a P/E of 14.8x. That is below both the Logistics industry average of 16.1x and the broader peer average of 24.5x, suggesting the market is applying a more conservative earnings multiple to ZTO than to many similar companies.

Simply Wall St’s Fair Ratio for ZTO is 18.9x. This is a proprietary P/E estimate that reflects factors such as the company’s earnings growth profile, industry, profit margins, market capitalization and risk characteristics. Because it blends these elements, the Fair Ratio can be more tailored than a simple comparison with industry or peer averages, which do not adjust for differences in quality, size or risk.

Comparing the current 14.8x P/E to the 18.9x Fair Ratio suggests the shares are trading below this fair multiple marker.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your ZTO Express (Cayman) Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced, which let you attach a simple story about ZTO Express (Cayman)'s future to hard numbers like fair value, revenue, earnings and margin estimates, then link that story to a financial forecast and a fair value that you can compare with the current share price to decide whether you see the stock as priced attractively or not.

On Simply Wall St's Community page, Narratives are presented as an easy tool used by millions of investors. You can choose or adapt a view that fits how you see the business and instantly see what that implies for fair value versus the current price.

Narratives also update when new information such as earnings, guidance, buyback announcements or news is incorporated into the underlying assumptions, so the story and the numbers stay aligned rather than becoming stale.

For ZTO Express (Cayman), for example, one bullish Narrative currently assumes a fair value of about US$31.38 based on higher revenue growth, margin and P/E assumptions. A more cautious Narrative sits nearer US$23.81, which shows how two investors looking at the same company can reasonably land on quite different fair values using the same framework.

For ZTO Express (Cayman) however we will make it really easy for you with previews of two leading ZTO Express (Cayman) Narratives:

Fair value in this bullish narrative: US$31.38

Implied discount to this fair value versus the recent US$25.73 price: about 18% undervalued

Revenue growth assumption: about 14.69% a year

- Assumes parcel volume growth, automation and AI driven cost efficiencies, and deeper e commerce partnerships can support higher earnings and profitability over time.

- Builds in ongoing share buybacks and a modest lift in the P/E ratio to 14.9x by 2029, which together support the US$31.38 fair value marker.

- Flags execution risks around pricing pressure, capital spending, labor costs and reliance on a few large customers, which could challenge this more upbeat view if they play out less favorably.

Fair value in this cautious narrative: US$23.81

Implied premium to this fair value versus the recent US$25.73 price: about 8% overvalued

Revenue growth assumption: about 9.52% a year

- Frames slower e commerce growth, price competition and a higher mix of low value parcels as constraints on revenue expansion and long run earnings strength.

- Assumes a lower 12.8x P/E by 2029 with earnings of CN¥12.4b, which pulls the indicated fair value down to US$23.81.

- Acknowledges that technology investment, cost control and strong client relationships could still support efficiency and resilience, which would work against the more pessimistic case.

If you want to see how all the detailed assumptions, risks and supporting data line up behind these cases, you can review the full set of ZTO Express (Cayman) narratives side by side on Simply Wall St To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for ZTO Express (Cayman) on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for ZTO Express (Cayman)? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.