Is It Too Late To Consider Amgen (AMGN) After Strong One Year Share Price Gains?

Amgen Inc. AMGN | 0.00 |

- Investors may be wondering whether Amgen, at around US$340 a share, still offers value or whether most of the opportunity is already priced in.

- The stock has pulled back 1.4% over the last week and 2.5% over the last month, although it is still up 3.8% year to date and 21.6% over the past year.

- Recent attention on Amgen reflects ongoing interest in large biotech names as investors reassess long term growth drivers and the role of established players in portfolios. Broader sector conversations about pricing, regulation, and capital allocation decisions continue to shape how investors think about risk and reward for companies like this.

- Amgen currently scores 4 out of 6 on Simply Wall St's valuation checks. This sets up a closer look at how different methods such as DCF, multiples, and peer comparisons stack up, and hints at a more complete way to think about value that will be covered at the end of this article.

Approach 1: Amgen Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today using a required return, giving an estimate of what the entire business could be worth now.

For Amgen, the model starts with last twelve months free cash flow of about $8.4b and uses analyst forecasts for the next several years, then extends those projections further out. By 2030, free cash flow is projected at about $16.5b, with intermediate yearly figures between 2026 and 2035 ranging from around $13.4b to $20.5b before discounting.

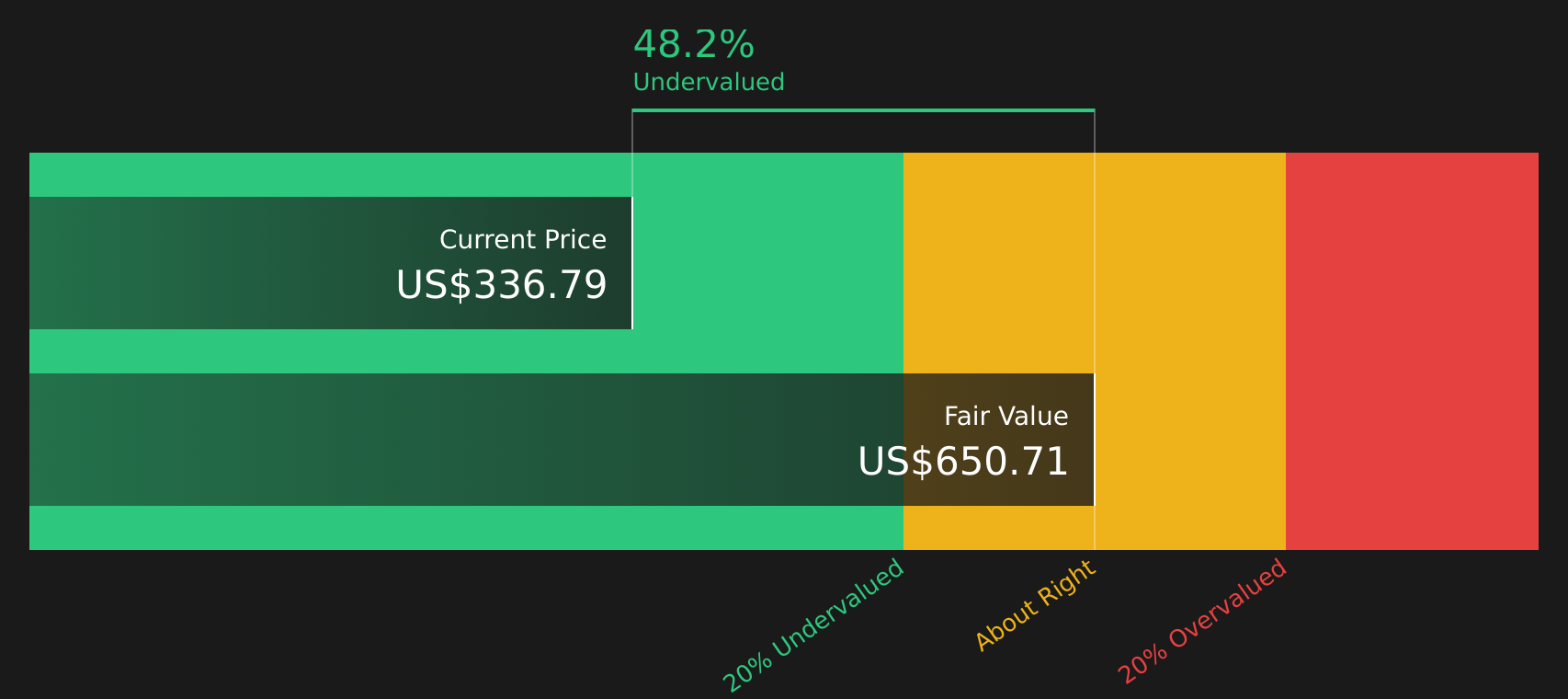

Using a 2 Stage Free Cash Flow to Equity approach, these cash flows are discounted and summed to an estimated intrinsic value of about $644.13 per share. Compared with a recent share price around $340, this DCF indicates roughly a 47.2% discount to the modelled value. This suggests that, under the assumptions used, Amgen is trading well below this cash flow based estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Amgen is undervalued by 47.2%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Amgen Price vs Earnings

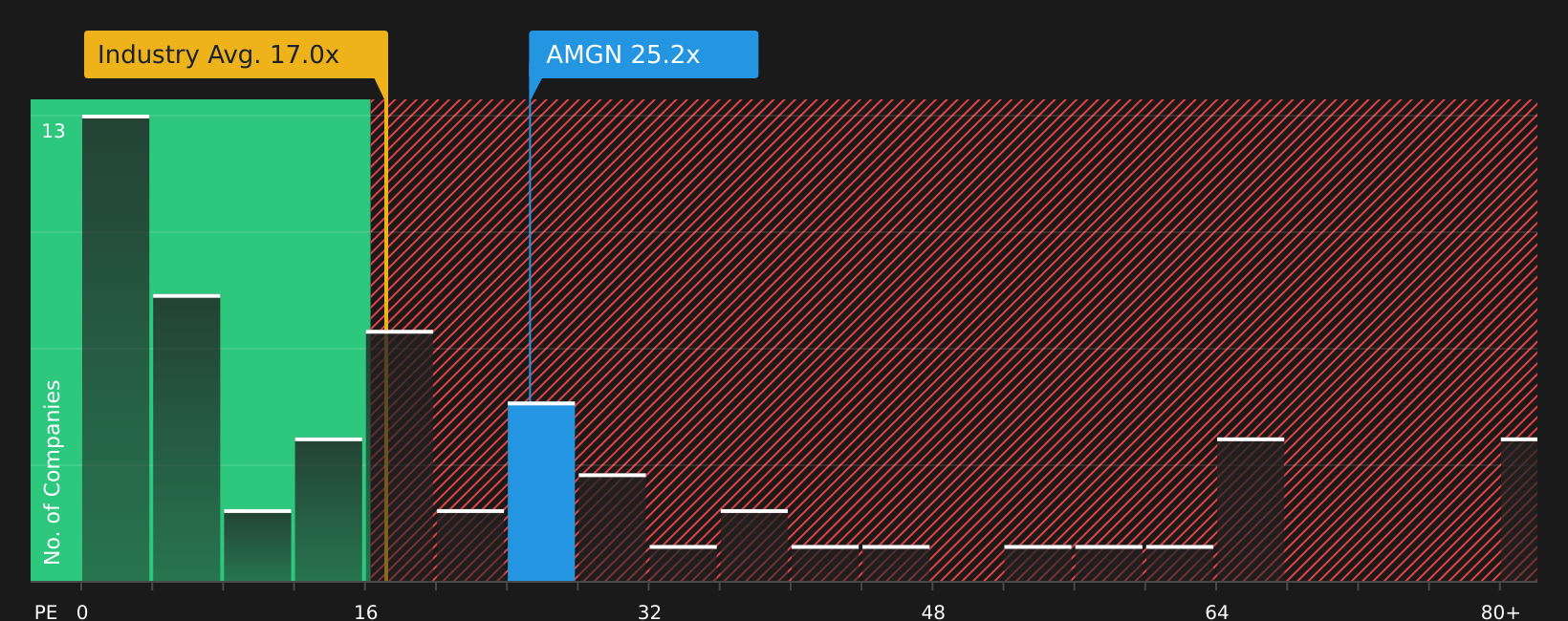

For a profitable company like Amgen, the P/E ratio is a useful shorthand because it links what you pay today to the earnings the business is already generating. It is a way to see how much the market is willing to pay for each dollar of current earnings.

What counts as a “normal” P/E usually reflects two things: how fast earnings are expected to grow and how risky those earnings might be. Higher expected growth or lower risk can support a higher multiple, while slower growth or higher uncertainty can point to a lower one.

Amgen currently trades on a P/E of 23.81x. That is above the Biotechs industry average P/E of about 17.26x, but below the peer group average of 36.56x. Simply Wall St’s proprietary Fair Ratio for Amgen is 26.09x. This Fair Ratio aims to capture what a reasonable P/E could look like after considering factors such as earnings growth, industry, profit margins, market cap and risk, which makes it more tailored than a simple comparison to peers or the broad industry.

Since Amgen’s current P/E of 23.81x is below the Fair Ratio of 26.09x, the shares screen as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Amgen Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced as a simple way for you to attach a clear story about Amgen to the numbers. This links your view on future revenue, earnings and margins to a Fair Value that can be compared directly with the current share price on Simply Wall St’s Community page.

A Narrative on the platform connects three elements: your view of the business, a financial forecast that reflects that view, and a resulting Fair Value. It then updates automatically when new information such as earnings, price targets or trial results is added to the underlying data.

For Amgen, one investor might align with a cautious Narrative that uses assumptions similar to the bearish cohort with a Fair Value around US$243.49. Another investor might align with a more optimistic Narrative closer to the bullish cohort with a Fair Value around US$432.00. By comparing each Fair Value with the current price, you can decide whether the stock looks expensive, cheap, or roughly in line with your expectations based on the story you believe.

For Amgen however we will make it really easy for you with previews of two leading Amgen Narratives:

Fair Value: US$432.00 per share

Gap to Fair Value: about 21.3% below this bullish fair value based on the recent price of US$340.18

Revenue Outlook Used: 6.52% annual revenue growth assumption

- Emphasises a broad autoimmune, cardiovascular and rare disease portfolio, with AI assisted R&D and a wide late stage pipeline supporting the view that new product launches and higher margins can justify a higher value.

- Assumes Amgen can manage pricing and regulatory pressures through its biologics and biosimilars scale, global footprint and capacity for further M&A, with earnings projected to reach US$13.2b by 2029 on a 22.2x P/E.

- Highlights key risks such as drug price reform, patent expiries, biosimilar competition and acquisition integration, and encourages you to test whether the bullish revenue, margin and valuation assumptions align with your own expectations.

Fair Value: US$243.49 per share

Gap to Fair Value: about 39.7% above this bearish fair value based on the recent price of US$340.18

Revenue Outlook Used: 0.07% annual revenue decline assumption

- Focuses on reliance on aging blockbusters, patent expirations and growing biosimilar and branded competition, with concerns that these could pressure revenue and margins over time.

- Builds in the effect of potential pricing reforms, value based care and cost inflation, alongside integration and execution risk from large acquisitions, using a 21.7x P/E on 2029 earnings of US$7.6b.

- Flags that strong current volume growth, a broad late stage pipeline, biosimilars strength and demographic trends could all challenge this cautious view, so the key question is how much downside you see from today’s price relative to that US$243.49 fair value.

If you want to go beyond these previews and see how other investors are framing Amgen's risk and reward trade off, including different Fair Values and storylines, you can review the full range of Community views in one place with See what the community is saying about Amgen.

Do you think there's more to the story for Amgen? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.