Is It Too Late To Consider Akamai Technologies (AKAM) After Its Recent Share Price Jump?

Akamai Technologies, Inc. AKAM | 118.00 | +1.94% |

- If you are wondering whether Akamai Technologies is priced fairly or if there is still value on the table, this article walks through what the current share price may be implying.

- The stock last closed at US$111.76, with reported returns of 17.5% over 7 days, 23.3% over 30 days, 31.3% year to date, 11.7% over 1 year, 44.6% over 3 years, and 13.0% over 5 years, which gives plenty for valuation focused investors to think about.

- Alongside these share price moves, recent coverage around Akamai has centered on its position in software and content delivery and how investors are weighing that against broader sector trends. This provides useful context when you are asking whether the current price and expectations are in sync.

- Simply Wall St currently gives Akamai a value score of 2 out of 6, reflecting that it screens as undervalued on 2 of 6 checks. Next we will walk through the main valuation approaches used here before coming back at the end to a more complete way to think about what that score really means.

Akamai Technologies scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

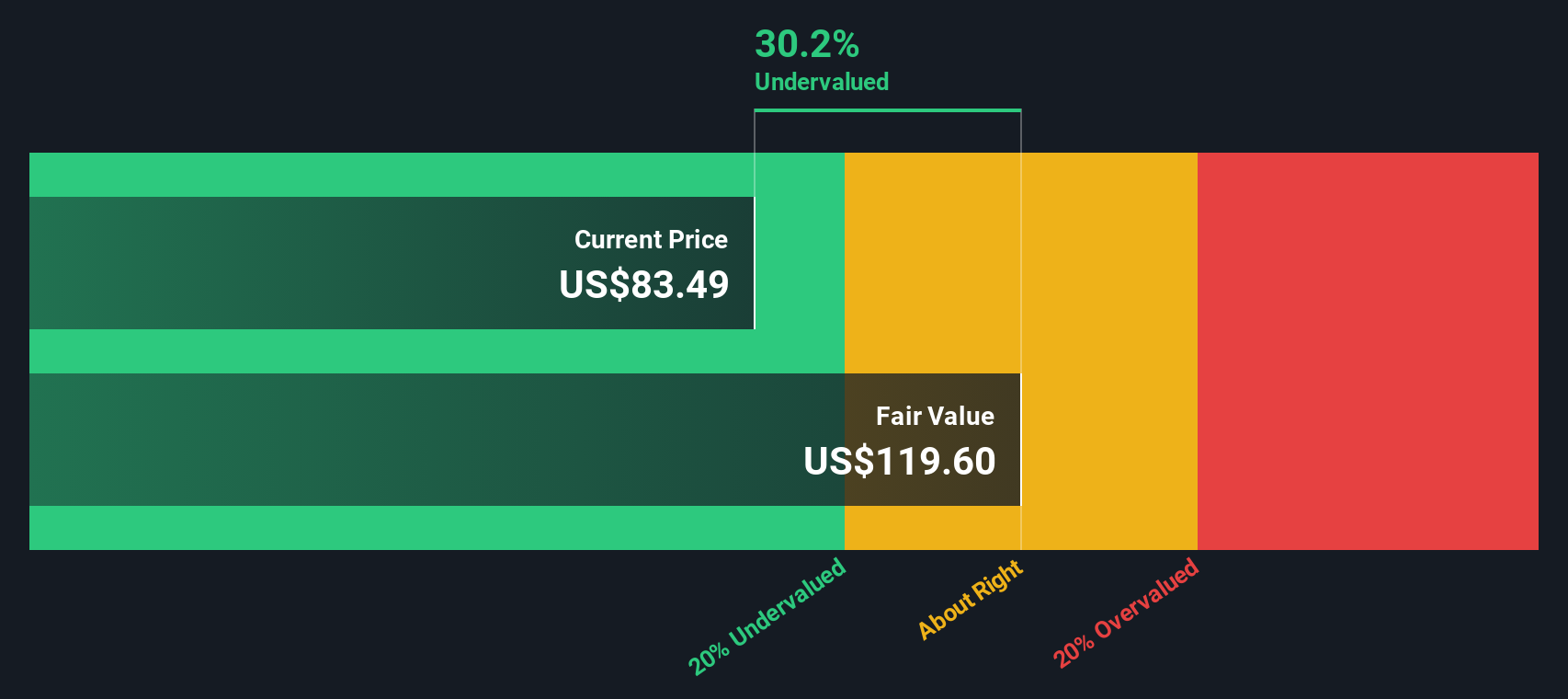

Approach 1: Akamai Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected cash flows a company may generate in the future and discounts them back to today to estimate what the business could be worth right now.

For Akamai Technologies, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is reported at about $649.8 million. Analysts provide specific free cash flow estimates up to several years out, and Simply Wall St then extrapolates those further, with projections ranging from $899.3 million in 2026 to $472.3 million in 2035. Within that, the projection for 2030 is $620 million.

After discounting these projected cash flows, the model arrives at an estimated intrinsic value of about $47.07 per share. Against the recent share price of US$111.76, this implies the stock is 137.4% overvalued based on this DCF framework.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Akamai Technologies may be overvalued by 137.4%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

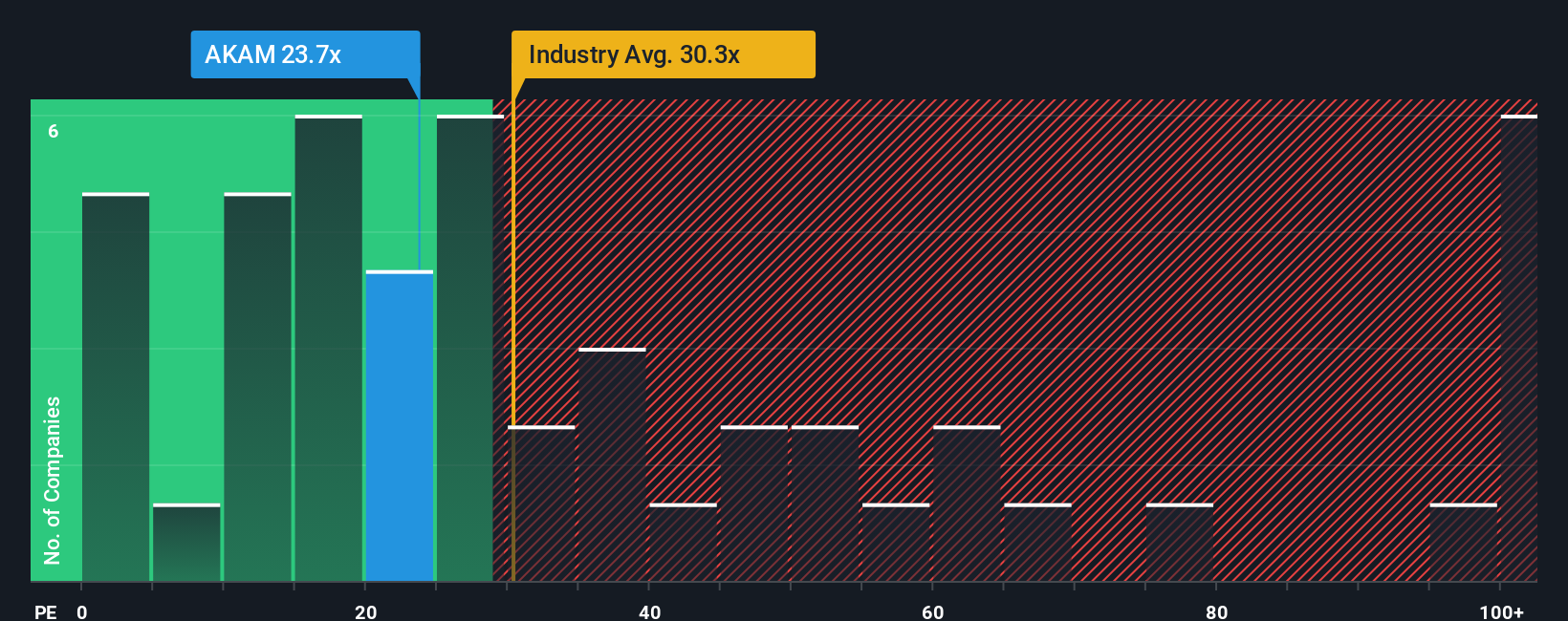

Approach 2: Akamai Technologies Price vs Earnings

For a profitable company like Akamai Technologies, the P/E ratio is a straightforward way to think about what you are paying for each dollar of earnings. Investors usually accept a higher P/E when they expect stronger growth or see lower risk, and a lower P/E when they expect slower growth or see higher risk.

Akamai’s current P/E is 31.7x, compared with the IT industry average of about 23.2x and a peer group average of 43.2x. Simply Wall St’s Fair Ratio for Akamai is 31.8x, which is their estimate of what a “normal” P/E might look like after factoring in elements such as earnings growth profile, profit margins, industry, market cap and specific risks.

This Fair Ratio is designed to be more tailored than a simple comparison with peers or the broad industry, because it adjusts for company specific traits rather than assuming all IT stocks should trade on the same multiple. With Akamai’s actual P/E of 31.7x sitting very close to the Fair Ratio of 31.8x, the shares appear to be trading at roughly the level this framework would suggest.

Result: ABOUT RIGHT

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Akamai Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simply your story about Akamai Technologies, tied to your own assumptions for future revenue, earnings and margins, that link into a forecast and then into a Fair Value you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are set up so you can see this link clearly. Your view of the business flows into a financial model and resulting Fair Value, which is then shown side by side with the current share price to help you decide whether the stock looks expensive, cheap, or somewhere in between for your assumptions.

Narratives update automatically when new information comes through, such as earnings, guidance or news. That keeps your Fair Value and your thinking about potential trades anchored to the latest data rather than a static snapshot.

For Akamai Technologies, one investor might build a more cautious Narrative that lines up with a Fair Value around the lower analyst end near US$66. Another might build a more optimistic Narrative closer to the upper end around US$131. Both can quickly see how their story translates into numbers and how far each Fair Value is from the current share price.

For Akamai Technologies, however, we will make it really easy for you with previews of two leading Akamai Technologies Narratives:

Fair value in this bullish Narrative: US$131.64 per share

Gap to that fair value at the last close of US$111.76, about 15.1% below the Narrative fair value

Assumed revenue growth: 8.24% a year

- This view assumes Akamai grows faster than consensus as AI, edge, and security offerings pick up more enterprise workloads and improve recurring margins.

- It also sees industry consolidation in content delivery, rising video and IoT traffic, and data sovereignty rules as supports for steadier delivery revenues and pricing power.

- It accepts meaningful risks around competition from hyperscalers, commoditization of legacy CDN, and execution on newer security and edge initiatives, but views them as manageable.

Fair value in this more cautious Narrative: US$101.16 per share

Gap to that fair value at the last close of US$111.76, about 10.5% above the Narrative fair value

Assumed revenue growth: 6.99% a year

- This more cautious view builds on analyst assumptions that Akamai can grow earnings through security and compute, but at a more moderate pace than the bullish view, with a lower future P/E multiple.

- It flags the drag from higher capex and operating spend for cloud and edge build out, plus dependence on a smaller group of large contracts that could make earnings less predictable.

- It highlights ongoing pressure on the legacy CDN business, competition from large cloud providers, and the chance that newer offerings do not scale fast enough to fully offset those headwinds.

Do you think there's more to the story for Akamai Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.