Is It Too Late To Consider American Express (AXP) After Its Strong Multi Year Rally?

American Express Company AXP | 300.18 | -0.11% |

- If you have ever wondered whether American Express shares are still priced reasonably after their long run, this article will walk you through what the current market price might be implying.

- The stock recently closed at US$352.17, with returns of 12.1% over 1 year and very large gains over 5 years. It has also shown a 2.6% decline over 7 days and a 5.5% decline over 30 days, and year to date it is down 5.5%.

- Recent news flow around American Express has largely centered on its role as a global payments and card network. This includes ongoing attention on consumer spending patterns and credit quality, as investors watch how card issuers are positioned. Broader sector discussions about interest rates, lending standards and consumer health have also kept companies like American Express in focus. This helps frame how the market is currently thinking about risk and reward for the stock.

- On our valuation checklist, American Express currently scores 1 out of 6 for being undervalued on traditional metrics. Next, we will walk through what different valuation methods say about that price, and then finish with a framework that can help you judge whether those numbers really fit your own view of the business.

American Express scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

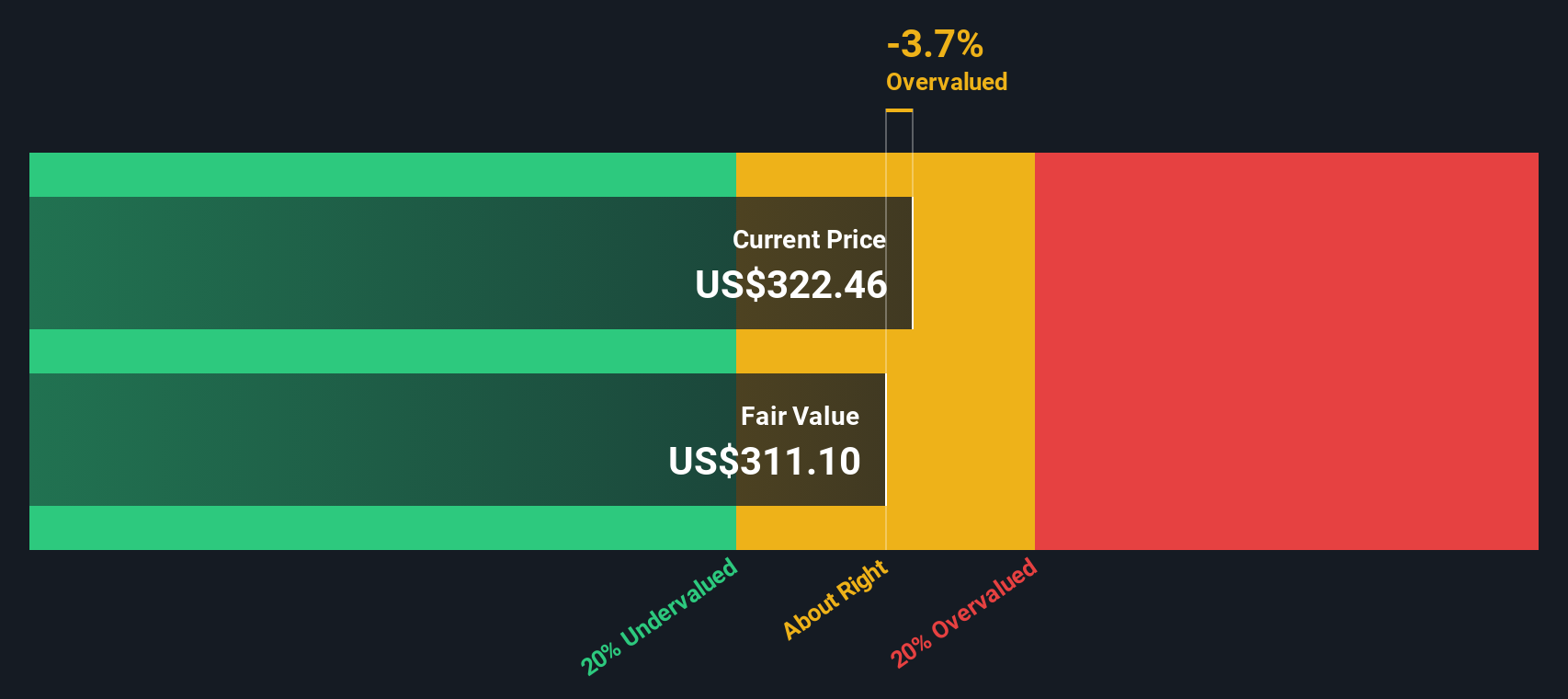

Approach 1: American Express Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to earn above the return that shareholders require, then adds that stream of extra value to its book value per share.

For American Express, the model starts with a Book Value of $47.05 per share and a Stable EPS of $20.43 per share, based on weighted future Return on Equity estimates from 9 analysts. The Average Return on Equity is 37.18%, while the Cost of Equity is $4.58 per share, which implies an Excess Return of $15.85 per share. In other words, the company is modeled to earn more on its equity base than the return investors are assumed to require.

The Stable Book Value used in the model is $54.94 per share, sourced from weighted future Book Value estimates from 6 analysts. Combining this book value with the projected excess returns produces an intrinsic value estimate of about $367.61 per share.

Compared with the recent share price of about $352.17, the Excess Returns model points to roughly a 4.2% discount, which is quite small.

Result: ABOUT RIGHT

American Express is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

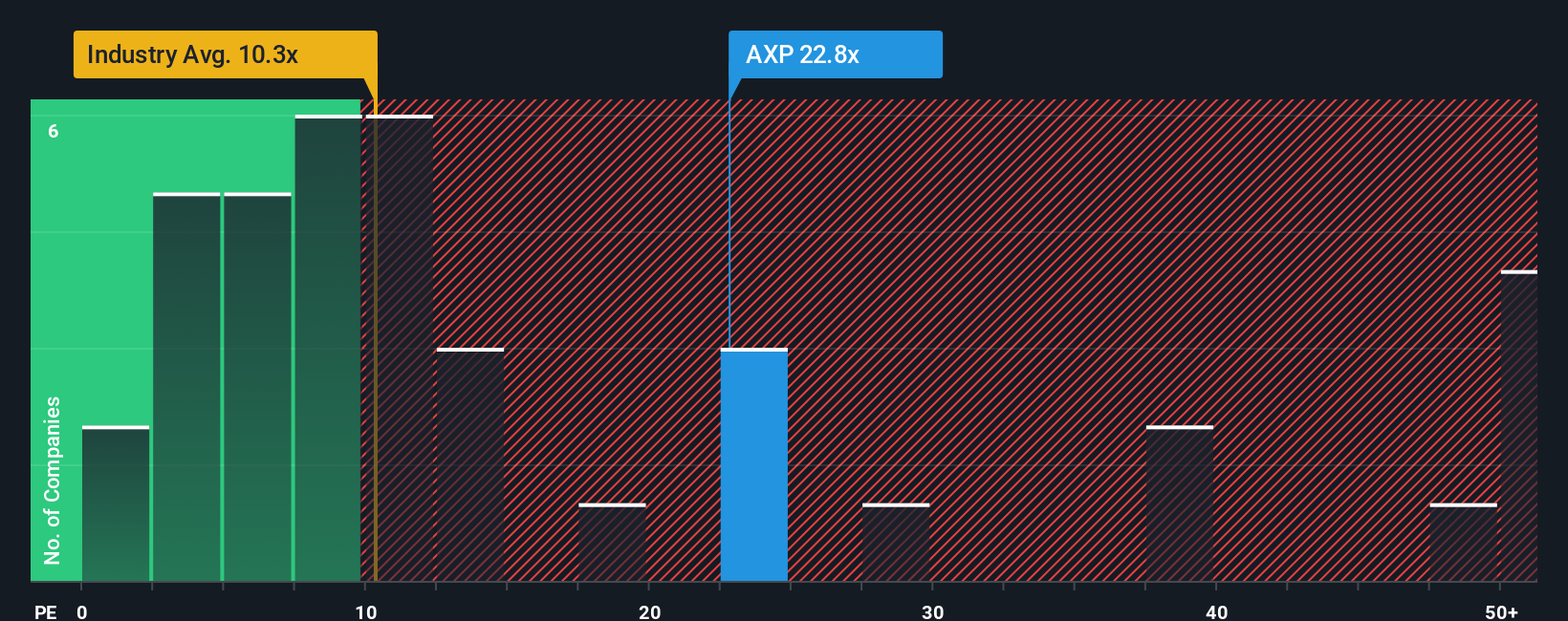

Approach 2: American Express Price vs Earnings

For a profitable company like American Express, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings. It links directly to what the business is currently earning, which is often easier to relate to than cash flow or book value models.

What counts as a "fair" P/E usually reflects the trade off between expected growth and risk. Higher growth or lower perceived risk can support a higher multiple, while slower growth or higher risk tends to justify a lower one.

American Express currently trades on a P/E of 23.30x. That is above the Consumer Finance industry average P/E of 8.69x and slightly above the peer group average of 22.58x. Simply Wall St also calculates a proprietary Fair Ratio of 20.32x, which is the P/E level it would expect given factors such as earnings growth, profit margins, industry, market cap and specific risks.

This Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for company specific characteristics rather than assuming all Consumer Finance stocks should trade at the same multiple.

With the current P/E of 23.30x sitting above the Fair Ratio of 20.32x, this approach points to American Express appearing overvalued on earnings.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1417 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your American Express Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which simply means writing down your story about American Express and linking it directly to your own assumptions for future revenue, earnings, margins and fair value.

Instead of only looking at the P/E or a single fair value estimate, a Narrative ties three things together: what you believe about the business, the financial forecast that follows from that belief, and the fair value that results from those numbers.

On Simply Wall St, Narratives sit in the Community page and are used by millions of investors as an easy tool where you can plug in your expectations, see the implied fair value and compare it with the current share price to help decide whether the stock looks attractive, fully priced or expensive for you personally.

Because Narratives on the platform update when new information arrives, such as fresh earnings or important news, your fair value view can evolve in real time and you will see different investors publishing Narratives for American Express with very high and very low fair values based on their own assumptions about its future.

Do you think there's more to the story for American Express? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.