Is It Time To Revisit DraftKings (DKNG) After Recent Share Price Rebound

DraftKings DKNG | 0.00 |

- If you are trying to work out whether DraftKings stock looks attractively priced or too expensive at today’s levels, you will want more than just the latest share price in front of you.

- The stock recently closed at US$25.22, with returns of 8.1% over 7 days and 9.9% over 30 days, while year to date and 1 year returns of negative 29.3% and negative 28.7% show a very different picture over a longer window.

- Recent headlines around DraftKings have largely focused on the broader US sports betting and online gaming sector, including ongoing discussion about competition, regulation and the pace of market expansion. These themes help frame why shorter term share price moves can look very different to the stock’s performance over the past year.

- On Simply Wall St’s 6 point valuation checklist, DraftKings currently scores 3 out of 6. The rest of this article will unpack what that means across different valuation methods, before finishing with a way to think about value that goes beyond any single model.

Approach 1: DraftKings Discounted Cash Flow (DCF) Analysis

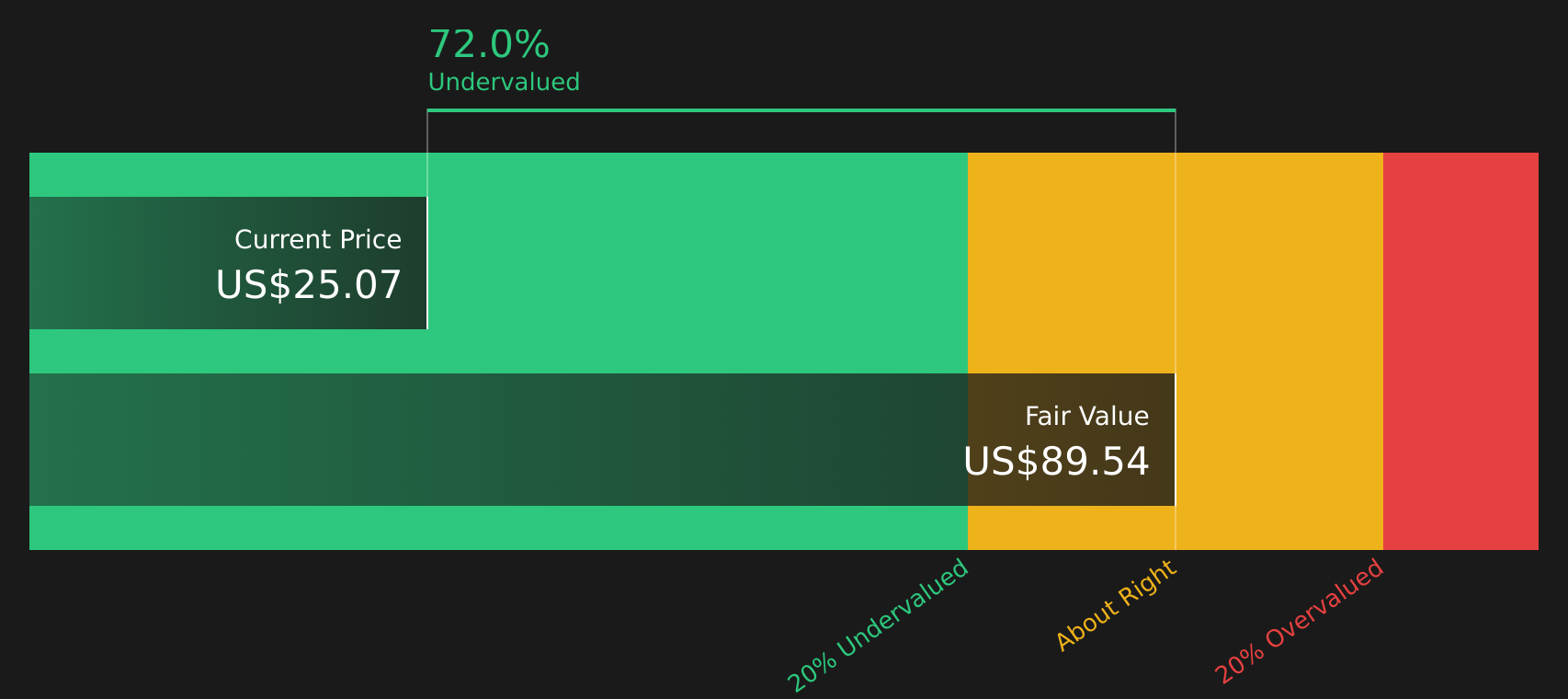

A Discounted Cash Flow, or DCF, projects the cash DraftKings could generate in the future and then discounts those projections back to today to estimate what the stock might be worth right now.

DraftKings currently has last twelve month free cash flow of about $500.4m. Using a 2 Stage Free Cash Flow to Equity model, analysts and Simply Wall St projections point to free cash flow of about $2.49b in 2030, with estimates provided out to 5 years and the remaining years extrapolated.

Pulling all those projected cash flows together and discounting them back to today gives an estimated intrinsic value of $91.56 per share. Compared with the recent share price of $25.22, this DCF implies the stock trades at roughly a 72.5% discount. On this model alone, the shares appear materially undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DraftKings is undervalued by 72.5%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: DraftKings Price vs Sales

For companies where profits are limited or volatile, the P/S ratio is often more useful than P/E because it compares the stock price with the revenue the company is already generating, rather than earnings that can swing around from year to year.

In general, higher expected growth and lower perceived risk can support a higher P/S multiple, while slower growth and higher risk usually point to a lower, more conservative range. So it helps to compare DraftKings with both its sector and peers.

DraftKings currently trades on a P/S ratio of 2.07x. That sits above the Hospitality industry average of 1.66x and also above the peer average of 1.36x, which might look expensive if you only use simple comparisons. Simply Wall St’s Fair Ratio for DraftKings is 3.65x, which reflects a model that factors in elements like growth, profit margins, industry, market value and company specific risks.

Because the Fair Ratio is tailored to the company, it can be more informative than a straight industry or peer comparison. Here, the current 2.07x P/S is below the 3.65x Fair Ratio, which suggests that, on this measure, the stock may be trading at a lower level than that model-based estimate.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your DraftKings Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced as a simple way for you to connect your view of DraftKings with a set of revenue, earnings and margin assumptions that roll into a Fair Value you can compare with the current price, all within the Narratives feature on Simply Wall St’s Community page that is used by millions of investors.

In practice, a Narrative is your story about where the business is heading, tied directly to a financial forecast and a Fair Value estimate that updates when new information such as earnings or news is added. This allows you to quickly see whether your story still fits the latest data.

For DraftKings, one investor might align with a more optimistic Narrative that assumes a Fair Value around US$54.68 with higher revenue growth and profit margins. Another might prefer a more cautious Narrative closer to US$24.00 with slower growth and lower margins. Comparing each Fair Value with the current share price can help you decide whether you see the stock as richly priced, closer to fully valued, or trading below your own expectations.

For DraftKings, however, we will make it really easy for you with previews of two leading DraftKings Narratives:

Fair Value: US$35.95

Implied discount to this Narrative: about 29.8% relative to the recent US$25.22 share price

Revenue growth assumption: 13.7%

- Analysts behind this view see revenue reaching about US$8.9b and earnings of US$904.2m by 2029, with profit margins moving from around 0.1% to 10.1%.

- This Narrative focuses on expansion in legal online sports betting and iGaming, efficiency gains, and proprietary technology to support higher margins and earnings.

- Key risks include higher state taxes, regulatory scrutiny of prediction markets and microbetting, competition, and uncertainty around how quickly new markets can be added.

Fair Value: US$24.00

Implied premium to this Narrative: about 5.1% relative to the recent US$25.22 share price

Revenue growth assumption: 11.2%

- The more cautious analysts behind this view anchor on a Fair Value of US$24.00, based on revenue of about US$8.3b and earnings of US$707.8m by 2029, with margins rising to 8.5%.

- They place more weight on slower market expansion, tighter regulation, higher taxes, and the cost of promotions and prediction market investment, which they see as limiting upside.

- This camp still factors in growth and margin improvement, but views DraftKings as closer to fairly priced at current levels, with less room for disappointment in execution or regulation.

If you want to see how other investors are joining the dots between these types of assumptions, fair values, and risks for DraftKings, check out what the wider community is saying through the full range of Narratives and use them as a benchmark for your own view.

Do you think there's more to the story for DraftKings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.