Is It Too Late To Consider EchoStar (SATS) After Last Week’s Share Price Pullback?

EchoStar Corporation Class A SATS | 0.00 |

- Wondering if EchoStar at around US$116 per share still offers value, or if most of the upside is already behind it? This article focuses on what the current price really implies.

- The stock is up a very large amount over the past year. However, it is up 3.7% year to date and has fallen 10% over the past week and 7.5% over the past month. These moves can change how you think about risk and potential entry points.

- Recent coverage has focused on EchoStar’s sharp share price gains and what they might mean for expectations around the business and the satellite and communications sector more broadly. Investors are now paying closer attention to whether those expectations are reflected in the current valuation, or if sentiment has run ahead of fundamentals.

- EchoStar currently has a value score of 2 out of 6. This article will walk through what different valuation approaches say about the stock today, and will finish by looking at a broader way to think about value that goes beyond a single model or metric.

EchoStar scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

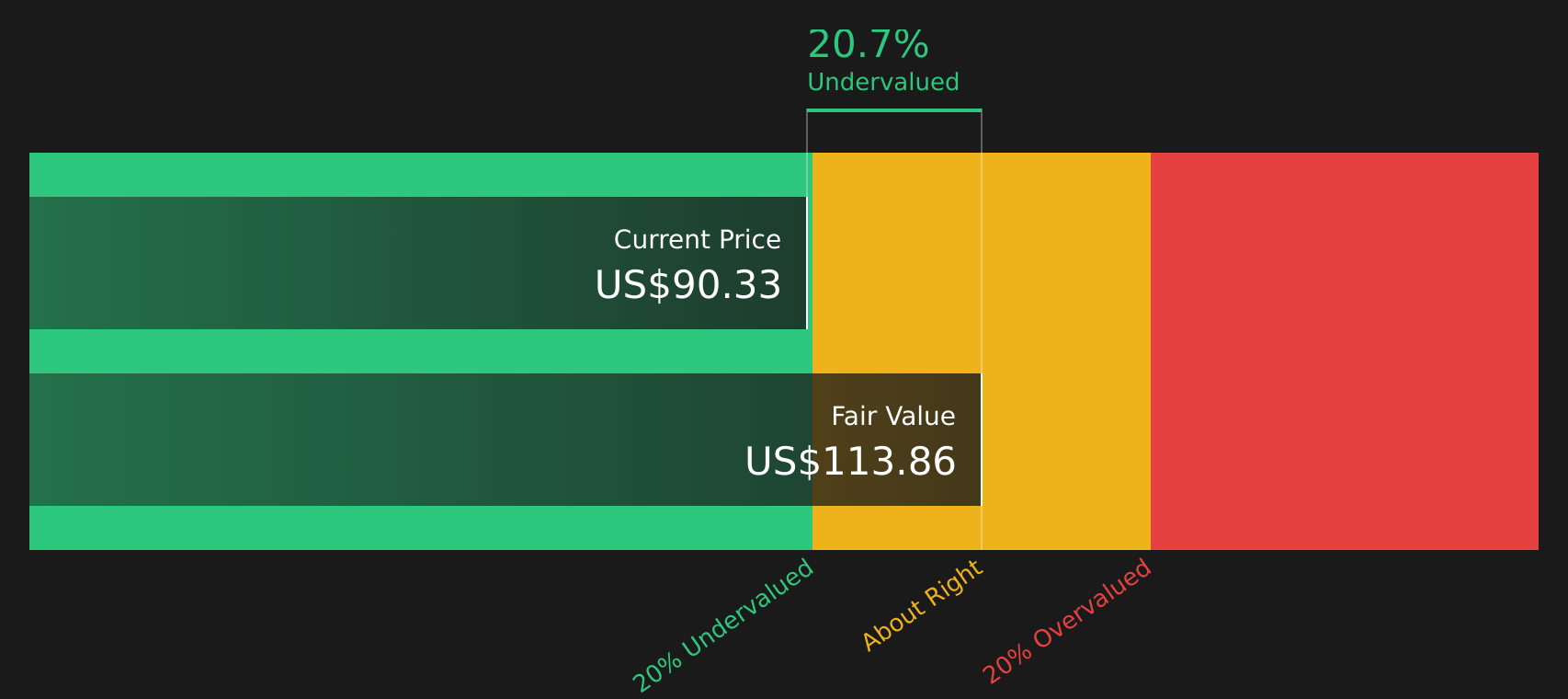

Approach 1: EchoStar Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth today by projecting the cash it could generate in the future and then discounting those cash flows back to a present value.

For EchoStar, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company recently reported free cash flow of a loss of $2.446b. Analyst and extrapolated estimates point to projected free cash flow of $1.911b in 2030, with a path that includes $184.0m in 2026, $1.003b in 2027 and $1.823b in 2028, all in $ and already discounted back to today in the model.

Bringing all those projected cash flows together, the DCF output indicates an estimated intrinsic value of about $116.94 per share. Against a recent share price around $116, this implies the stock is about 0.6% undervalued, which suggests the current price and the DCF estimate are very close.

Result: ABOUT RIGHT

EchoStar is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: EchoStar Price vs Sales

For companies where earnings move around or are temporarily depressed, focusing on revenue can be more useful, which is why the P/S ratio is often the preferred multiple. It relates what you pay for each dollar of sales and can be compared across similar businesses.

In general, higher expected growth and lower perceived risk can support a higher “normal” P/S ratio, while slower expected growth or higher risk tends to justify a lower one. That context matters when you compare companies.

EchoStar currently trades on a P/S of 2.28x. This is above the broader Media industry average of 1.09x, but below the peer group average of 3.16x. Simply Wall St’s “Fair Ratio” for EchoStar is 1.33x, which is a proprietary estimate of what the P/S might be given factors such as earnings growth, industry, profit margins, market cap and risks.

This Fair Ratio can be more informative than a simple comparison with peers or the industry, because it adjusts for EchoStar’s own characteristics rather than assuming it should look like an average company. Compared with the current 2.28x P/S, the 1.33x Fair Ratio points to EchoStar trading above that modelled range.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your EchoStar Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and that is where Narratives come in as a simple story that you choose to sit behind the numbers like fair value, future revenue, earnings and margins.

On Simply Wall St, Narratives live in the Community page and give you a clear link from a company’s story to a financial forecast and then to a fair value that you can compare directly with the current share price when you are deciding whether the stock looks expensive or cheap against your own view.

Narratives update automatically when new information such as news or earnings is added to the platform, so if EchoStar’s situation changes, the underlying assumptions and fair value ranges shift too without you having to rebuild a model from scratch.

For EchoStar, one investor on the platform has built a very optimistic Narrative with a fair value of about US$147 per share, while another more cautious Narrative sits closer to US$43.91 per share. Seeing those side by side helps you decide which story and set of assumptions is closest to how you see the company today.

For EchoStar, however, we will make it really easy for you with previews of two leading EchoStar Narratives:

Together they frame the current share price in very different ways and give you a clear sense of the assumptions other investors are using when they think about value and risk.

Fair value in this Narrative: US$120.00

Current price vs this fair value: about 3.1% below the Narrative fair value, so the stock is slightly below this author's estimate.

Revenue trend assumption: revenue declines about 3.15% per year.

- Focuses on regulatory uncertainty around spectrum rights, high debt and looming maturities that could limit flexibility and raise financial risk.

- Assumes revenue falls and profitability remains pressured for several years, with the valuation relying on profit margins eventually aligning with the broader US Media sector.

- Still gives weight to EchoStar's spectrum, technology and partnerships, which could support new services if execution and industry conditions improve.

Fair value in this Narrative: US$43.91

Current price vs this fair value: about 164.8% above the Narrative fair value, which frames the stock as trading well above this author's estimate.

Revenue trend assumption: revenue declines about 2.30% per year.

- Highlights EchoStar's legacy financial challenges and treats the shift into a space focused holding structure as a major change in how investors might think about the stock.

- Places a lot of emphasis on indirect exposure to SpaceX and the broader space economy, with value concentrated in that stake and in net cash.

- Points to index inclusion and potential partnerships as supportive factors, while flagging that enthusiasm around other Musk related ventures could influence how the market values that exposure.

Seeing these Narratives side by side helps you decide which story, risk profile and fair value range lines up closest with how you see EchoStar today, and whether the current price feels high, low or about right against your own assumptions.

To go further and test your own view against the community, you can scan the full set of Narratives, look at the underlying forecasts and, if you want, build your own version that reflects your expectations for EchoStar's revenue, margins and fair value over time. See what the community is saying about EchoStar

Do you think there's more to the story for EchoStar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.