Is It Too Late To Consider Buying Garmin (GRMN) After A 95% Five Year Run?

Garmin Ltd. GRMN | 0.00 |

- If you are wondering whether Garmin's current share price reflects its underlying value, the recent track record gives plenty to think about.

- The stock last closed at US$241.90, with returns of 29.1% over 1 year, 19.5% year to date, 0.3% over 30 days, and a 3.7% decline over the past week, adding some short term volatility to a much longer run up of 95.0% over 5 years.

- These moves sit against a backdrop where investors have been closely watching Garmin's positioning across its product categories and how that affects long term expectations. Market attention has also focused on how the company fits into broader themes around consumer electronics and wearables, which can influence both enthusiasm and caution around the stock.

- Despite that backdrop, Garmin currently scores 0 out of 6 on Simply Wall St's valuation checks for being undervalued. The rest of this article will unpack the main valuation methods used on the stock and outline a more complete way to think about value that brings those pieces together at the end.

Garmin scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

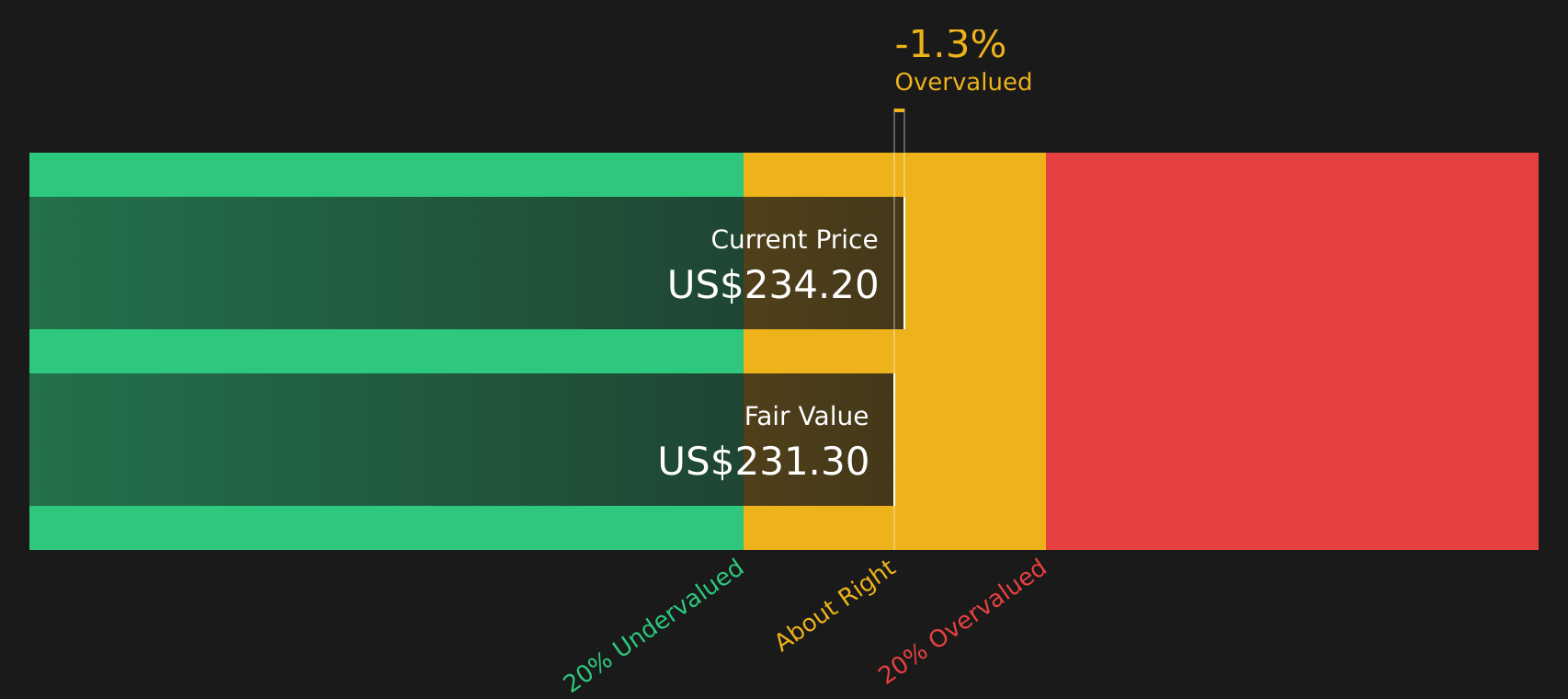

Approach 1: Garmin Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today’s value. It is essentially asking what all those future dollars are worth in today’s terms.

For Garmin, the model uses a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month Free Cash Flow is about $1.49b. Analyst inputs and extrapolated estimates suggest projected Free Cash Flow of $2.29b in 2030, with a detailed path of forecasts and discounted values running from 2026 through 2035.

Pulling those cash flows together, Simply Wall St’s DCF model arrives at an estimated intrinsic value of about $228.49 per share, compared with the recent share price of $241.90. That implies the stock is roughly 5.9% above this DCF estimate, which sits in a range where the model suggests the stock is close to fair value rather than sharply mispriced.

Result: ABOUT RIGHT

Garmin is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Garmin Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to connect what you pay for a stock with the earnings it generates. It lets you see how many dollars investors are currently paying for each dollar of earnings.

What counts as a “normal” P/E depends a lot on how the market views growth potential and risk. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth expectations or higher risk usually points to a lower multiple.

Garmin currently trades on a P/E of 26.9x. That sits above the Consumer Durables industry average P/E of about 12.4x and above the peer average of 16.2x. Simply Wall St’s Fair Ratio for Garmin is 24.1x, which is the P/E level suggested after accounting for factors such as earnings growth, industry, profit margin, market cap and risk profile.

This Fair Ratio is more tailored than a simple peer or industry comparison because it adjusts for Garmin’s specific characteristics rather than assuming all companies in the group should trade on similar multiples. With the current P/E only modestly above the Fair Ratio, the stock screens as slightly expensive on this measure, but broadly in line with expectations.

Result: ABOUT RIGHT

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Garmin Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring your story about Garmin together with the numbers by linking a clear view on its products, competition, regulation and end markets to a forecast for revenue, earnings and margins. This then feeds into a Fair Value that you can easily compare with the current share price to think about when to buy or sell, all within Simply Wall St’s Community page where millions of investors share views. For Garmin, that could mean choosing between a more cautious Fair Value around US$220 that leans on concerns about smartphone cannibalization and regulation, or a more optimistic Fair Value around US$320 that leans on confidence in AI enabled services and fitness momentum. Each Narrative updates automatically as new news and earnings arrive so your valuation view stays in line with the latest information.

For Garmin however we will make it really easy for you with previews of two leading Garmin Narratives:

Fair value in this bullish narrative: US$320.00

Implied discount to this fair value versus the recent US$241.90 share price: around 24.5% undervalued

Revenue growth assumption: 11.54%

- Leans on faster scaling of subscriptions and software, supported by products such as Garmin Coach, Connect Plus and the MYLAPS acquisition, to support higher margins and earnings.

- Assumes AI driven health features, advanced wearables and expansion into premium verticals such as aviation and marine deepen the ecosystem and support long term demand for devices and services.

- Requires comfort with a higher future P/E of about 37x earnings and analyst expectations for revenue of US$10.1b and earnings of US$2.1b by 2029.

Fair value in this bearish narrative: US$220.00

Implied premium to this fair value versus the recent US$241.90 share price: around 10.0% overvalued

Revenue growth assumption: 7.59%

- Focuses on the risk that smartphones and multipurpose devices absorb more health, fitness and navigation functions, which could weigh on dedicated device demand and pricing power.

- Highlights exposure to regulation, commoditization and niche sectors such as aviation and marine, which could add cost and earnings volatility even as the company invests in new offerings.

- Builds in more moderate growth and a lower future P/E of about 26x earnings, with revenue assumptions of US$9.3b and earnings of US$2.1b by 2029.

Whichever story feels closer to your own view, the key is to test the revenue, margin and multiple assumptions against what you believe about Garmin’s products, competitors and end markets, then decide where the current price sits against your personal fair value range.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Garmin on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Garmin? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.