Is It Time To Revisit Inspire Medical Systems (INSP) After A Sharp Share Price Pullback?

Inspire Medical Systems, Inc. INSP | 0.00 |

- If you are wondering whether Inspire Medical Systems at around US$57.59 is priced attractively or not, it helps to start by separating story from numbers.

- The share price has moved 6.6% over the last 7 days and 2.1% over the past month, set against a much weaker year to date return of 37.6% and a 1 year return of 61.7%.

- Recent coverage has focused on the company as a medical device player in sleep apnea treatment, with attention on how its growth profile and competitive position compare with other specialized healthcare names. That context matters when you weigh up a share price that has pulled back over 3 and 5 years, with returns of 79.1% and 74.7% respectively.

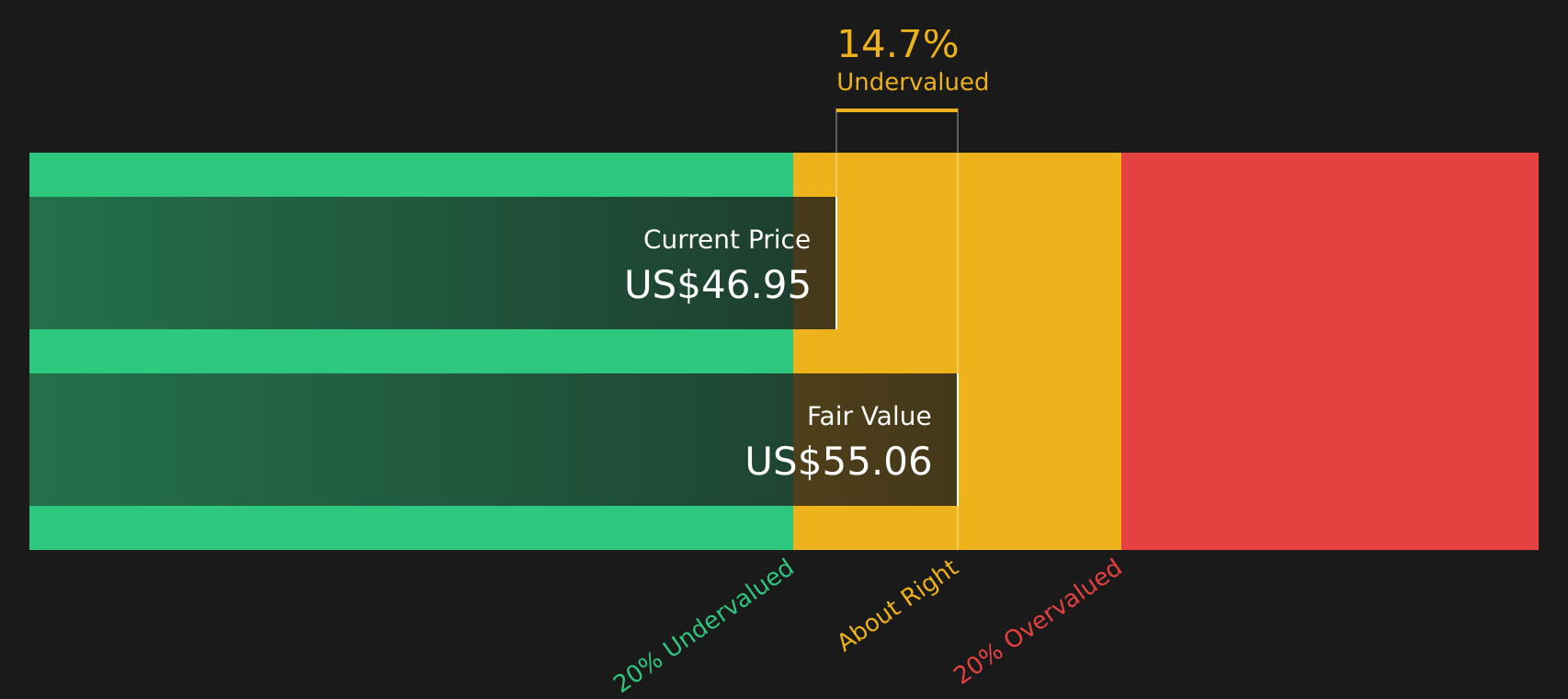

- Simply Wall St currently gives Inspire Medical Systems a valuation score of 5 out of 6 based on six separate checks for potential undervaluation. The next sections will compare what different valuation methods say about the stock, while keeping an even more helpful way to think about value for the end of the article.

Approach 1: Inspire Medical Systems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows and then discounts them back to today using a required rate of return to estimate what the business might be worth right now.

For Inspire Medical Systems, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow sits at about $77.5 million. Analyst estimates and extrapolations together produce ten year free cash flow projections, with discounted values such as $147.5 million in 2026, $162.2 million in 2027 and $157.7 million in 2028, extending through to 2035 using Simply Wall St extrapolations.

When all of those discounted cash flows are added up, the model arrives at an estimated intrinsic value of about $146.92 per share. Compared with the recent share price of around $57.59, this implies an intrinsic discount of 60.8%. On this DCF view, the shares screen as undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Inspire Medical Systems is undervalued by 60.8%. Track this in your watchlist or portfolio, or discover 59 more high quality undervalued stocks.

Approach 2: Inspire Medical Systems Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay for a share directly to the earnings that support it. In general, higher growth expectations and lower perceived risk can justify a higher P/E, while slower growth or higher risk tend to align with a lower, more conservative multiple.

Inspire Medical Systems currently trades on a P/E of about 11.4x. That sits well below the Medical Equipment industry average of roughly 26.0x and the peer group average of about 77.7x. Simply Wall St also calculates a “Fair Ratio” for the stock of around 15.7x, which is the P/E level suggested by its earnings growth profile, industry, profit margins, market cap and identified risks.

This Fair Ratio is more tailored than a simple comparison with peers or the broad industry, because it adjusts for the company’s own characteristics rather than assuming that all medical equipment names should trade on the same multiple. Setting the current P/E of 11.4x against the Fair Ratio of 15.7x indicates that the shares are trading below the level implied by those fundamentals.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Inspire Medical Systems Narrative

Earlier sections compared Inspire Medical Systems using DCF and P/E, but a more useful way to think about value is through Narratives, where you set a clear story for the company and tie that story to explicit assumptions for future revenue, earnings, margins and a fair value estimate, then compare that to the current price.

On Simply Wall St's Community page, Narratives let you do this in a structured and accessible way, connecting your view of Inspire Medical Systems, such as cautious expectations around reimbursement and slower growth or a more optimistic view linked to faster Inspire V adoption and stronger margins, directly to a forecast and resulting fair value.

For Inspire Medical Systems today, one investor might lean toward a cautious Narrative with a fair value around US$56 based on slower revenue growth, lower margins and a P/E near 30x in 2029. Another might back a more optimistic Narrative with a fair value near US$212 that assumes higher revenue growth, improving margins and a P/E near 47x in 2028. As new information like earnings, CMS updates or guidance changes arrives, these Narratives can be updated so you can keep checking how each fair value compares with the live share price.

For Inspire Medical Systems, we will make it really easy for you with previews of two leading Inspire Medical Systems Narratives:

Start with this bullish take if you think the current pricing is too cautious.

Fair value: US$79.42

Implied discount to this fair value versus the last close of US$57.59: about 27.5%.

Revenue growth assumption: 8.01% a year.

- Analysts in this camp see recent operational and coding issues as temporary, with CMS clarity and Inspire V adoption helping support future procedure volumes and earnings power.

- The narrative builds in mid single digit to high single digit annual revenue growth, a step down in profit margins from current levels, and a future P/E of about 26.5x on 2029 earnings.

- It leans on broad sleep apnea demand, reimbursement support and improved center productivity, while flagging risks around rollout execution, reimbursement policy shifts and possible changes in treatment preferences.

Or start here if you think the market is already giving Inspire Medical Systems the benefit of the doubt.

Fair value: US$56.00

Implied premium to this fair value versus the last close of US$57.59: about 2.8%.

Revenue growth assumption: 5.64% a year.

- This view leans on reimbursement pressure, slower center expansion and higher operating costs as constraints on revenue growth and margins despite ongoing demand for sleep apnea treatment.

- The bearish cohort assumes mid single digit annual revenue growth, margin compression toward the mid single digits and a future P/E of about 30.6x on 2029 earnings, which is higher than the current industry P/E used in the narrative.

- Key watchpoints include the Inspire V rollout, competition from at home or non implant options, legal and compliance costs and the risk that value based care models weigh on pricing and long term earnings potential.

Use these two Narratives as reference points, then adjust the growth, margins, P/E and risk assumptions until the story lines up with how you see Inspire Medical Systems and what you think the shares are worth at today’s price.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Inspire Medical Systems on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Inspire Medical Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.