Is It Time To Reconsider WEX (WEX) After Its Recent Share Price Pause?

WEX Inc. WEX | 154.69 | +2.88% |

- If you are wondering whether WEX at around US$157 per share still offers value, looking closely at what you are paying for each dollar of its business is a useful place to start.

- The stock has been relatively muted recently, with a 0.8% decline over the last 7 days and a 2.3% decline over the last 30 days, while year to date it is up 6.3% and 1 year returns sit at 1.9% against weaker 3 year and 5 year returns of 18.0% and 28.7% declines.

- Recent coverage of WEX has focused on keeping investors updated as part of ongoing, evergreen analysis of the stock, rather than being driven by a single one off announcement. In that context, it can be a good moment to step back and look at how the current share price lines up with a range of valuation checks.

- On Simply Wall St's valuation model, WEX scores 2 out of 6 on its value checks, as shown in the valuation score. Next, we will compare what different methods say about the stock, and then point you to a more holistic way to think about valuation at the end of this article.

WEX scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: WEX Excess Returns Analysis

The Excess Returns model looks at how much value WEX creates over and above the return that shareholders are expected to require, and then capitalises those extra profits into an estimated intrinsic value per share.

For WEX, the inputs are quite punchy. Book value is $35.89 per share, while stable earnings per share are estimated at $24.02, based on weighted future Return on Equity estimates from 5 analysts. That implies an average Return on Equity of 40.50% on a stable book value of $59.31 per share, which comes from weighted future book value estimates from 4 analysts.

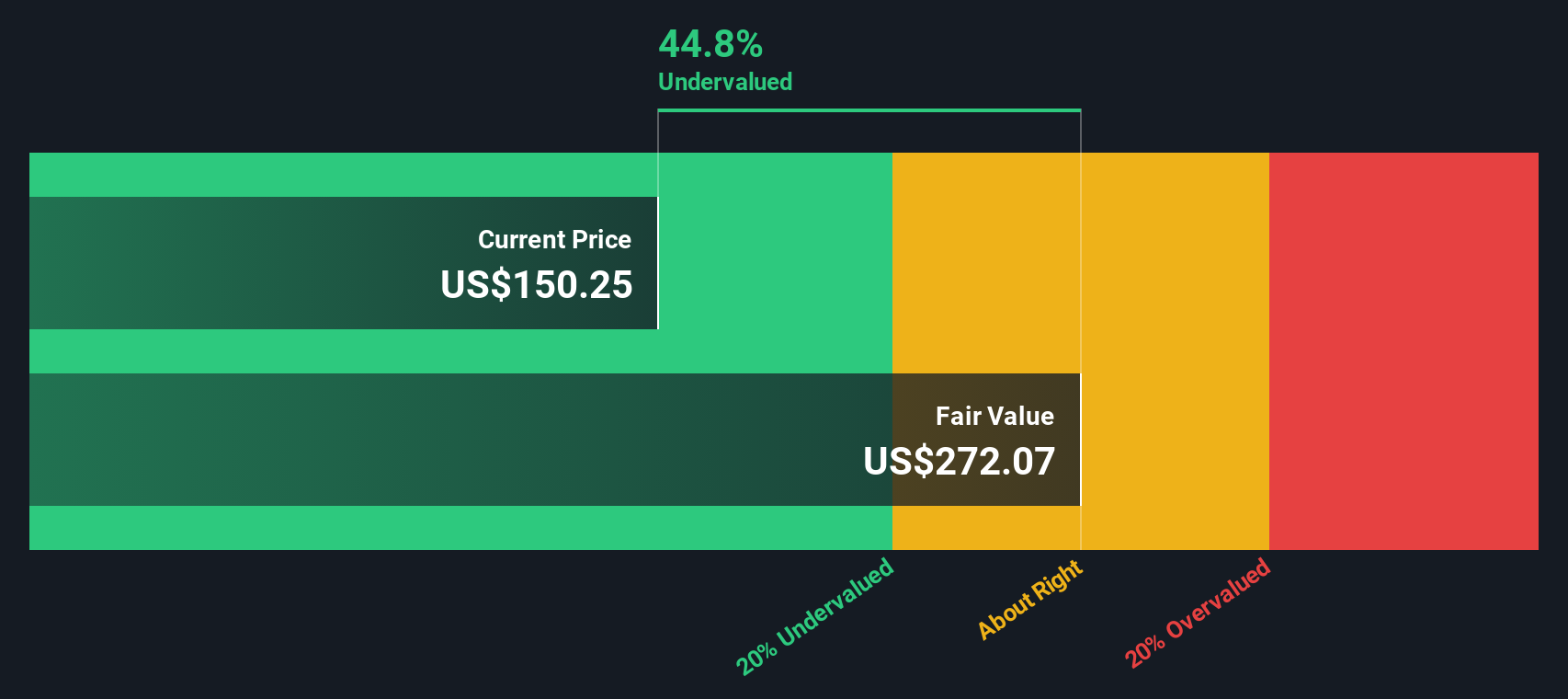

The model uses a cost of equity of $5.29 per share and an excess return of $18.73 per share, which reflects what is left after covering that equity cost. Aggregating these excess returns gives an Excess Returns fair value of about $398.98 per share.

Compared with the current share price of around $157, this valuation suggests the stock is roughly 60.5% undervalued on this approach.

Result: UNDERVALUED

Our Excess Returns analysis suggests WEX is undervalued by 60.5%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: WEX Price vs Earnings

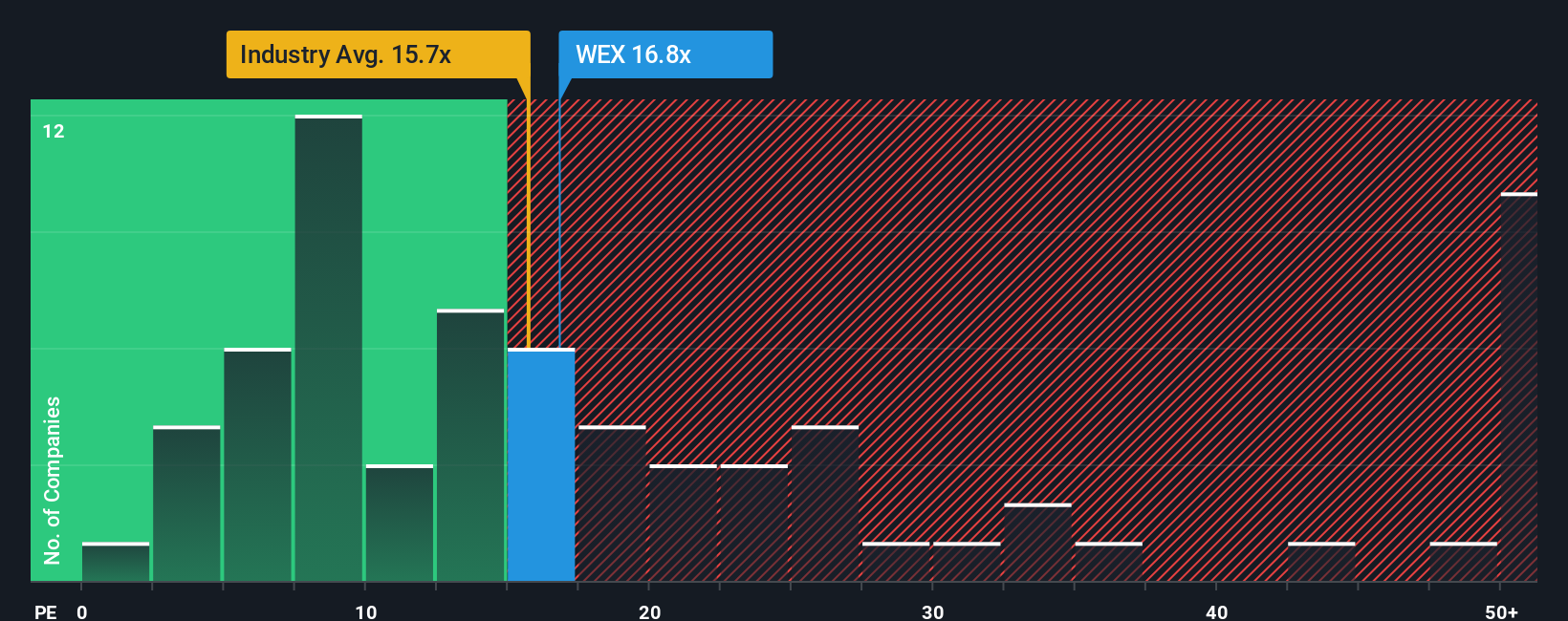

For a profitable company like WEX, the P/E ratio is a useful shorthand for what the market is paying for each dollar of earnings. It connects directly to what ultimately matters, the earnings that support the share price, and is widely used, which makes comparisons straightforward.

In practice, a higher or lower P/E often reflects what investors expect for future earnings and how much risk they see in those earnings. Stronger expected growth or lower perceived risk can support a higher P/E, while weaker expectations or higher risk usually go with a lower multiple.

WEX currently trades on a P/E of 17.78x. That sits above the Diversified Financial industry average of 16.02x and also above the peer group average of 14.89x. Simply Wall St's proprietary Fair Ratio for WEX is 16.78x, which is an estimate of what the P/E might be given factors such as earnings growth, profit margins, industry, market cap and company specific risks.

This Fair Ratio is more tailored than a simple industry or peer comparison because it adjusts for those company specific characteristics rather than treating all Diversified Financial stocks as the same. With the current 17.78x P/E sitting above the 16.78x Fair Ratio, the multiple on WEX appears slightly rich on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your WEX Narrative

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St this comes through Narratives, where you spell out your story for WEX by linking your assumptions for future revenue, earnings and margins to a forecast and an implied fair value, then compare that fair value with the current share price to decide whether the stock looks interesting to you.

You can access these Narratives on the WEX Community page. They update automatically when new information such as news, guidance or earnings is added, so your view does not stay frozen while the facts move on.

For WEX today, one investor might align with the bullish Narrative that points to a fair value of about US$210.00. Another might sit closer to the cautious Narrative around US$130.00. By seeing those stories side by side you can decide which assumptions feel closest to your own and what that means for your next move.

For WEX however we will make it really easy for you with previews of two leading WEX Narratives:

Fair value: US$173.60

Implied discount to this fair value: 9.2% compared to the last close of US$157.67

Assumed annual revenue growth: 4.62%

- Analysts in this camp see WEX benefiting from broader digital payments adoption, product investment and partnerships that support revenue growth and margin expansion across fleets, corporate payments and benefits.

- They expect earnings and earnings per share to rise as margins move higher and the share count trends lower, with a 2028 P/E of 14.5x used to anchor the narrative fair value around US$173.60.

- The key watchpoints they call out include competition, regulation, the shift to electric vehicles and execution on international growth, which could all affect how close reality comes to these assumptions.

Fair value: US$130.00

Implied premium to this fair value: 21.3% compared to the last close of US$157.67

Assumed annual revenue growth: 2.12%

- The more cautious analysts focus on tougher competition, rising compliance and technology costs and pressure on core fleet payments, which they see as limiting WEX's ability to expand margins and justify a higher valuation.

- They work with slower revenue growth, more modest margin gains and a lower 2028 P/E of 12.4x, which together point to a fair value of US$130.00 in their framework.

- On their numbers, exposure to alternative fuels, digital payments rivals, regulatory scrutiny and heavy investment needs are central risks that could hold back earnings and keep returns closer to the lower end of analyst targets.

Do you think there's more to the story for WEX? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.