Is It Time To Revisit eXp World Holdings (EXPI) After Prolonged Share Price Weakness

eXp World Holdings, Inc. EXPI | 6.25 6.25 | +1.63% 0.00% Pre |

- If you are wondering whether eXp World Holdings at around US$7.50 is a bargain or a value trap, you are not alone, and this article is built to help you frame that question clearly.

- The share price is around US$7.50, with returns of 2.7% decline over 7 days, 21.4% decline over 30 days, 17.6% decline year to date, 32.3% decline over 1 year and 41.2% decline over 3 years. This raises fair questions about how the market currently views its prospects and risks.

- Recent news coverage has focused on eXp World Holdings as an online real estate brokerage platform, with attention on how its agent count, transaction volumes and technology‑centric model fit into a competitive housing market. Commentary has also highlighted how these business drivers may be influencing investor sentiment and price moves, even when short term headlines are mixed.

- On our checks, eXp World Holdings posts a valuation score of 4 out of 6. This suggests some aspects look potentially cheap while others are more in line with the current share price. Next we will walk through the usual valuation tools before finishing with a broader way to think about what the business might be worth.

Approach 1: eXp World Holdings Discounted Cash Flow (DCF) Analysis

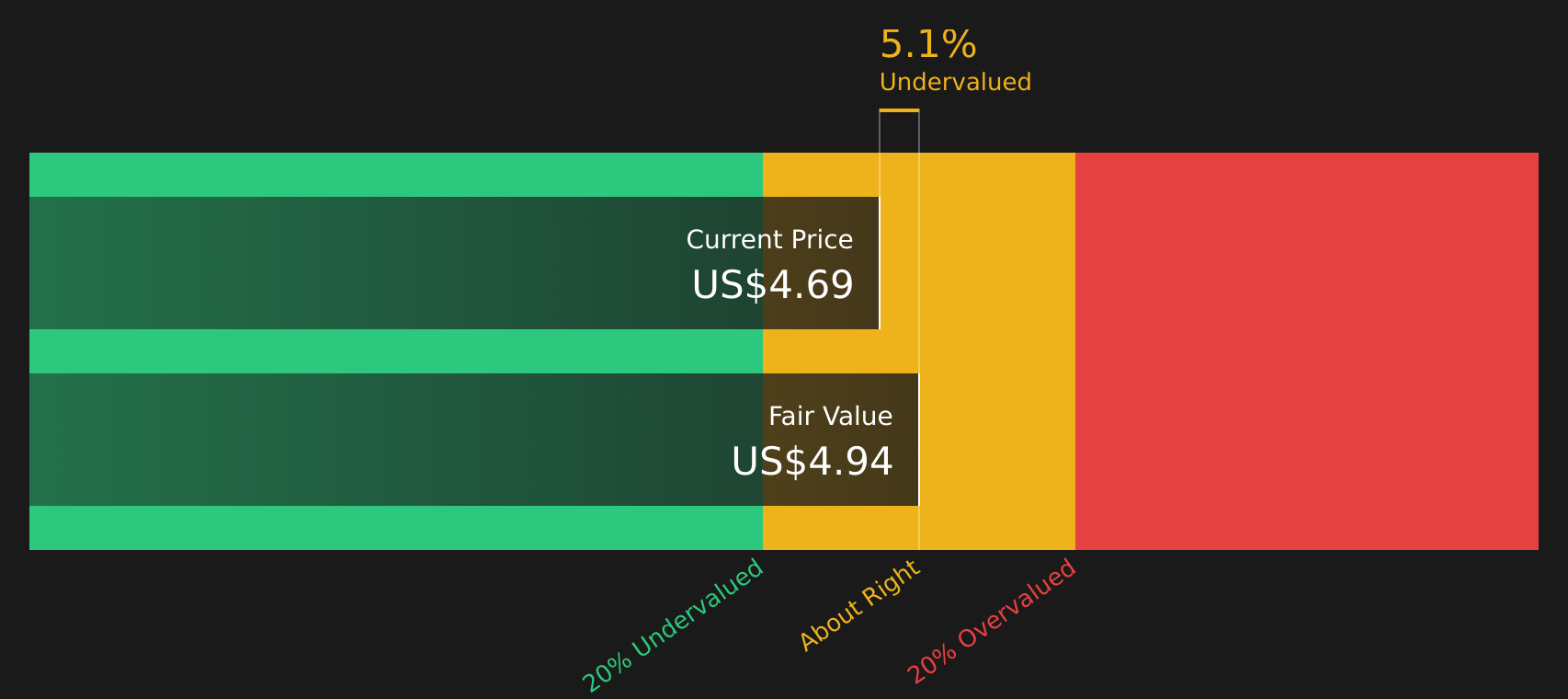

A Discounted Cash Flow model projects a company’s future cash flows and then discounts them back to today, aiming to estimate what the entire business could be worth right now.

For eXp World Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach that starts from last twelve months free cash flow of about $109.1 million. Simply Wall St then applies cash flow projections, with analyst inputs for the early years and its own extrapolations thereafter, to estimate how those cash flows might look over time.

By 2035, the model is working with projected free cash flow of about $79.6 million, all expressed in $. When those yearly amounts are discounted back to today and combined with a terminal value, the result is an estimated intrinsic value of about $7.93 per share.

Against a recent share price around $7.50, the DCF implies the stock is roughly 5.4% undervalued, which is a fairly small gap and could be within the usual margin of error for this kind of model.

Result: ABOUT RIGHT

eXp World Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: eXp World Holdings Price vs Sales

For companies where earnings can be noisy, the P/S ratio is often a useful way to look at value, because it compares the market value of the business to the revenue it is bringing in, rather than to accounting profit. Investors usually accept a higher or lower P/S depending on what they expect for future growth and how risky they think those revenues are, so there is no single “right” number that fits every stock.

eXp World Holdings is currently trading at a P/S of 0.25x. That sits below the Real Estate industry average P/S of 2.66x and below the peer average of 0.81x. Simply Wall St’s Fair Ratio for the company is 0.37x, which is its proprietary estimate of what a more “normal” P/S might be given factors like the company’s growth profile, profit margins, size and risk characteristics.

This Fair Ratio can be more tailored than a simple peer or industry comparison, because it looks at the company’s own fundamentals rather than assuming it should trade exactly in line with others. With the current P/S of 0.25x versus a Fair Ratio of 0.37x, the shares screen as undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your eXp World Holdings Narrative

Earlier we mentioned that there is an even better way to think about value, and on Simply Wall St this is done through Narratives. You write a simple story about eXp World Holdings, link that story to your own assumptions for future revenue, earnings and margins, and the platform then turns it into a forecast and a fair value. You can compare this directly with the current price on the Community page that is used by millions of investors. When new information such as legal developments around workplace oversight or news like the reaffirmed US$13.00 fair value and updated discount rate, revenue growth and profit margin assumptions comes in, your Narrative updates automatically. This means one investor might build a cautious eXp World Holdings Narrative that focuses on legal and regulatory risks and arrives at a lower fair value, while another focuses more on global expansion, technology adoption and ancillary revenue opportunities and arrives at a higher fair value. You can use those different fair values, side by side, to help decide whether the current price looks attractive to you or not.

Do you think there's more to the story for eXp World Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.