Is It Too Late To Consider Diamondback Energy (FANG) After Its Recent Share Price Run?

Diamondback Energy, Inc. FANG | 186.51 | -1.37% |

- Wondering if Diamondback Energy is still priced attractively after its recent run, or if most of the upside is already on the table? This article looks at what the current share price might be implying about value.

- The stock last closed at US$169.14, with returns of 2.6% over 7 days, 11.8% over 30 days, and 11.0% both year to date and over the past year. This may signal changing views on its risk and return profile.

- Recent coverage has focused on Diamondback Energy as a key US energy player, with investors watching how it positions itself within the sector and manages its capital allocation. These themes help frame how the market could be thinking about the share price today.

- Based on our checklist of six valuation tests, Diamondback Energy currently scores 5 out of 6. This raises the question of whether traditional metrics tell the full story, or if there is a more complete way to think about value that we will come back to at the end of this article after walking through the main valuation approaches.

Approach 1: Diamondback Energy Discounted Cash Flow (DCF) Analysis

A DCF model estimates what a company might be worth by projecting the cash it could generate in the future, then discounting those cash flows back to today to get a present value per share.

For Diamondback Energy, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $423.1 million. Analyst inputs underpin projections for the next few years, and beyond that Simply Wall St extrapolates estimates, with Free Cash Flow for 2030 projected at $5.9b.

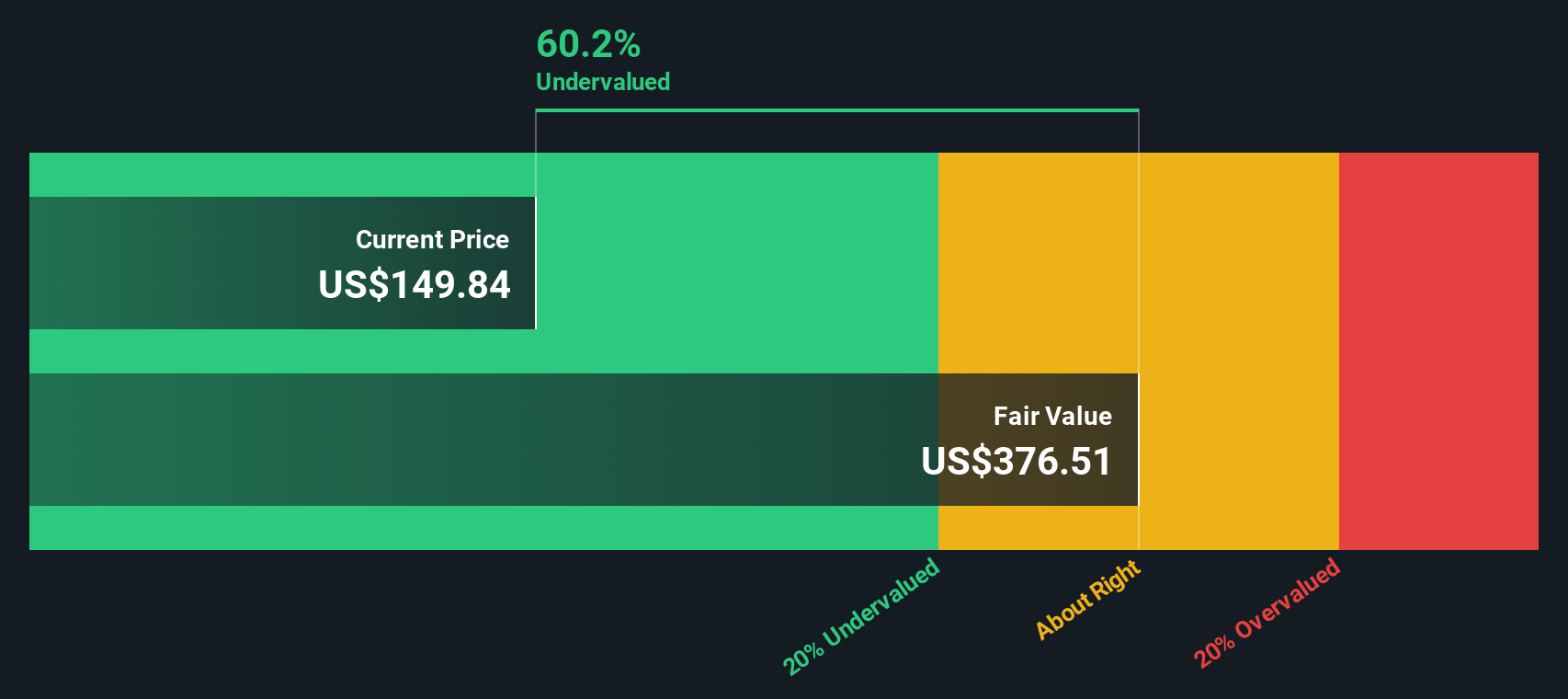

After discounting each year’s projected cash flow, the model arrives at an estimated intrinsic value of about $491.74 per share. Compared with the recent share price of US$169.14, this implies an intrinsic discount of 65.6%, which indicates that, on these cash flow assumptions, the shares appear undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Diamondback Energy is undervalued by 65.6%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

Approach 2: Diamondback Energy Price vs Earnings

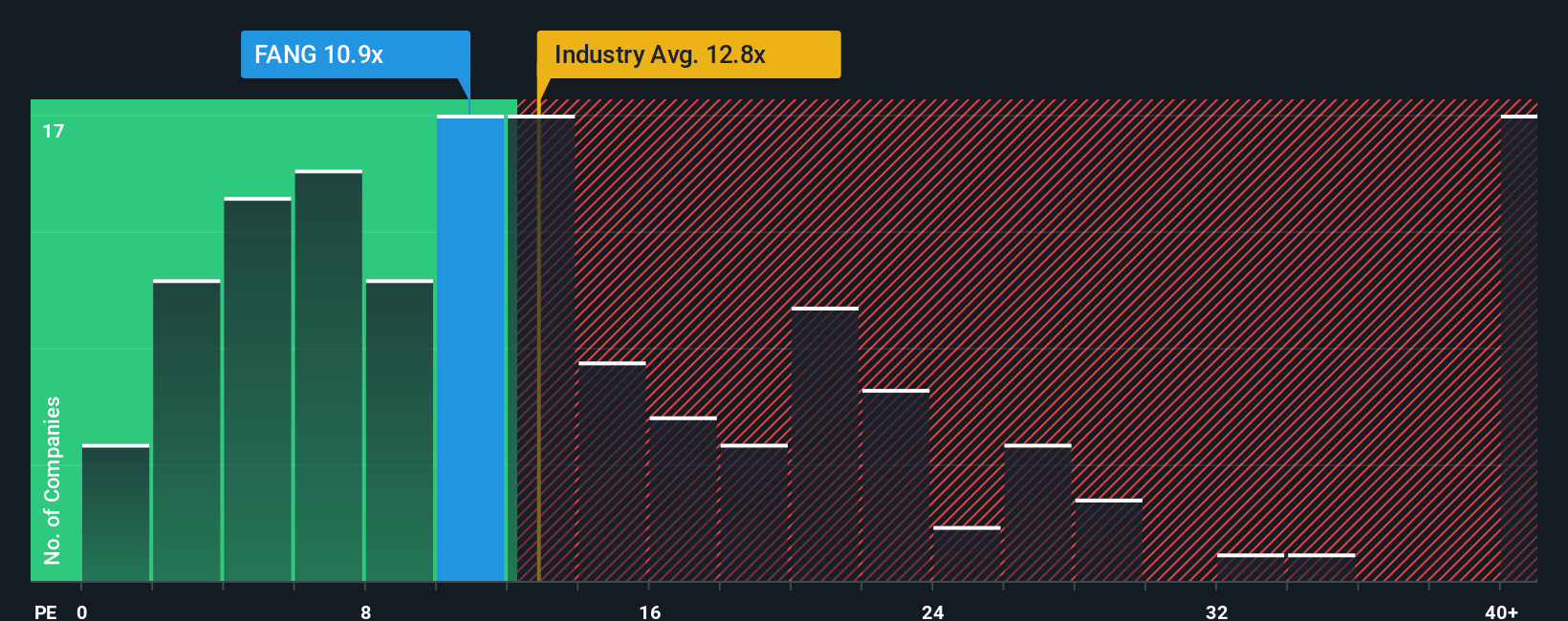

For profitable companies, the P/E ratio is often a useful shorthand because it links what you pay for each share directly to the earnings that the business is currently generating.

What counts as a "normal" or "fair" P/E really depends on how the market views a company’s growth potential and risk, with higher growth or lower perceived risk often justifying a higher multiple, and the reverse also holding true.

Diamondback Energy currently trades on a P/E of 11.59x. That sits below the Oil and Gas industry average of 14.46x and well below the peer group average of 23.92x. Simply Wall St also provides a proprietary Fair Ratio of 20.23x, which is the P/E level suggested by factors such as the company’s earnings growth profile, profit margins, industry, market cap and its specific risks.

This Fair Ratio aims to be more tailored than a simple peer or industry comparison because it adjusts for the mix of growth, risk and profitability that is specific to Diamondback Energy rather than assuming all Oil and Gas companies are directly comparable.

Comparing the current P/E of 11.59x with the Fair Ratio of 20.23x, the shares appear undervalued on this multiple based approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Diamondback Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which Simply Wall St hosts on its Community page for millions of investors. There you can set out your own story for Diamondback Energy, link that story to specific assumptions for future revenue, earnings, margins and P/E, and arrive at a Fair Value you can compare to today’s share price. All of this updates automatically as new news or earnings arrive. A more cautious investor might lean toward a lower Fair Value around US$158 based on more conservative margins and growth. A more optimistic investor might use assumptions closer to US$207. These two Narratives will each give a clear, numbers backed view of whether the current price around US$169.14 looks high, low or about right for their own decision making.

For Diamondback Energy, however, we will make it really easy for you with previews of two leading Diamondback Energy Narratives:

These give you a clear bullish and cautious view built from different assumptions on revenue, margins and the P/E the market might be willing to pay.

Fair value: US$207.41 per share

Implied discount to this narrative: about 18.4% versus the recent price of US$169.14, using ((207.41 - 169.14) / 207.41)

Revenue growth assumption: 138.29% a year

- Focuses on higher margins and strong cash generation supported by operational efficiency, capital allocation and acquisitions in the Permian Basin.

- Assumes revenue growth, slightly higher profit margins over time and a higher future P/E multiple to arrive at a bullish fair value of US$235.44 and a narrative fair value of about US$207.41.

- Flags risks around the global renewables push, ESG pressures, concentration in the Permian, ongoing capital needs and reserve depletion, and encourages you to test whether those assumptions fit your own view.

Fair value: US$158.00 per share

Implied premium to this narrative: about 7.1% versus the recent price of US$169.14, using ((169.14 - 158.00) / 158.00)

Revenue growth assumption: 139.84% a year

- Builds a more cautious case where growth leans heavily on scale efficiencies and acquisitions, with greater focus on capital and operational constraints.

- Assumes lower future profit margins, different earnings outcomes and a higher future P/E multiple to reach a fair value of US$158, even while some analyst targets still sit above the market price.

- Highlights risks around dependence on share repurchases, capital spending efficiency, asset sale execution, power costs in the Permian and the challenge of sustaining free cash flow breakeven improvements.

If you want to go beyond a single number and see how other investors are weighing these kinds of trade offs, Curious how numbers become stories that shape markets? Explore Community Narratives can help you put Diamondback Energy in context with other ideas you are following.

Do you think there's more to the story for Diamondback Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.