Is It Too Late To Consider Delek Logistics Partners (DKL) After A 40% One-Year Rally?

Delek Logistics Partners LP DKL | 50.28 | -0.34% |

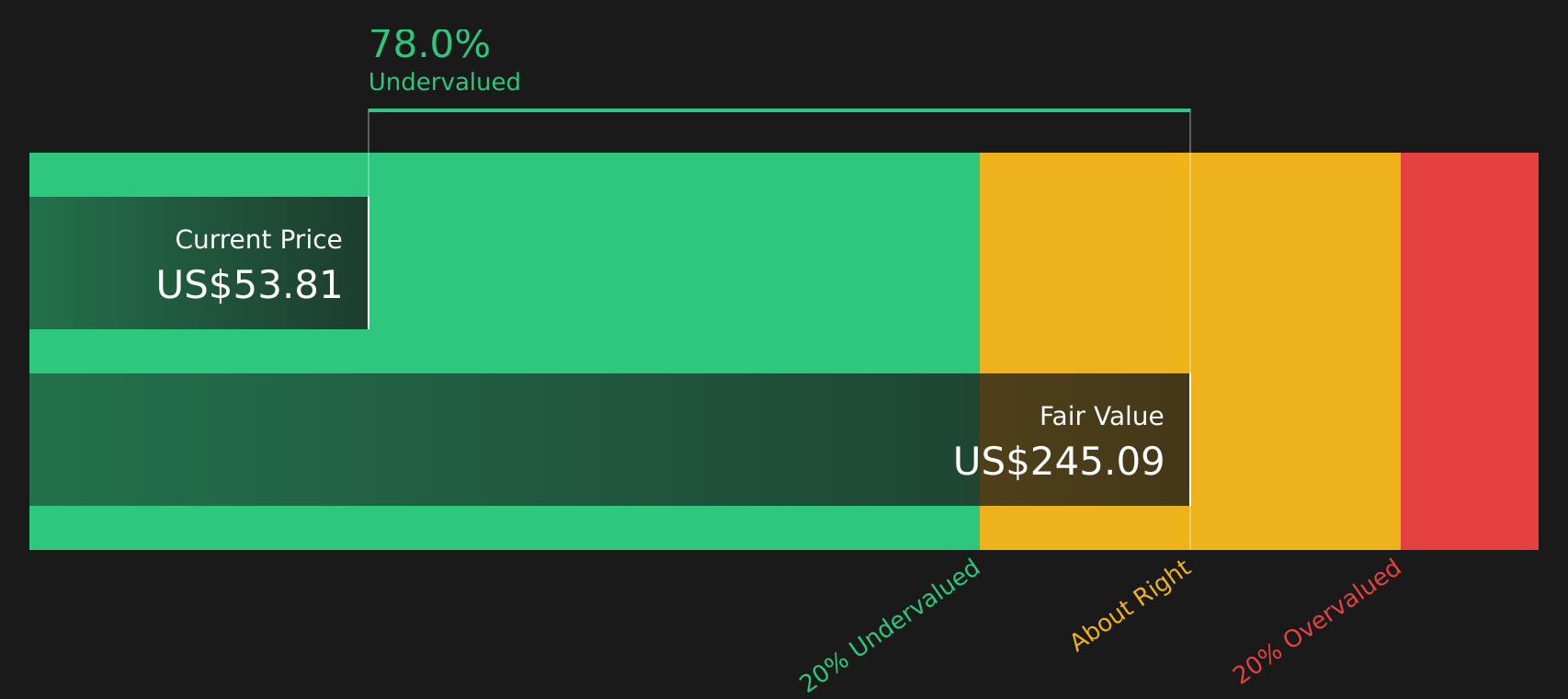

- If you are wondering whether Delek Logistics Partners is still fairly priced after its recent run, the starting point is to look closely at what the current market price might already be assuming.

- The units closed at US$52.05, with a 0.2% move over the last week, a 1% decline over the last 30 days, and returns of 10.7% year to date and 40.1% over the past year, which will naturally have some investors questioning how much value is left on the table.

- These returns sit alongside a longer track record that includes 35.8% over 3 years and 123.3% over 5 years. These figures keep the stock on many income and infrastructure watchlists. This mix of shorter term softness and longer term strength is a useful backdrop as you think about what the current price implies.

- On our structured checks Delek Logistics Partners scores a 3 out of 6 valuation score, which suggests some aspects of the market price look more attractive than others. Next we will walk through the main valuation approaches, then finish with a way to look at value that ties everything together.

Approach 1: Delek Logistics Partners Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth by projecting the cash it could generate in the future and then discounting those cash flows back to today using a required return.

For Delek Logistics Partners, the model uses a 2 Stage Free Cash Flow to Equity approach built on cash flow projections. The latest twelve month free cash flow is about $62.5 million. Analysts provide explicit forecasts for the next few years, and Simply Wall St extends those out so that free cash flow reaches a projected $1.1b in 2035, with interim estimates such as $152.7 million in 2026 and $298.2 million in 2027, all in $ terms.

When these projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $343.71 per unit. Compared with the recent market price of $52.05, this implies the units are 84.9% undervalued according to this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Delek Logistics Partners is undervalued by 84.9%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: Delek Logistics Partners Price vs Earnings

For a profitable business like Delek Logistics Partners, the P/E ratio is a useful way to think about value because it directly links what you pay for each unit with the earnings that support that price. It is a simple shorthand for how many years of current earnings the market is willing to pay for today.

What counts as a reasonable P/E usually reflects two big forces: how fast earnings are expected to grow and how risky or cyclical those earnings might be. Higher expected growth or lower perceived risk can support a higher multiple, while more uncertainty can justify a lower one.

Delek Logistics Partners currently trades on a P/E of 15.78x. That sits above the peer average of 13.68x and close to the Oil and Gas industry average of 15.23x. Simply Wall St’s proprietary Fair Ratio for Delek Logistics Partners is 21.21x, which is an estimate of what the P/E might be based on factors such as earnings growth, profit margins, industry, market cap and company specific risks.

The Fair Ratio helps more than simple peer or industry comparisons because it adjusts for the company’s own characteristics rather than assuming all businesses in the group deserve similar multiples. With a Fair Ratio of 21.21x versus the current 15.78x, the P/E suggests the units may be trading below this Fair Ratio based view of value.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Delek Logistics Partners Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, where you put your own story about Delek Logistics Partners into a simple forecast that links what you believe about future revenue, earnings and margins to a Fair Value you can compare with today’s price. You can see how different views look side by side. For example, one investor might use the more optimistic Fair Value of US$55.00, while another leans toward the lower US$36.00 view. Each Narrative updates automatically as new earnings or news arrive so you can keep checking whether the price still lines up with your assumptions.

For Delek Logistics Partners, however, we will make it really easy for you with previews of two leading Delek Logistics Partners Narratives:

Fair value in this bullish Narrative: US$55.00 per unit

Implied pricing gap vs last close: about 5.4% below this Narrative fair value

Analyst revenue growth assumption used in this Narrative: 6.47% a year

- Focuses on the build out of sour gas handling at the Libby Complex and the wider Delaware gas business as long term earnings and EBITDA drivers.

- Assumes a combined crude, gas and water offering in the Permian Basin and a higher mix of third party EBITDA will support revenue diversity and resilience.

- Links bullish views on revenue, margins and earnings in 2029 to a Fair Value of US$55.00, while flagging risks around utilization, regulation, capital allocation and competition.

Fair value in this more cautious Narrative: US$45.75 per unit

Implied pricing gap vs last close: about 13.8% above this Narrative fair value

Analyst revenue growth assumption used in this Narrative: 6.24% a year

- Highlights the commissioning of Libby 2, water system integrations and fee based contracts as supportive for earnings, but also ties them to higher capital intensity and leverage.

- Emphasizes exposure to fossil fuel demand, customer concentration and potential regulatory and competitive pressure that could weigh on margins and utilization over time.

- Arrives at a Fair Value of US$45.75 that is anchored in analyst consensus assumptions for revenue, earnings, future P/E and discount rate, while stressing that investors should test these inputs against their own view.

Do you think there's more to the story for Delek Logistics Partners? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.