Is It Time To Reconsider East West Bancorp (EWBC) After Strong Multi Year Share Gains

East West Bancorp, Inc. EWBC | 108.99 | -0.31% |

- If you are wondering whether East West Bancorp is offering fair value at its current share price, this breakdown will help you connect the recent share performance with what the fundamentals suggest.

- The stock last closed at US$118.46, with returns of 3.5% over the past 7 days, 0.7% over 30 days, 3.0% year to date, 19.1% over 1 year, 65.5% over 3 years, and 103.0% over 5 years. This naturally raises questions about what is already reflected in the price.

- Recent news coverage around US regional banks has largely centered on balance sheet resilience, asset quality and how management teams are positioning for credit conditions. All of this shapes how investors think about risk and value. For East West Bancorp, these themes help explain why the market is paying close attention to how its fundamentals compare with the current share price.

- On our framework of 6 valuation checks, East West Bancorp earns a valuation score of 4. Below, we unpack this using different valuation approaches before turning to a broader way of thinking about what the market might be pricing in.

Approach 1: East West Bancorp Excess Returns Analysis

The Excess Returns model looks at how much value a bank can create over and above the return that equity investors require. Instead of focusing on cash flows, it asks whether each dollar of equity is earning more than its cost, and how long that pattern can reasonably continue.

For East West Bancorp, the model works off a Book Value of US$64.68 per share and a Stable EPS of US$11.36 per share, based on weighted future Return on Equity estimates from 11 analysts. That translates into an Average Return on Equity of 14.83%, compared with a Cost of Equity of US$5.35 per share. The gap between the earnings generated and that cost, the Excess Return, is US$6.02 per share.

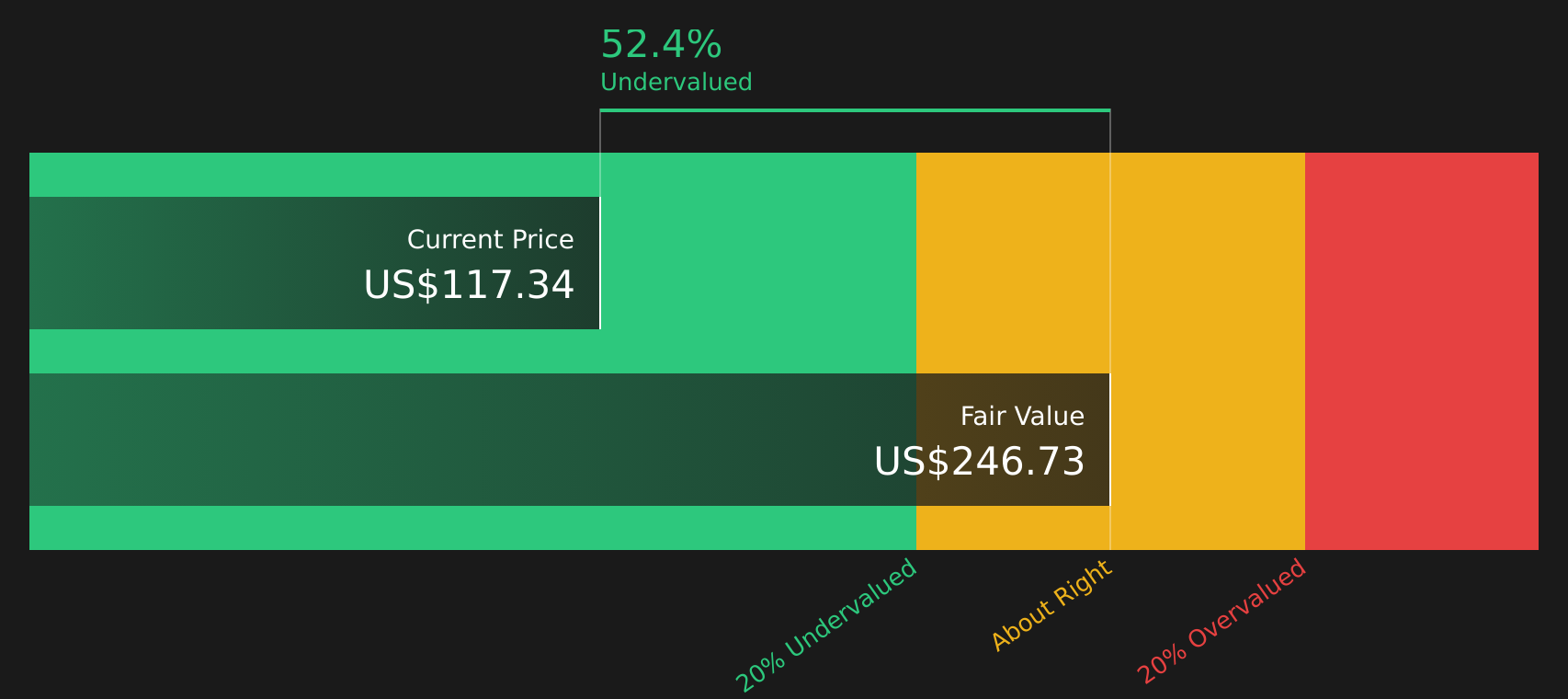

The analysis also uses a Stable Book Value of US$76.61 per share, based on estimates from 8 analysts, to project how these excess returns might compound over time. When those future excess earnings are added to today’s equity base, the model arrives at an intrinsic value of roughly US$245.20 per share.

Against the recent share price of US$118.46, this indicates the stock is about 51.7% undervalued on this method.

Result: UNDERVALUED

Our Excess Returns analysis suggests East West Bancorp is undervalued by 51.7%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

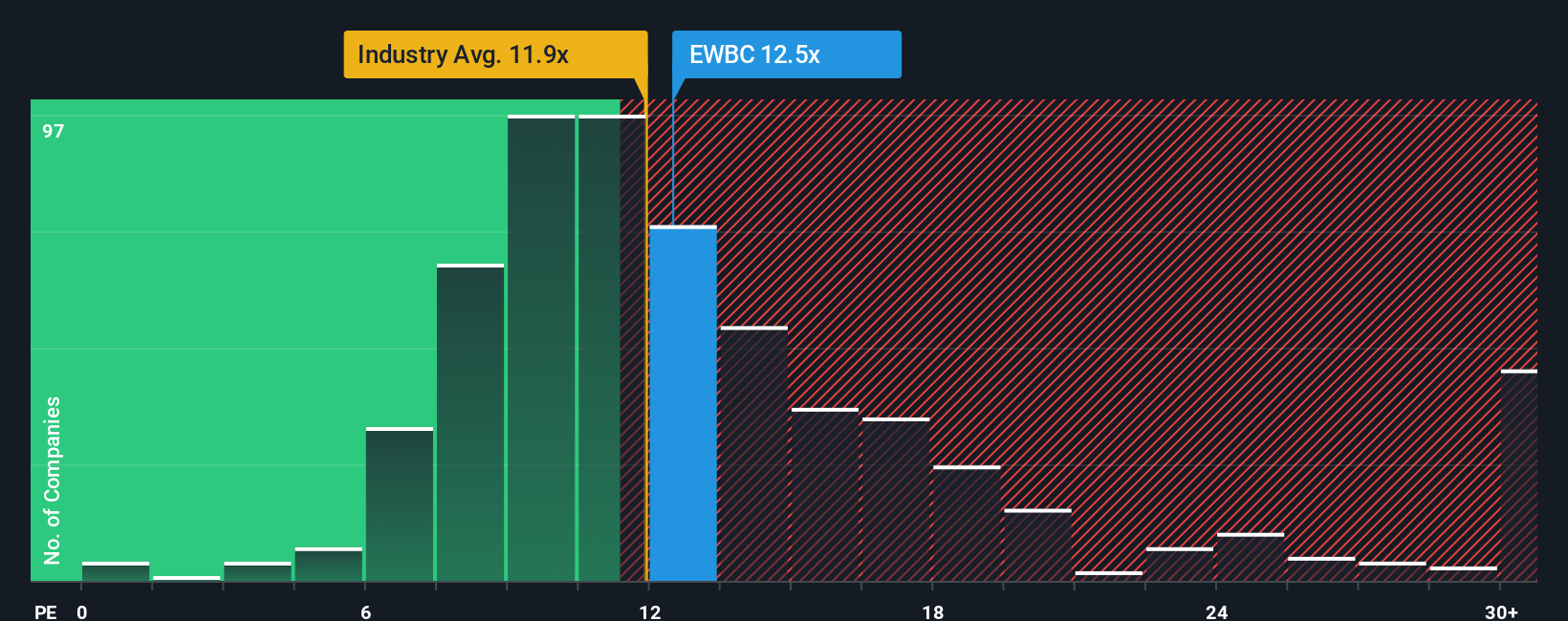

Approach 2: East West Bancorp Price vs Earnings

For a profitable bank, the P/E ratio is a straightforward way to relate what you pay for each share to the earnings that the business is currently generating. It gives you a quick sense of how much investors are willing to pay today for each dollar of earnings.

What counts as a “normal” P/E depends on how the market views a company’s growth prospects and risk profile. Higher expected growth or lower perceived risk can support a higher multiple, while lower growth expectations or higher risk usually lead to a lower one.

East West Bancorp currently trades on a P/E of 12.30x. That sits slightly above the Banks industry average of 11.95x, but below the peer group average of 15.72x. Simply Wall St’s Fair Ratio framework goes a step further by estimating what P/E might be reasonable given factors such as earnings growth, profit margins, industry, market cap and risk, rather than relying only on broad group averages.

In this framework, East West Bancorp’s Fair Ratio is 13.69x, which is higher than the current 12.30x. That gap suggests the shares look undervalued on this earnings based view.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your East West Bancorp Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simply your story about a company tied directly to the numbers you think are reasonable for its future revenue, earnings and margins.

With a Narrative, you connect what you believe about East West Bancorp to a financial forecast and then to an assumed fair value, so you are not just looking at ratios in isolation but at a joined up picture of story, forecast and price.

On Simply Wall St, Narratives sit inside the Community page. They are designed to be quick to set up, easy to adjust and available to millions of investors who want a more structured way to link their views to a value estimate.

Once you have a Narrative, you can compare its fair value to the current share price to help inform whether you want to buy, hold or sell. Your view can update automatically as new earnings releases or news items feed into the underlying data.

For example, one East West Bancorp Narrative might assume a relatively cautious revenue path and arrive at a lower fair value, while another assumes stronger earnings and reaches a higher fair value. This shows how different investors can reasonably disagree yet stay grounded in clear numbers.

Do you think there's more to the story for East West Bancorp? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.