Is It Time To Reconsider First Solar (FSLR) After Its Recent Share Price Recovery?

First Solar, Inc. FSLR | 0.00 |

- Wondering whether First Solar's current price gives you enough value for the risk you are taking? This article focuses squarely on what the numbers say about the stock's valuation.

- First Solar last closed at US$233.37, with the stock showing returns of 6.1% over 7 days, 19.6% over 30 days and 30.8% over 1 year, while the year-to-date return is a decline of 14.9%.

- These moves sit against a backdrop of continued investor attention on solar and semiconductor related stocks, where capital allocation, policy support and competition often influence sentiment. Market commentary has also focused on how current order books, project pipelines and cost trends could affect how investors think about companies such as First Solar.

- On Simply Wall St's valuation framework, First Solar scores a 4 out of 6. This means it screens as undervalued on four of the six checks. Next comes a closer look at what different valuation methods say today, and a way at the end of the article to assess whether those methods tell the full story.

Approach 1: First Solar Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a stock could be worth by projecting its future cash flows and then discounting those back to today using a required rate of return.

For First Solar, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $1.01b. Analysts provide detailed estimates for the next few years, and Simply Wall St extends those out to 2035 using its own assumptions.

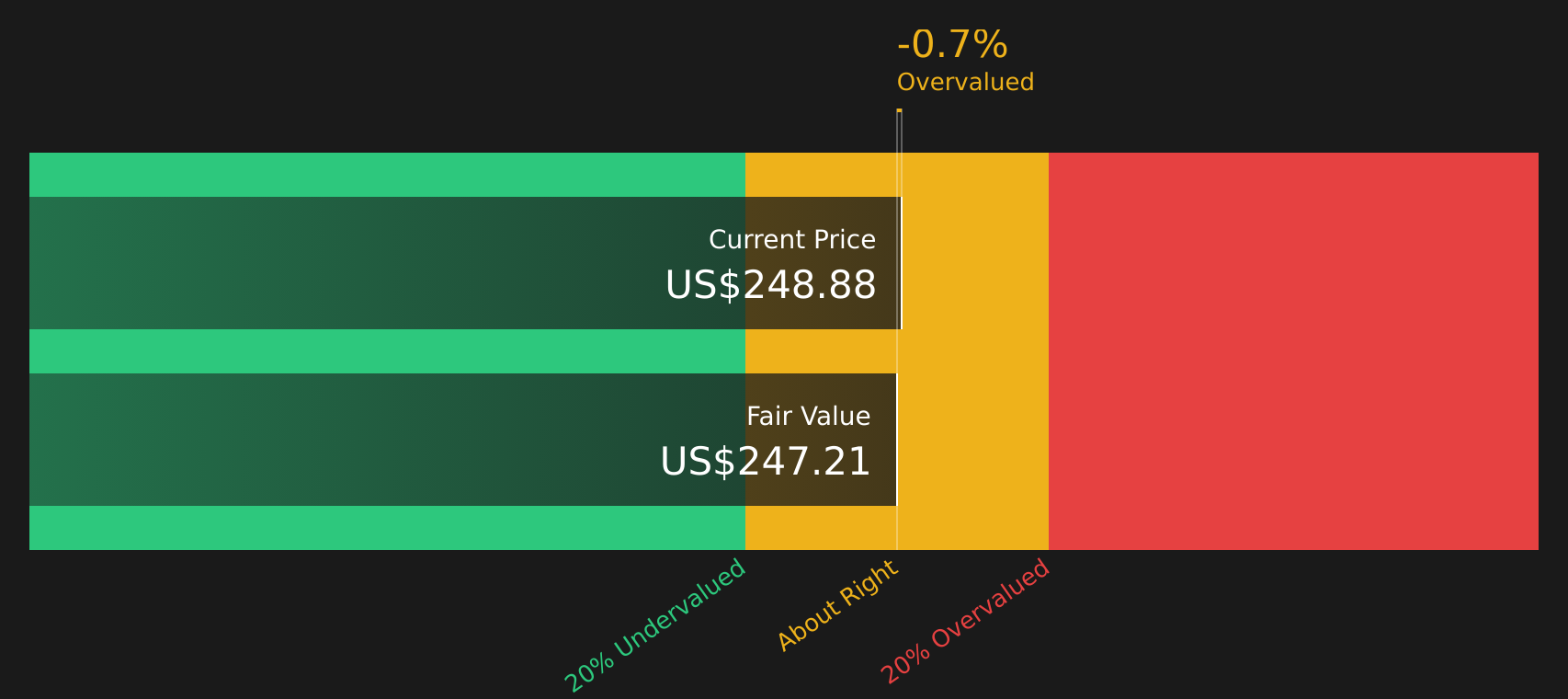

Within these projections, free cash flow is expected to be $2.94b in 2030, with a series of intermediate years that include both relatively small projected outflows and larger inflows. These yearly cash flows are discounted back to today and summed to arrive at an estimated intrinsic value per share of $246.65.

Against the recent share price of $233.37, this implies the stock trades at a 5.4% discount to the DCF estimate, which sits in a fairly tight band around the current market price.

Result: ABOUT RIGHT

First Solar is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

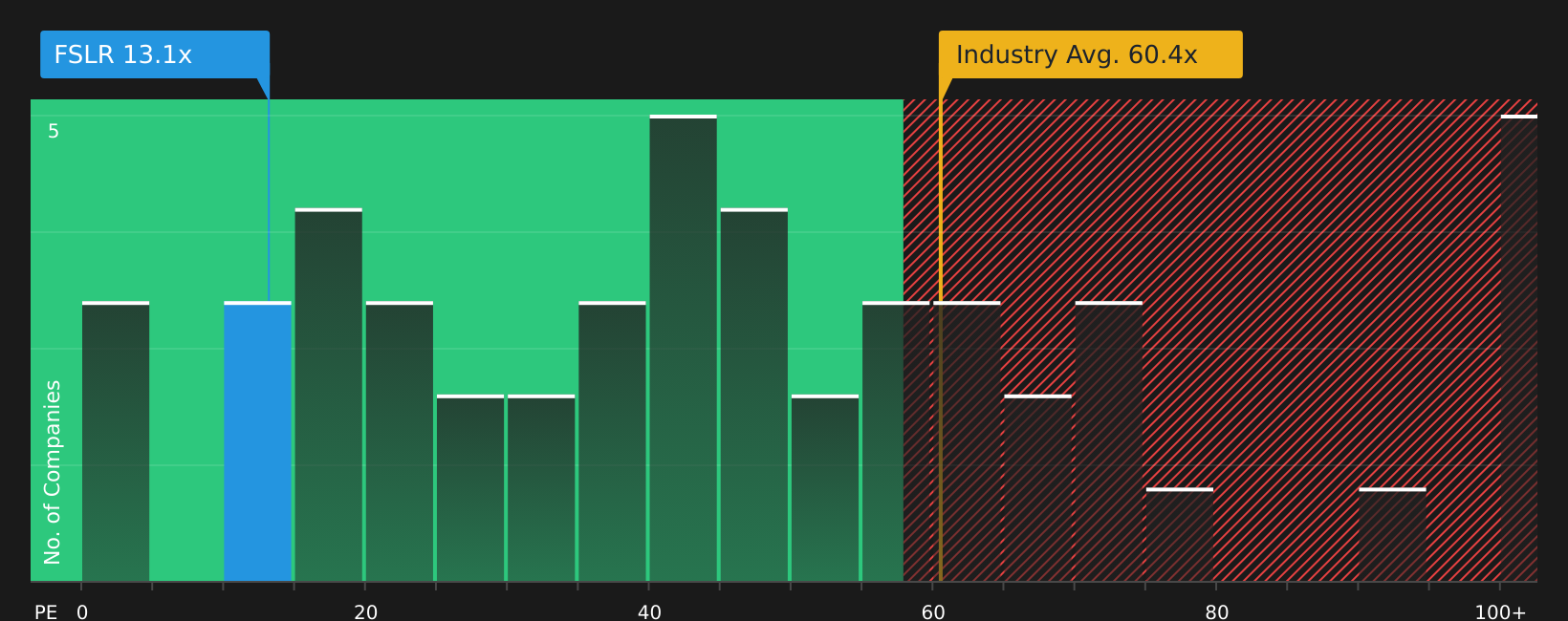

Approach 2: First Solar Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It ties the share price directly to earnings power, which is usually the main driver of long term returns for established businesses.

What counts as a “normal” P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth and lower perceived risk often justify a higher multiple, while slower growth or higher risk usually point to a lower one.

First Solar currently trades on a P/E of 15.06x, compared with the Semiconductor industry average of 64.82x and a peer group average of 124.19x. Simply Wall St’s “Fair Ratio” for First Solar is 38.80x. This Fair Ratio is a proprietary estimate of the P/E the stock might trade on, given factors such as its earnings growth profile, profit margins, industry, market cap and key risks. This can give a more tailored anchor than simple peer or industry comparisons.

Comparing the Fair Ratio of 38.80x to the current P/E of 15.06x suggests the stock trades below that level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your First Solar Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in, giving you a simple way to connect your view of First Solar’s story to a set of numbers like future revenue, earnings, margins and a Fair Value that can be compared with today’s share price.

A Narrative on Simply Wall St is your version of that story, written as plain language assumptions plus a forecast. The platform then links this directly to an estimated Fair Value so you can quickly see whether your view points to the stock looking expensive or cheap versus the live market price.

These Narratives sit inside the Community page used by millions of investors, are easy to browse and update, and they automatically refresh when new information such as earnings reports or policy news is added to the underlying data.

For First Solar, one Narrative currently anchors on a Fair Value of about US$155.98, while another uses US$313.00. This shows how two investors can look at the same company, apply different assumptions about revenue growth, profit margins and discount rates, and end up with very different conclusions about whether the stock looks attractively priced or not.

For First Solar however we'll make it really easy for you with previews of two leading First Solar Narratives:

Fair value in this bull case narrative: US$281.65

Current price versus this fair value suggests the stock is trading at about a 17.2% discount on this view.

Revenue growth assumption used in this narrative: 12.54% a year.

- Emphasis on U.S. policy support, domestic manufacturing build out and trade measures that support demand visibility and pricing for First Solar's modules.

- Analyst forecasts point to higher revenue, wider profit margins and a fair value above the recent share price, with a view that the stock is close to fairly priced against the consensus target.

- Key risks are around trade policy shifts, competition, technology changes and customer credit quality, which could affect earnings and cash flow against these projections.

Fair value in this bear case narrative: US$180.44

Current price versus this fair value suggests the stock is trading at about a 29.3% premium on this view.

Revenue growth assumption used in this narrative: 13.00% a year.

- Focus on strong end market demand for PV panels, U.S. manufacturing benefits and thin film technology, but with more conservative conclusions about what that is worth per share.

- Highlights positive factors such as cash exceeding debt, high forecast growth and policy support, but also flags that returns rely heavily on subsidies and protective tariffs.

- Flags risks around possible policy rollbacks, raw material constraints, operational challenges and competitor pricing that could cap the valuation investors are willing to pay.

These two Narratives sit at different ends of the fair value range. This is the sort of spread you want to see before deciding which assumptions feel closer to your own view of the stock's risks and rewards.

To see how these results tie into long term growth, risks and valuation, check out the full range of To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for First Solar on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for First Solar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.