Is It Too Late To Consider DHT Holdings (DHT) After Its Strong 1-Year Rally?

DHT Holdings, Inc. DHT | 0.00 |

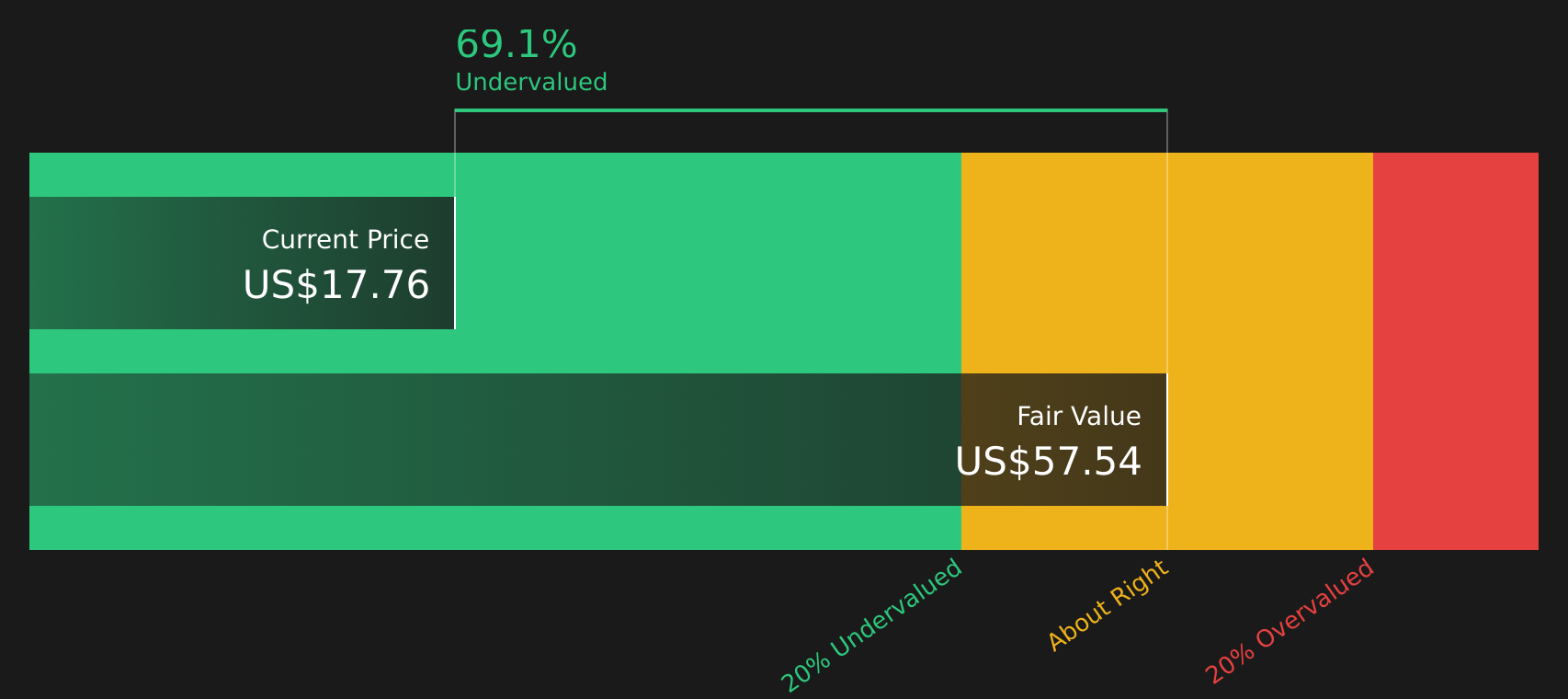

- If you are wondering whether DHT Holdings at around US$19.10 is still good value or already pricing in a lot of optimism, the starting point is to look closely at what the market is paying for its fundamentals.

- The stock has recently posted returns of 4.4% over 7 days, 2.4% over 30 days, 62.7% year to date and 83.0% over the last year. This naturally raises questions about how much of the story is already reflected in the price.

- Recent news coverage has focused on DHT Holdings in the context of ongoing interest in energy and shipping stocks, as investors reassess where they want exposure within the sector. This backdrop helps explain why the stock has attracted more attention and why valuation is now a key question.

- DHT Holdings currently has a valuation score of 5/6, which suggests most of the standard checks point to the stock being undervalued. The next step is a closer look at the usual approaches to valuation and, by the end of the article, a more complete way to think about what the stock might be worth.

Approach 1: DHT Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today’s value using a required rate of return.

For DHT Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow (FCF) is $101.39 million. Analyst and extrapolated estimates point to FCF of $442.00 million in 2026 and $386.00 million in 2028, with further projections out to 2035 provided by Simply Wall St. All of these are in US dollars.

When these projected cash flows are discounted back and combined, the DCF model suggests an intrinsic value of $57.42 per share. Compared with the recent share price around $19.10, this implies the stock is trading at a 66.7% discount to that estimated value. On this model alone, the shares appear materially undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DHT Holdings is undervalued by 66.7%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: DHT Holdings Price vs Earnings

For profitable companies, the P/E ratio is a useful way to check how much you are paying for each dollar of earnings. It captures what the market is willing to pay today relative to current profits, which is often a key anchor for valuation.

What counts as a "normal" P/E depends on how investors see growth potential and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to be associated with a lower P/E.

DHT Holdings currently trades on a P/E of 14.57x. That is slightly below the Oil and Gas industry average of 14.72x and below the peer group average of 15.56x. Simply Wall St also provides a proprietary “Fair Ratio” of 16.36x, which reflects what the P/E might be based on factors such as earnings growth, industry, profit margins, market cap and risk profile.

This Fair Ratio can be more informative than a simple comparison with peers or the industry because it adjusts for company specific characteristics rather than assuming all stocks deserve the same multiple. Comparing DHT Holdings current P/E of 14.57x with the Fair Ratio of 16.36x indicates that the shares may be undervalued on this approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your DHT Holdings Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced here as your way of attaching a clear story about DHT Holdings to the numbers you think are reasonable for its future revenue, earnings and margins, turning that story into a financial forecast and a fair value you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are presented as an easy tool used by millions of investors. They allow you to set assumptions, see the resulting fair value, and quickly judge whether the current price makes DHT look cheap or expensive for your particular view.

Because Narratives update automatically when new information appears, such as earnings results, charter announcements or analyst targets, your fair value view stays aligned with the latest data rather than a one off calculation.

For DHT Holdings, one investor Narrative might lean closer to the higher fair value around US$36 that assumes stronger earnings and a higher multiple. Another might sit nearer the lower fair value around US$16.70 that assumes slower revenue, a lower P/E of 12.9x and more conservative expectations. Comparing each of these fair values to the current share price can help you decide whether to buy, hold or sell based on which story you find more convincing.

For DHT Holdings, we will make it really easy for you with previews of two leading DHT Holdings Narratives:

Both are built on the same underlying data, but they tell very different stories about what the current price around US$19.10 might mean for you. Use them as starting points, then decide which assumptions feel closer to how you see the business and the tanker market.

Fair value: US$36.00

Implied discount to this narrative: 46.9%

Assumed revenue growth: 31.06%

- Focuses on DHT Holdings as a high spot exposure VLCC operator positioned to benefit when tanker day rates are strong and volatile.

- Builds a case around recent very high rate prints, one year charters reportedly above US$100,000 per day and the impact of route disruptions through the Strait of Hormuz on vessel demand.

- Arrives at a fair value of about US$36 per share using earnings estimates and P/E comparisons with other VLCC companies, which is higher than the recent share price.

Fair value: US$16.70

Implied premium to this narrative: 14.4%

Assumed revenue growth: 3.89% decline

- Emphasizes the risks of leaning heavily into spot market exposure if freight demand or charter appetite cools from current levels.

- Highlights concerns around vessel supply, newbuild commitments and how changes in crude trade flows or policy could pressure day rates and earnings quality over time.

- Uses analyst assumptions on revenue, margins, earnings and a future P/E of 12.9x to support a fair value around US$16.70, which is below the recent share price.

Together, these narratives frame a fair value range from about US$16.70 to US$36.00. Where you come out inside that range depends on how confident you are in sustained high VLCC rates, DHT Holdings capital allocation and the longer term balance between fleet supply and seaborne crude demand.

If you want to see the full assumptions, numbers and risk checks behind each of these views and compare them with your own, head over to the Community Narratives for DHT Holdings and stress test the story that best fits your expectations.

Do you think there's more to the story for DHT Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.