Is It Time To Reconsider Quest Diagnostics (DGX) After Recent Testing Demand Headlines?

Quest Diagnostics Incorporated DGX | 0.00 |

- If you are wondering whether Quest Diagnostics stock offers solid value at today's price, it is helpful to see how the market price compares with a few different valuation checks.

- The stock last closed at US$193.16, with returns of 0.1% over 7 days, 0.3% over 30 days, 11.1% year to date, 13.3% over 1 year, 54.0% over 3 years and 67.0% over 5 years. This provides useful context before considering what the business might be worth.

- Recent news has continued to focus on Quest Diagnostics' position as a major US healthcare provider, with attention on how testing demand and industry competition may influence long term expectations for the stock. Investors often watch this kind of news closely because it can help explain why the share price moves even when headline financial data is not in focus.

- On Simply Wall St's 6 point valuation checklist, Quest Diagnostics has a value score of 5. The next step is to compare what different valuation methods suggest the stock is worth, before turning to a more complete way to think about valuation later in the article.

Approach 1: Quest Diagnostics Discounted Cash Flow (DCF) Analysis

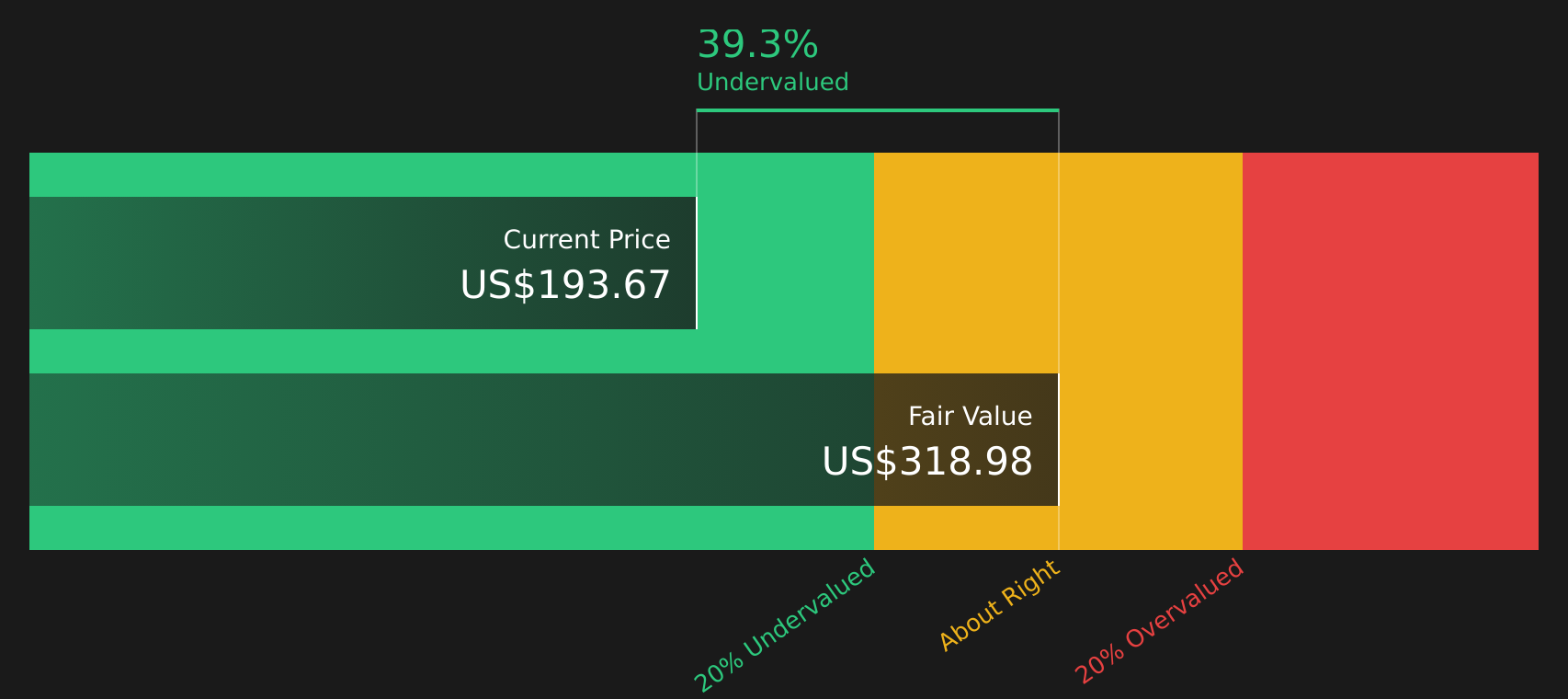

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth by projecting the cash the company could generate in the future and then discounting those cash flows back to today.

For Quest Diagnostics, the model used is a 2 Stage Free Cash Flow to Equity approach. The company’s latest twelve month free cash flow is about $1.36b. Analyst and extrapolated projections from Simply Wall St point to free cash flows between roughly $1.33b and $1.70b over the next decade, with $1.55b to $1.70b in the later years of that period.

After discounting those projected cash flows back to today, the model arrives at an estimated intrinsic value of $318.98 per share. Compared with the recent share price of $193.16, this points to an implied discount of 39.4%. In this model, the stock screens as undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Quest Diagnostics is undervalued by 39.4%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Quest Diagnostics Price vs Earnings

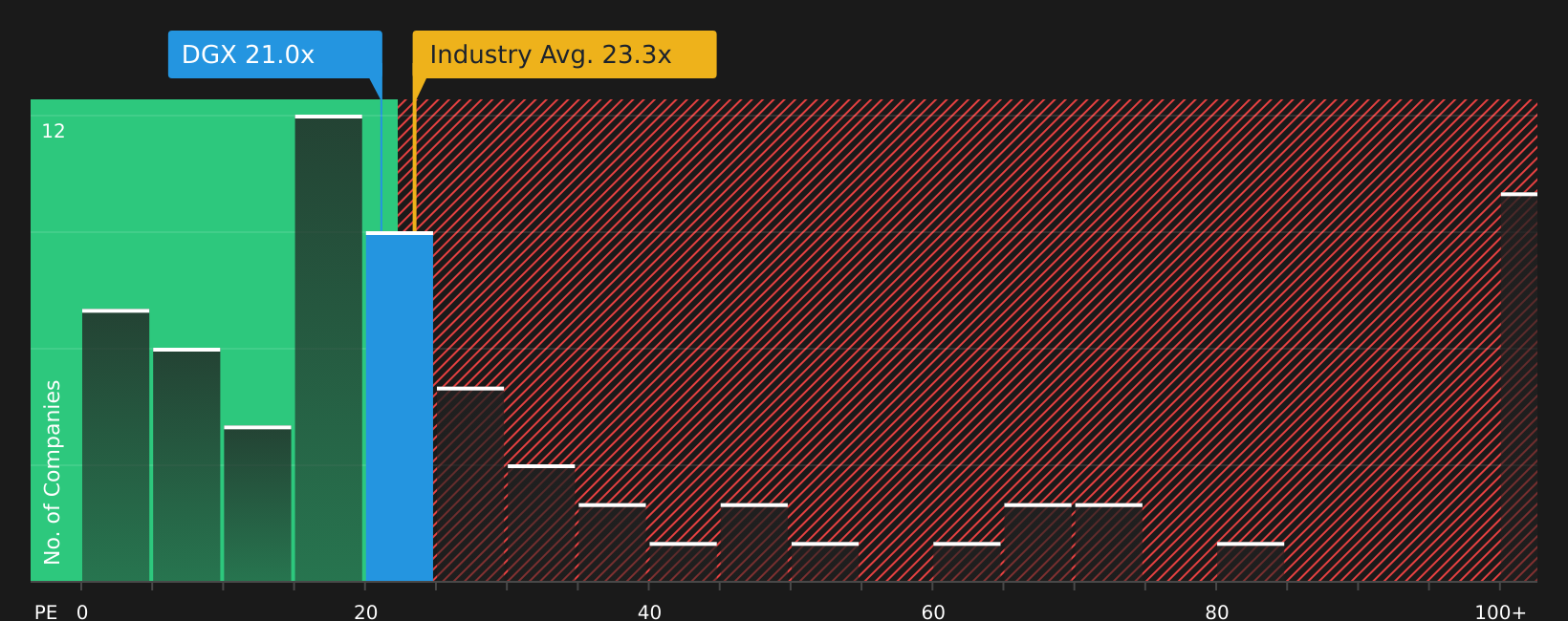

P/E is a common way to value profitable companies because it links what you pay for the stock to the earnings the business is already generating. In general, higher growth expectations and lower perceived risk can support a higher P/E ratio. Slower expected growth or higher risk usually lines up with a lower, more conservative P/E.

Quest Diagnostics currently trades on a P/E of 20.96x. This sits below the Healthcare industry average P/E of about 23.22x and also below the peer group average of 32.74x. On those simple comparisons, the stock screens as cheaper than both its industry and peer set.

Simply Wall St’s Fair Ratio for Quest Diagnostics is 22.92x. This is a proprietary estimate of what the P/E might reasonably be given factors such as the company’s earnings growth profile, industry, profit margins, market value and key risks. Because it adjusts for these fundamentals, the Fair Ratio can be more informative than a plain comparison with broad industry or peer averages.

Comparing the Fair Ratio of 22.92x to the current P/E of 20.96x suggests the stock trades below this implied fair level. On this measure it looks undervalued.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Quest Diagnostics Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple way for you to set out your story for Quest Diagnostics by linking your view on its future revenue, earnings and margins to a forecast, a Fair Value and then a clear comparison with today’s share price.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors where you can see, adjust and compare these story driven forecasts. They automatically update when new information such as earnings releases or major news is added to the platform.

For Quest Diagnostics, one investor might build a Narrative close to the more bullish analyst view, with a Fair Value around US$245 based on assumptions about revenue reaching US$13.0b, earnings of US$1.4b by about 2029 and a future P/E near 21.4x. Another might lean toward the more cautious US$184 fair value, highlighting risks around reimbursement, payer mix and competition. Your own stance can sit anywhere along that spectrum depending on how you interpret the same set of facts.

Do you think there's more to the story for Quest Diagnostics? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.