Is It Too Late To Consider Energy Transfer (ET) After A 3x Five Year Return?

Energy Transfer LP ET | 0.00 |

- For investors wondering whether Energy Transfer at around US$19.92 still offers value or whether most of the easy gains are already behind it, this article focuses on what the current price might mean for potential investors.

- The stock has had a mixed short term patch, with a 1.3% decline over the last 7 days, a 4.2% gain over 30 days, and year to date and 1 year returns of 20.1% and 25.9% respectively. This sits against a very large 5 year return of around 3x.

- Recent coverage has focused on Energy Transfer's position within the broader US energy sector and how its scale and asset base fit into investor interest in income focused energy infrastructure. Together with ongoing discussion about the stock's long term total return profile, this context helps explain why some investors are reassessing both upside potential and risk at current levels.

- Simply Wall St's valuation model currently gives Energy Transfer a value score of 4 out of 6. The sections that follow break down how different valuation approaches compare, then finish with a framework that can help you think about value more clearly than any single model alone.

Approach 1: Energy Transfer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and discounting them back to today in dollar terms.

For Energy Transfer, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $5.6b. Analyst inputs and extrapolations suggest free cash flow of $7.1b in 2030, with interim projections such as $5.7b in 2026 and $6.6b in 2027, all discounted back to reflect the time value of money.

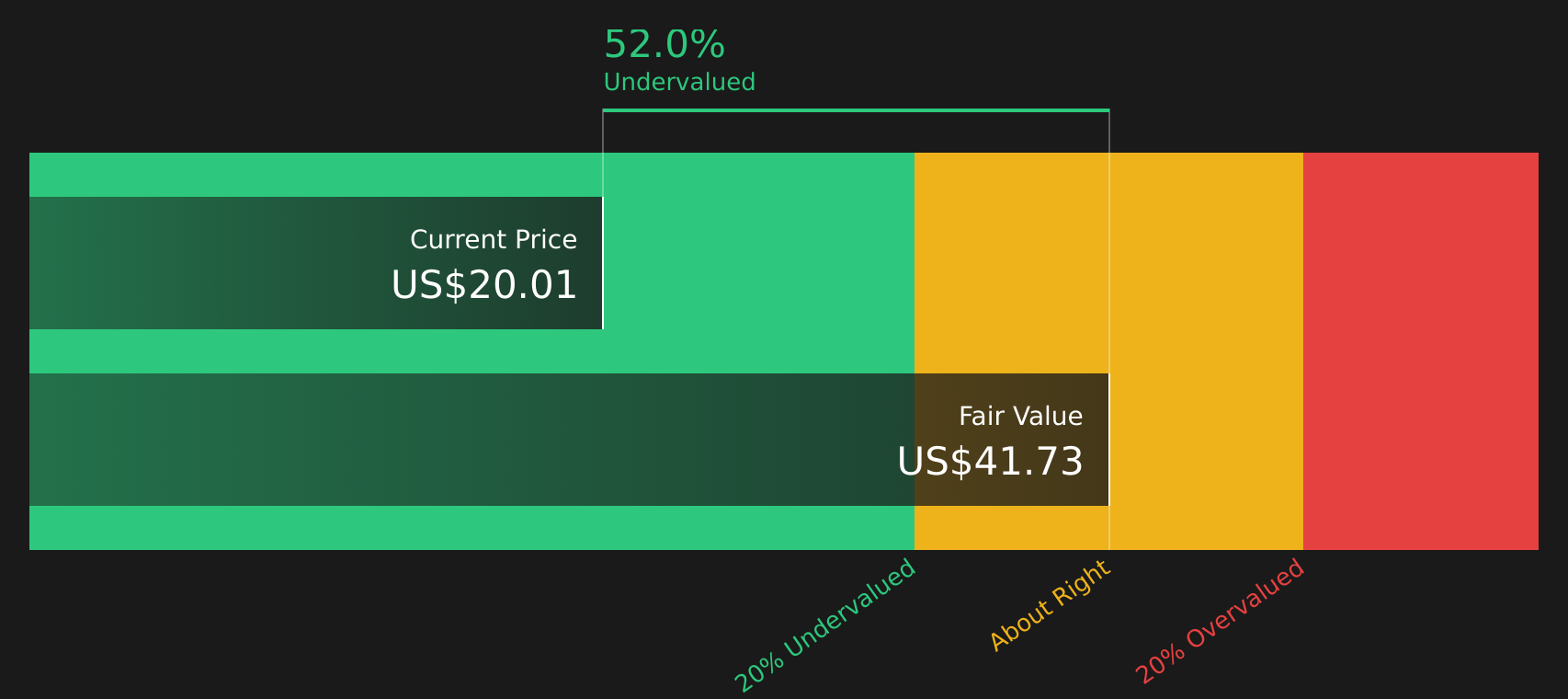

Pulling these projections together, Simply Wall St’s DCF model arrives at an estimated intrinsic value of about $41.64 per share. Versus the current share price of around $19.92, this implies the stock is 52.2% undervalued according to this method.

This is a single model, but on its own it points to a wide gap between price and estimated value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Energy Transfer is undervalued by 52.2%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Energy Transfer Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to link what you pay for the stock to the earnings it generates. This is why it is a commonly used metric for a business like Energy Transfer.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk often aligns with a lower P/E.

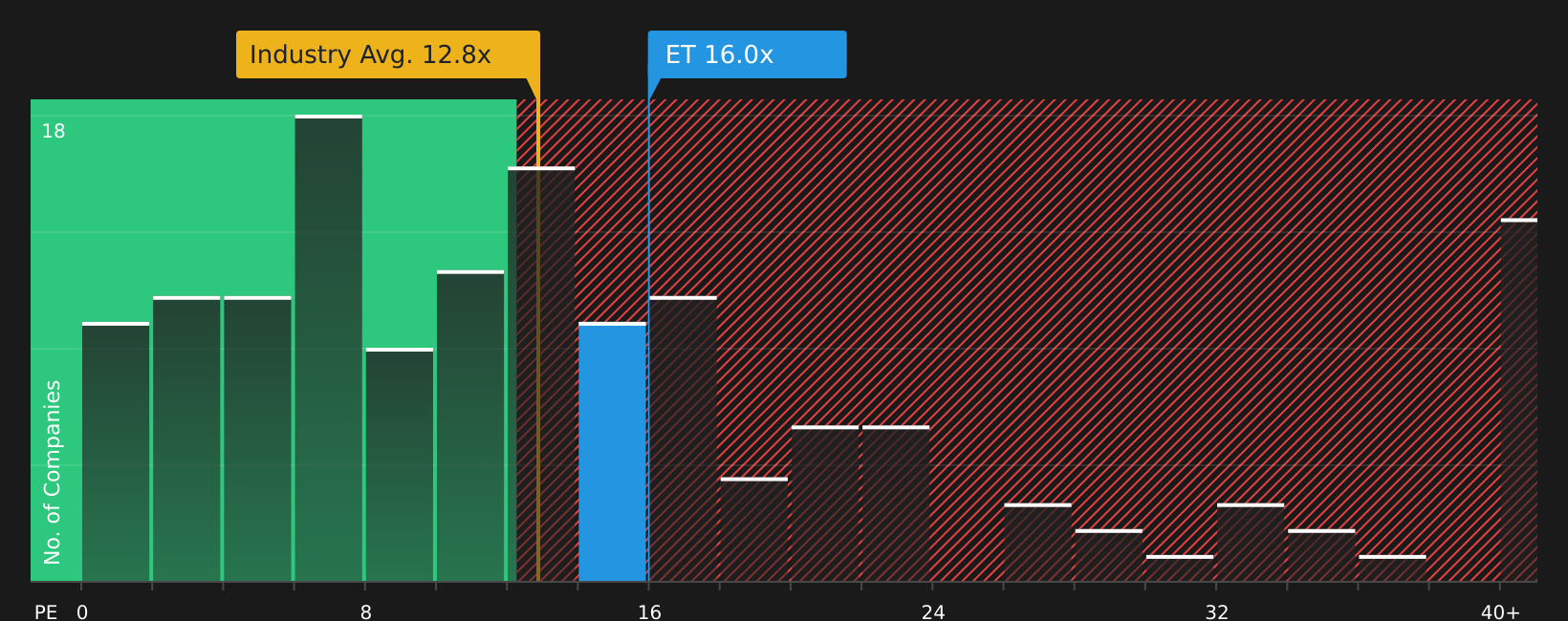

Energy Transfer currently trades on a P/E of 16.67x. This sits above the Oil and Gas industry average P/E of about 13.86x, yet below the peer group average of roughly 18.24x. To go further, Simply Wall St applies a proprietary “Fair Ratio” framework, which estimates what P/E might be reasonable given factors such as earnings growth, industry, profit margins, market capitalisation and company specific risks.

Because it blends these inputs, the Fair Ratio is more tailored than a simple comparison with peers or the broad industry. For Energy Transfer, the Fair Ratio is 29.71x, comfortably above the current 16.67x. This points to the stock trading below this model based reference level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Energy Transfer Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple tool on Simply Wall St’s Community page that lets you connect your view of Energy Transfer’s story with specific assumptions for future revenue, earnings, margins and a fair value estimate. You can then compare that fair value with today’s price, with the system updating your Narrative as new news or earnings arrive. For example, one investor might build a Narrative that leans toward the higher analyst fair value of US$25.00 based on confidence in gas projects and distribution growth. Another might anchor closer to US$19.50 to reflect concerns around project execution and long term demand. Both can see clearly how their story translates into numbers without relying only on one static model.

Do you think there's more to the story for Energy Transfer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.