Is It Time To Revisit United Parcel Service (UPS) After DCF Signals A Large Valuation Gap?

United Parcel Service, Inc. Class B UPS | 0.00 |

Beyond the day to day moves, many investors are really asking one thing about United Parcel Service: is the current share price giving you fair value for what you are getting?

Before looking under the hood, it helps to know what is actually being measured when talking about valuation.

What valuation really means for United Parcel Service

Valuation is simply an attempt to connect the price you see on the screen with the cash flows, assets and risks that sit behind United Parcel Service.

Instead of treating the share price as a verdict, valuation asks whether the current price fairly reflects the company as it stands today.

To do that, investors often break the question into a few core angles, such as what the business might earn in the future, what it owns and owes today, and how the current market price compares with those reference points.

Each approach has its own strengths and blind spots, which is why many investors like to look at several methods side by side rather than relying on a single number.

Key valuation approaches this article will cover

- Discounted cash flow (DCF), which estimates what future cash flows might be worth in today's money.

- Market multiples such as P/E or P/B, which compare United Parcel Service with similar companies on standard ratios.

- Asset and balance sheet checks, which look at what the company owns and owes relative to its market value.

- Qualitative context, such as industry position and business model durability, that helps explain why the market might be putting a particular price on the stock.

Taken together, these approaches can give you a fuller picture of whether the current share price looks demanding, reasonable or modest compared with the fundamentals.

How the Simply Wall St value score fits in

Alongside these individual methods, Simply Wall St also aggregates several valuation checks into a single score for United Parcel Service.

This value score runs from 0 to 6 and adds 1 point for each check where the stock screens as undervalued based on factors such as DCF estimates, P/E, P/B and other metrics.

United Parcel Service currently scores 4 out of 6, which means it passes four of these undervaluation checks.

The rest of this article will unpack what sits behind that score by walking through the main valuation approaches in turn, and then finish with a way of looking at value that goes beyond any single model or metric.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of future cash flows, then discounts them back to what they might be worth in today’s dollars. It is essentially asking what a stream of future cash flows could be worth if you had to pay for it now.

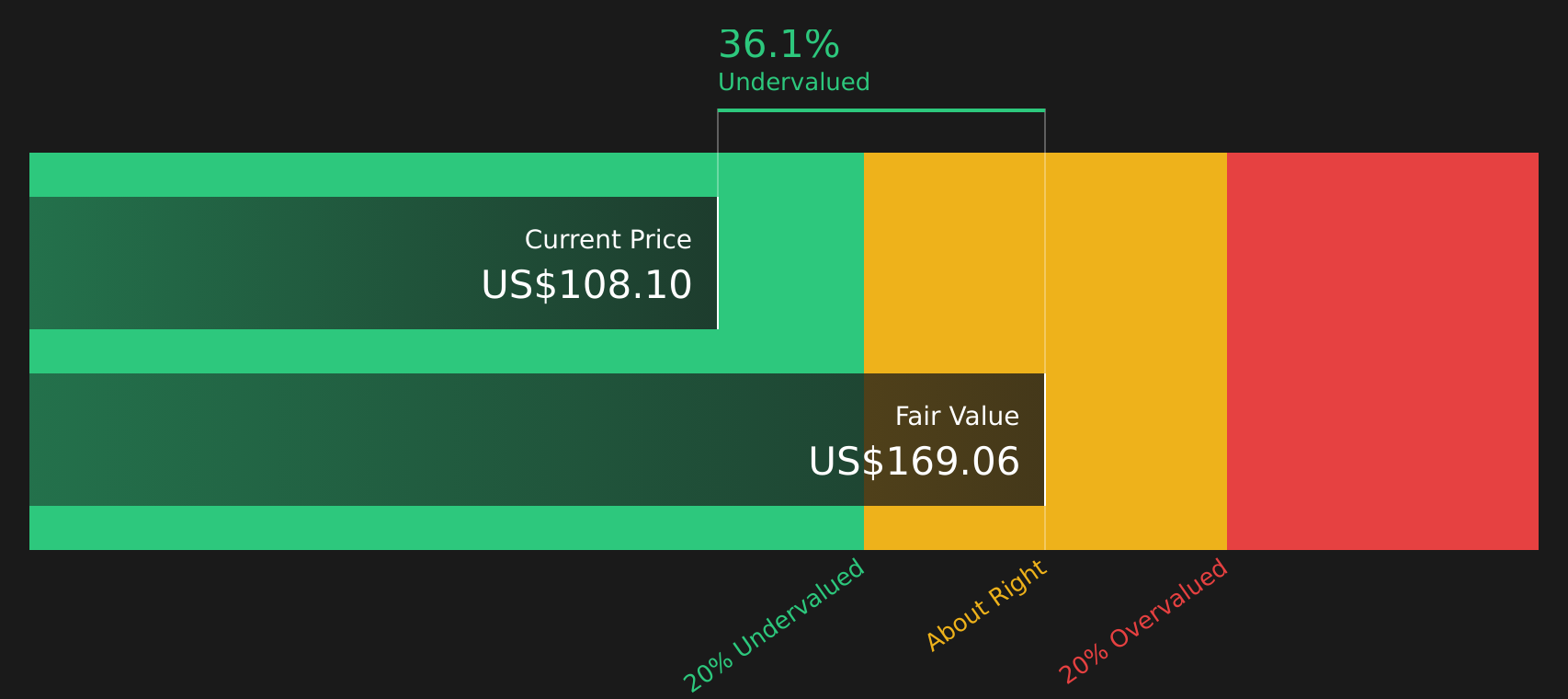

For United Parcel Service, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $4.0b. Simply Wall St then projects Free Cash Flow in detail out to 2035, using analyst estimates where available and extending those projections further out. For example, projected Free Cash Flow for 2029 is $7.46b, with discounted values provided for each year between 2026 and 2035.

When those projected cash flows are discounted back and aggregated, the model arrives at an estimated intrinsic value of $165.77 per share. Compared with the current share price, this implies an intrinsic discount of 40.6%. This outcome suggests the stock screens as undervalued on this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 40.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. It links directly to how quickly earnings might grow and how risky those earnings are, which is why it is often a go to yardstick for established businesses.

In broad terms, higher growth and lower perceived risk tend to justify a higher “normal” or “fair” P/E ratio, while slower growth or more uncertainty usually point to a lower multiple. So the question is not whether a P/E is high or low in isolation, but whether it fits the company’s earnings profile and risks.

United Parcel Service currently trades on a P/E of 15.94x, compared with the Logistics industry average of about 15.76x and a peer average of 22.34x. Simply Wall St’s proprietary “Fair Ratio” for United Parcel Service is 22.37x. This Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it incorporates factors such as the company’s earnings growth profile, profit margins, industry, market cap and risk characteristics. On this framework, United Parcel Service’s actual P/E of 15.94x is below the Fair Ratio of 22.37x, which indicates that the stock screens as undervalued on this earnings based check.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives take that next step by allowing you to link a clear story about United Parcel Service to specific assumptions for future revenue, earnings and margins. You can then convert those assumptions into a Fair Value and compare that Fair Value with the current price, all within Simply Wall St's Community page. Narratives are updated as new information arrives and you can see, for example, one community view that sets fair value around US$95.21 and another closer to US$135.00, and decide which story about United Parcel Service you find more reasonable for your own decision making.

For United Parcel Service, here are previews of two leading United Parcel Service Narratives to make comparison easier:

Fair value used in this bullish narrative: US$135.00

Gap between this fair value and the last close of US$98.42: about 27.1% below the narrative fair value

Revenue growth assumption in this bullish view: 4.38% a year

- Focuses on automation, cost reductions and network reconfiguration, with analysts building in revenue of US$100.8b and earnings of US$7.3b by 2029 and a P/E of 20.2x on those earnings.

- Highlights opportunities in healthcare logistics and global trade routes, with updated research lifting the narrative fair value to US$135 and using an 8.34% discount rate.

- Flags risks around competition, labor costs, regulation and sustainability requirements and stresses the need to test these bullish assumptions against personal expectations.

Fair value used in this cautious narrative: US$95.21

Gap between this fair value and the last close of US$98.42: about 3.4% above the narrative fair value

Revenue growth assumption in this cautious view: 1.75% a year

- Sets out concerns about higher costs, sustainability issues and internal headwinds, with an initial fair value of US$95.21 and a P/E of 14.5x on expected 2028 earnings.

- Points to facility closures, job cuts and new debt, alongside union tensions and shareholder governance proposals, as factors that could weigh on future profitability.

- Notes that new partnerships and efficiency plans could help, but sees execution risk and earnings pressure as key reasons to treat the stock prudently at this fair value level.

If you want to see how these UPS stories are built from the ground up, including the detailed earnings, margin and P/E paths behind each fair value, you can go straight to the narrative pages and compare the full bullish and cautious cases side by side using the community tools.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for United Parcel Service on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.