Is It Too Late To Consider Buying Compañía de Minas Buenaventura (BVN) After Its 1 Year Surge?

Compania de Minas Buenaventura SAA Sponsored ADR BVN | 0.00 |

- Investors may be wondering if Compañía de Minas BuenaventuraA at around US$31.98 still offers value after a strong run, or if most of the opportunity has already been priced in.

- The stock has returned 2.8% over the last 7 days, moved by 12.2% over the last month, is up 11.9% year to date, 114.5% over 1 year and has a very large 3 year return that is roughly 4x, with a 5 year return of 214.8%.

- Recent attention on the stock has been driven by ongoing interest in metals and mining companies and how they are positioned within the sector. News coverage has focused on how these types of companies manage costs, projects and balance sheet strength as conditions change.

- Simply Wall St gives Compañía de Minas BuenaventuraA a value score of 3 out of 6. The rest of this article will look at how different valuation approaches line up with that score, before finishing with a broader way to think about what valuation really means for you as an investor.

Approach 1: Compañía de Minas BuenaventuraA Discounted Cash Flow (DCF) Analysis

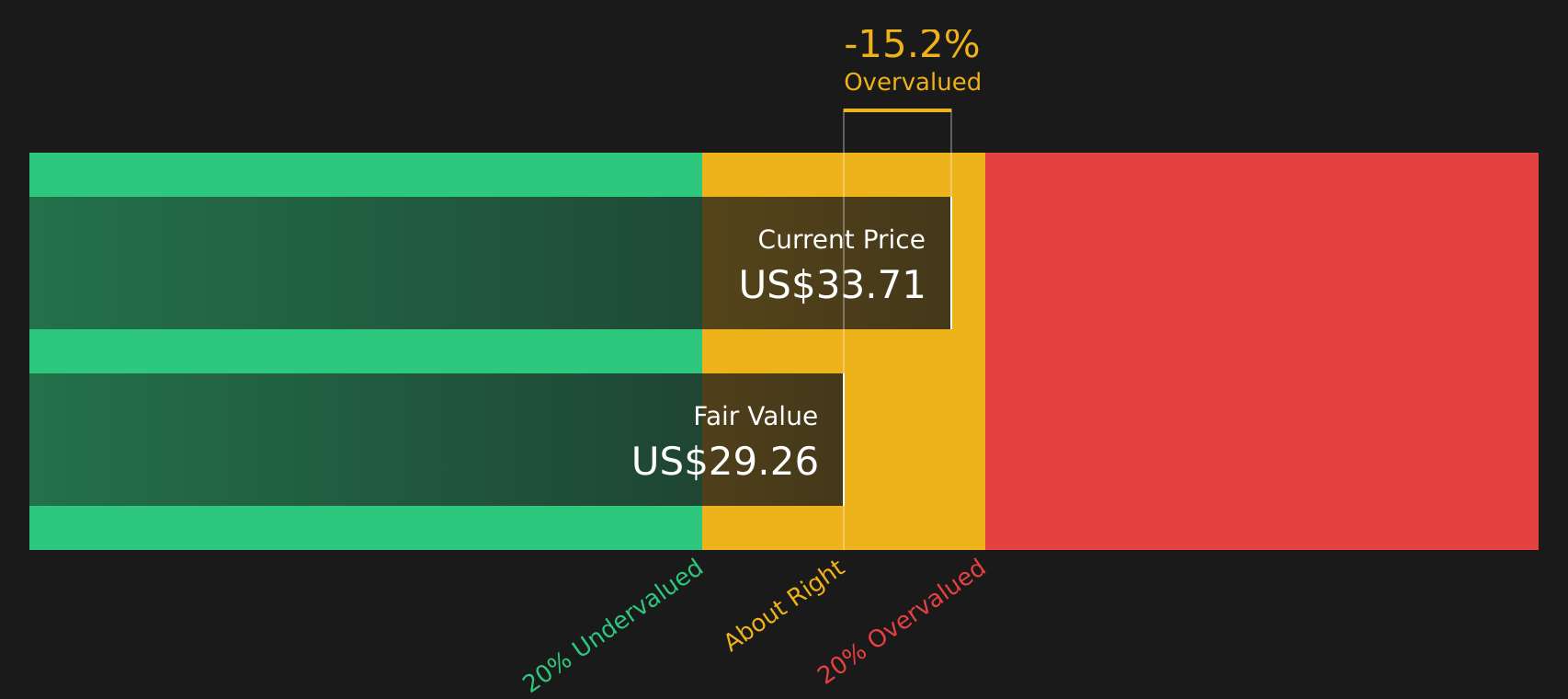

A Discounted Cash Flow, or DCF, model takes the cash that a company is expected to generate in the future and discounts those amounts back to today to estimate what the business might be worth right now.

For Compañía de Minas BuenaventuraA, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $350 million. Simply Wall St then projects future Free Cash Flow, using analyst estimates where available and extending them further out. For example, the projections run through to 2035, with estimated Free Cash Flow of $785.3 million in that year and discounted figures provided for each year in between.

Bringing all of those discounted cash flows together results in an estimated intrinsic value of about $29.26 per share. Compared with the recent share price of around $31.98, the DCF output suggests the stock is about 9.3% overvalued, which sits very close to the model’s fair value range.

Result: ABOUT RIGHT

Compañía de Minas BuenaventuraA is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Compañía de Minas BuenaventuraA Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it links what you are paying directly to the earnings the business is generating today. It gives a quick sense of how many dollars investors are willing to pay for each dollar of profit.

What counts as a “normal” P/E depends on how quickly earnings are expected to grow and how risky those earnings are. Higher expected growth and lower perceived risk usually support a higher P/E, while slower growth or higher uncertainty tend to justify a lower one.

Compañía de Minas BuenaventuraA currently trades on a P/E of 8.23x. That sits below the Metals and Mining industry average of 23.16x and also below the peer group average of 33.65x. Simply Wall St’s proprietary Fair Ratio for the stock is 17.52x, which represents the P/E that might be expected given factors such as its earnings growth profile, profit margins, industry, market value and key risks.

The Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for company specific traits, rather than assuming all miners deserve the same multiple. With the actual P/E of 8.23x sitting well below the Fair Ratio of 17.52x, the multiple based view suggests the stock trades at a discount to what these fundamentals imply.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Compañía de Minas Buenaventura A Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives let you attach a clear story to your numbers by linking your view on Compañía de Minas Buenaventura A’s projects, revenues, earnings and margins to an explicit forecast and a Fair Value that you can then compare with the current price to decide whether the stock looks attractive or stretched.

On Simply Wall St’s Community page, Narratives are set up as easy to use templates that update automatically when fresh information such as news, earnings or guidance is added, so your Fair Value view stays aligned with what is happening at the company.

For example, one Compañía de Minas Buenaventura A Narrative on the bullish end assumes a Fair Value of US$50.00, while a more cautious Narrative assumes US$24.00. That spread shows how different investors can look at the same facts around San Gabriel, copper volumes and margins yet reach very different Fair Values, which you can review side by side and decide which story you find more reasonable.

For Compañía de Minas BuenaventuraA, we will make it really easy for you with previews of two leading Compañía de Minas BuenaventuraA Narratives:

Fair value used in this bullish narrative: US$40.08 per share.

At the recent price of US$31.98, this narrative implies the stock is about 20.2% below that fair value.

Revenue growth assumption in this narrative: 7.76% a year.

- Analysts in this camp see a bigger contribution from San Gabriel and copper volumes, with revenue modeled at US$2.2b and earnings of US$1.0b by around 2029 if their assumptions hold.

- They factor in higher profit margins at about 46.6%, supported by cost controls, contract terms and capital discipline across the project portfolio.

- Their US$40.08 consensus target sits between a bullish US$50.00 and a cautious US$27.40, so the bullish narrative still acknowledges a wide range of possible outcomes.

Fair value used in this bearish narrative: US$24.00 per share.

At the recent price of US$31.98, this narrative implies the stock is about 33.4% above that fair value.

Revenue growth assumption in this narrative: 8.90% a year.

- The bearish cohort focuses on risks around San Gabriel commissioning, tailings management and permitting, which they see as potential constraints on output and cash flow.

- They assume margin pressure, with profit margins modeled to fall from 30.9% to 18.6%, and earnings of US$337.6m by 2029 despite higher revenue.

- On these assumptions, their US$24.00 fair value sits well below the current price, which they view as pricing in stronger execution, higher grades and better cost control than their base case.

Ultimately, you can line these stories up against your own expectations for gold and copper volumes, San Gabriel ramp up, costs and balance sheet strength, then decide which narrative, if either, feels closer to how you see Compañía de Minas BuenaventuraA today.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Compañía de Minas BuenaventuraA on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Compañía de Minas BuenaventuraA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.