Is It Time To Revisit Albertsons Companies (ACI) After Recent Share Price Weakness?

Albertsons Companies, Inc. ACI | 17.45 | +2.59% |

- If you are wondering whether Albertsons Companies is offering good value at its current share price, you are not alone. This article is here to unpack that question clearly.

- The stock most recently closed at US$18.57, with returns of 2.7% over the past week, 4.9% over the past month, 7.3% year to date, but an 8.1% decline over the last year and a 5.3% decline over three years, while the five year return sits at 67.6%.

- Recent attention on Albertsons has centered on how its grocery footprint and competitive position fit into the broader US consumer retail sector, with investors weighing up the balance between steady demand for essentials and changing shopping habits. Headlines have also focused on how consolidation interest in the supermarket space and ongoing regulatory discussions shape sentiment around companies like Albertsons.

- Against that backdrop, Albertsons carries a valuation score of 5 out of 6, suggesting it screens as undervalued on most of the checks we will walk through next. We will then finish with a more rounded way to think about its valuation at the end of the article.

Approach 1: Albertsons Companies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimated future cash flows, discounts them back to today using a required return, and sums them to get an estimate of what the business might be worth per share.

For Albertsons Companies, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $384.2 million. Analyst and extrapolated projections suggest free cash flow rising to around $1.4b by 2029, with further estimates out to 2035 provided in thousands of US$. Simply Wall St uses analyst inputs for the earlier years and then extends the trend to build a 10 year cash flow path.

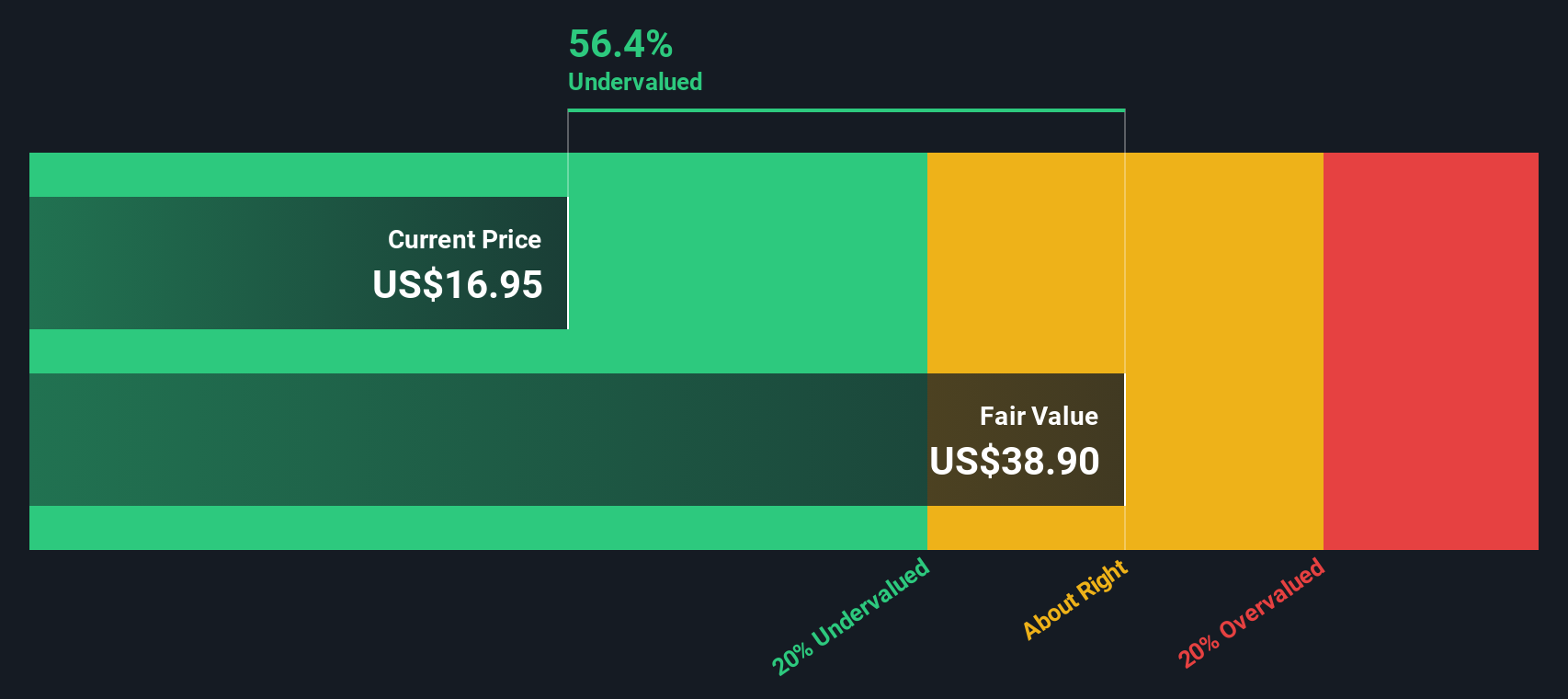

When these projected cash flows are discounted back and combined with an estimate of value beyond the explicit forecast period, the model arrives at an intrinsic value of about $41.30 per share. Compared with the recent share price of $18.57, this implies an intrinsic discount of roughly 55.0%, which indicates that Albertsons screens as materially undervalued according to this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Albertsons Companies is undervalued by 55.0%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Albertsons Companies Price vs Earnings

For profitable companies, the P/E ratio is a useful way to link what you pay for the stock to the earnings the business is already generating. Investors usually accept a higher or lower P/E depending on what they expect for future growth and how risky they think those earnings are.

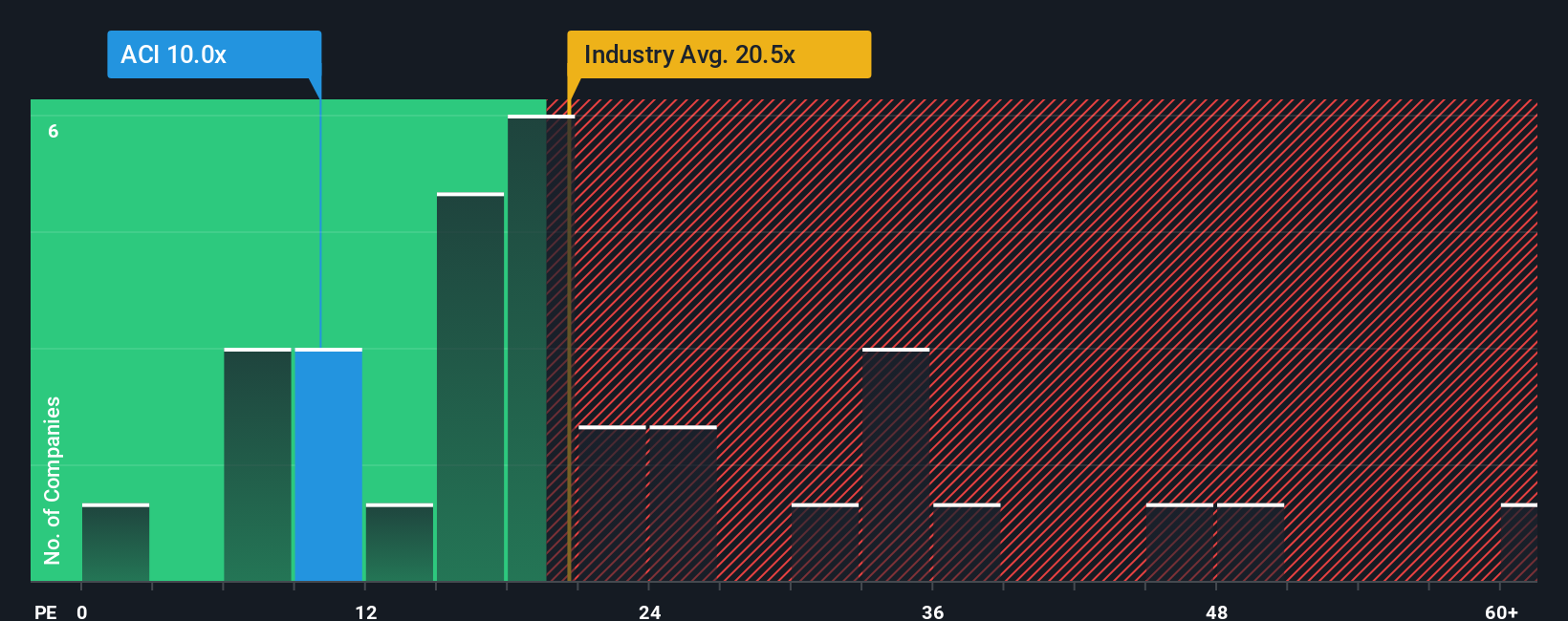

Albertsons Companies currently trades on a P/E of 10.97x. That sits below the Consumer Retailing industry average P/E of 23.38x and also below the broader peer group average of 32.58x, so the stock is priced at a lower multiple of earnings than many peers in its space.

Simply Wall St also calculates a “Fair Ratio” of 18.17x for Albertsons. This is a proprietary estimate of what the P/E might reasonably be, given factors such as the company’s earnings growth profile, profit margins, risk characteristics, industry and market cap. Because it blends these inputs, the Fair Ratio can give a more tailored anchor than a simple comparison with industry or peer averages. With the current P/E of 10.97x sitting below the Fair Ratio of 18.17x, Albertsons screens as undervalued on this P/E-based view.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Albertsons Companies Narrative

Earlier we mentioned that there is an even better way to think about valuation. Let us introduce Narratives, a simple way for you to set out your own story for Albertsons Companies by linking what you believe about its future revenue, earnings and margins to a forecast and a fair value, and then comparing that fair value to today’s price.

On Simply Wall St’s Community page, millions of investors use Narratives as an accessible tool where they plug in assumptions, see how those flow through to future cash flows and valuation, and then use the gap between their Fair Value and the market price to help decide whether the stock looks attractive, fairly priced or expensive to them.

Narratives also refresh as new information arrives. When earnings, news or updated analyst targets come through, the fair value adjusts. This is why one Albertsons Narrative currently anchors to a cautious fair value of about US$14.87, while a more optimistic Narrative points to about US$29.74, reflecting two very different views of how its digital, pharmacy and Own Brands efforts might play out over time.

For Albertsons Companies, however, we will make it really easy for you with previews of two leading Albertsons Companies Narratives:

Fair value in this bullish Narrative: US$22.00 per share

Gap to that fair value versus the last close of US$18.57: around 15.6% below the Narrative fair value

Revenue growth assumption: 1.52% a year

- Analysts backing this view see steady support from digital channels, pharmacy and health services, and a growing loyalty base feeding into revenue and margin resilience over time.

- They factor in modest improvements in profit margins and a future P/E of 11.24x, along with ongoing share buybacks and a 9.91% discount rate to bring future earnings back to today.

- Key watchpoints are e commerce profitability, labor costs, tough grocery competition and the mix effect from pharmacy. All of these could influence whether earnings and valuation reach those targets.

Fair value in this bearish Narrative: about US$14.87 per share

Gap to that fair value versus the last close of US$18.57: around 25.0% above the Narrative fair value

Revenue growth assumption: 0.97% a year

- This view leans on cautious assumptions around food disinflation, value focused shoppers and tighter sector conditions, which feed into slower revenue growth and thinner margins.

- It applies a higher discount rate of 9.77% and a lower future P/E of 8.09x, reflecting more restrained expectations for how much investors might be willing to pay for future earnings.

- Even here, digital investments, media, loyalty and Own Brands are seen as potential offsets. However, the Narrative treats them as not fully compensating for cost pressure and a softer top line.

If you want to go further than these previews and stress test your own view on growth, margins and P/E, you can build and track a narrative yourself or compare against the full range of community views on Albertsons.

Do you think there's more to the story for Albertsons Companies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.