Is It Too Late To Consider China Yuchai International (CYD) After A 196% One-Year Surge?

China Yuchai International Limited CYD | 0.00 |

- For readers considering whether China Yuchai International at around US$50 is still offering value after a strong run, or if the easy gains are behind it, this article breaks down what the current price might be implying about the stock.

- The stock has posted returns of 8.1% over the past week, 15.6% over the past month, 35.1% year to date and 196.6% over the past year, which has sharpened the focus on both potential upside and changing risk.

- Recent news coverage has centered on China Yuchai International's position within the Machinery industry and how investors are interpreting its prospects compared with peers. Headlines have also highlighted the scale of its share price move over the last three years, which is described as very large, putting extra attention on whether the current valuation still looks sensible.

- On Simply Wall St's valuation checks, China Yuchai International scores 4 out of 6, and the next sections walk through what different valuation approaches suggest about the stock and point to an even more complete way to think about value at the end of the article.

Approach 1: China Yuchai International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today’s value. It focuses on the cash that could theoretically flow to shareholders over time, adjusted for risk.

For China Yuchai International, the 2 Stage Free Cash Flow to Equity model starts with last twelve months Free Cash Flow of about CN¥2.1b. Analysts provide near term estimates and Simply Wall St then extrapolates further out. For example, Free Cash Flow is projected at CN¥883m in 2026, CN¥1,326m in 2027 and CN¥1,477m in 2028, with additional estimates extending to 2035 using a tapering pattern supplied in the model.

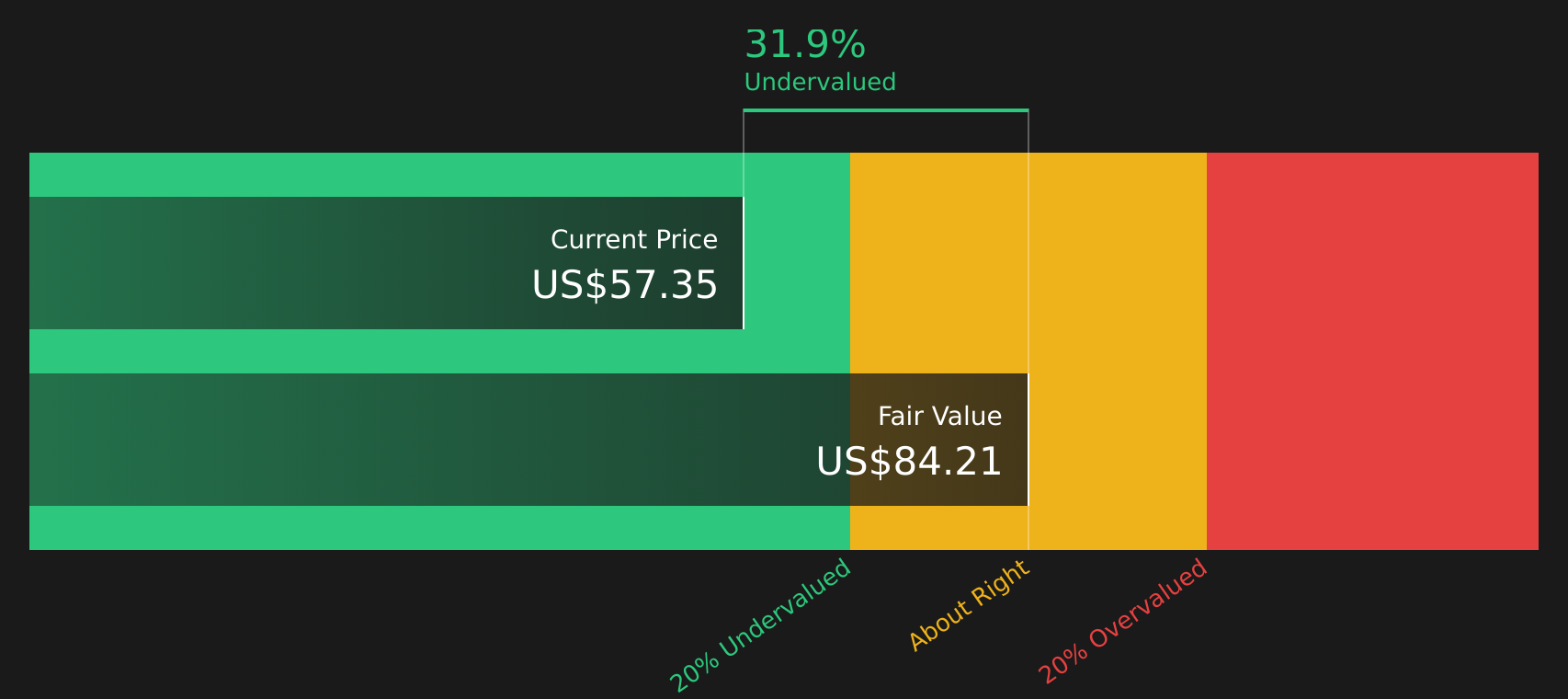

After discounting these projected cash flows back to today, the model arrives at an estimated intrinsic value of US$83.28 per share. Compared with a current share price around US$50, the DCF output suggests the stock trades at roughly a 40.0% discount, which indicates potential upside if these cash flow assumptions hold over time.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests China Yuchai International is undervalued by 40.0%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: China Yuchai International Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to link what you pay for the stock to the earnings it currently generates. The level of P/E that looks reasonable tends to depend on what investors expect for future earnings growth and how much risk they see in those earnings, with higher growth or lower perceived risk often supporting higher P/E levels.

China Yuchai International is trading on a P/E of 23.8x, compared with the Machinery industry average of about 25.9x and a peer average of 19.8x. Simply Wall St also provides a “Fair Ratio” for the stock of 31.7x. This is a proprietary estimate of what the P/E might be based on factors such as the company’s earnings growth profile, industry, profit margins, market capitalization and risk characteristics.

Because the Fair Ratio incorporates these company specific factors, it can give you a more tailored reference point than a simple comparison with peers or the broad industry. Setting China Yuchai International’s actual P/E of 23.8x against the Fair Ratio of 31.7x suggests the stock is trading below that calibrated level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your China Yuchai International Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced, which let you attach a clear story about China Yuchai International to the numbers you see by linking a view on its future revenue, earnings and margins to a specific forecast and Fair Value that you can access on Simply Wall St’s Community page. You can then compare this Fair Value with the current share price to help you decide whether the stock looks attractive or expensive for your own goals, and see it automatically refreshed when new information such as earnings or news arrives. For example, one investor might align with a more cautious view that ties a Fair Value of about US$45.00 to assumptions such as an 11.3% annual revenue growth rate, a 3.1% profit margin and a 14.0x future P/E. Another might side with a more optimistic view using a Fair Value closer to US$64.80, 11.1% annual revenue growth, a 3.1% margin and a 20.3x future P/E. Both Narratives give you a structured, comparable way to see how different stories about the same company translate into different Fair Values.

For China Yuchai International, however, we will make it really easy for you with previews of two leading China Yuchai International Narratives:

Fair Value: US$64.80

Implied discount to this Fair Value at around US$50: about 23% below that narrative Fair Value

Revenue growth assumption: 11.1% a year

- Focuses on higher earnings potential from expansion in high horsepower engines, emerging markets and alternative fuel products.

- Assumes improved supply chain efficiency and strong OEM relationships support a larger, more recurring revenue base and higher margins.

- Backs a Fair Value of US$64.80, tied to expectations for CN¥33.8b of revenue, CN¥1.1b of earnings and a 20.3x P/E around 2029 under an 8.7% discount rate.

Fair Value: US$45.00

Implied premium to this Fair Value at around US$50: about 11% above that narrative Fair Value

Revenue growth assumption: 11.3% a year

- Highlights risks from reliance on diesel engines, exposure to electrification trends, geopolitical frictions and supply chain constraints.

- Assumes revenue and earnings growth but at a lower future P/E of 14.0x, reflecting concerns about long term relevance and pricing power.

- Anchors a Fair Value of US$45.00, tied to CN¥34.0b of revenue, CN¥1.1b of earnings and an 8.8% discount rate, with the current price seen close to that level.

If you want to see how other investors are framing the trade off between these bullish and cautious views, and how their Fair Values update as new data comes in, it is worth reading the full narratives side by side before you make any moves.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for China Yuchai International on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for China Yuchai International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.