Is It Too Late To Consider ESCO Technologies (ESE) After A 102% One Year Rally?

ESCO Technologies Inc. ESE | 0.00 |

- Wondering whether ESCO Technologies at around US$318.83 still offers value, or if most of the opportunity is already reflected in the price.

- The stock has posted returns of 6.3% over the last week, 15.2% over the past month, 61.3% year to date and 102.2% over the past year, with a 3 year return of 242.0% and 5 year return of 190.3%.

- Recent coverage has focused on ESCO Technologies as a capital goods player whose share price performance has drawn fresh attention from investors seeking quality industrial names. That interest provides useful context for assessing whether the current price still lines up with fundamentals.

- Despite the strong share price track record, ESCO Technologies currently holds a valuation score of 0/6. The sections that follow will compare different valuation methods and then finish with a simpler way to keep track of value over time.

ESCO Technologies scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

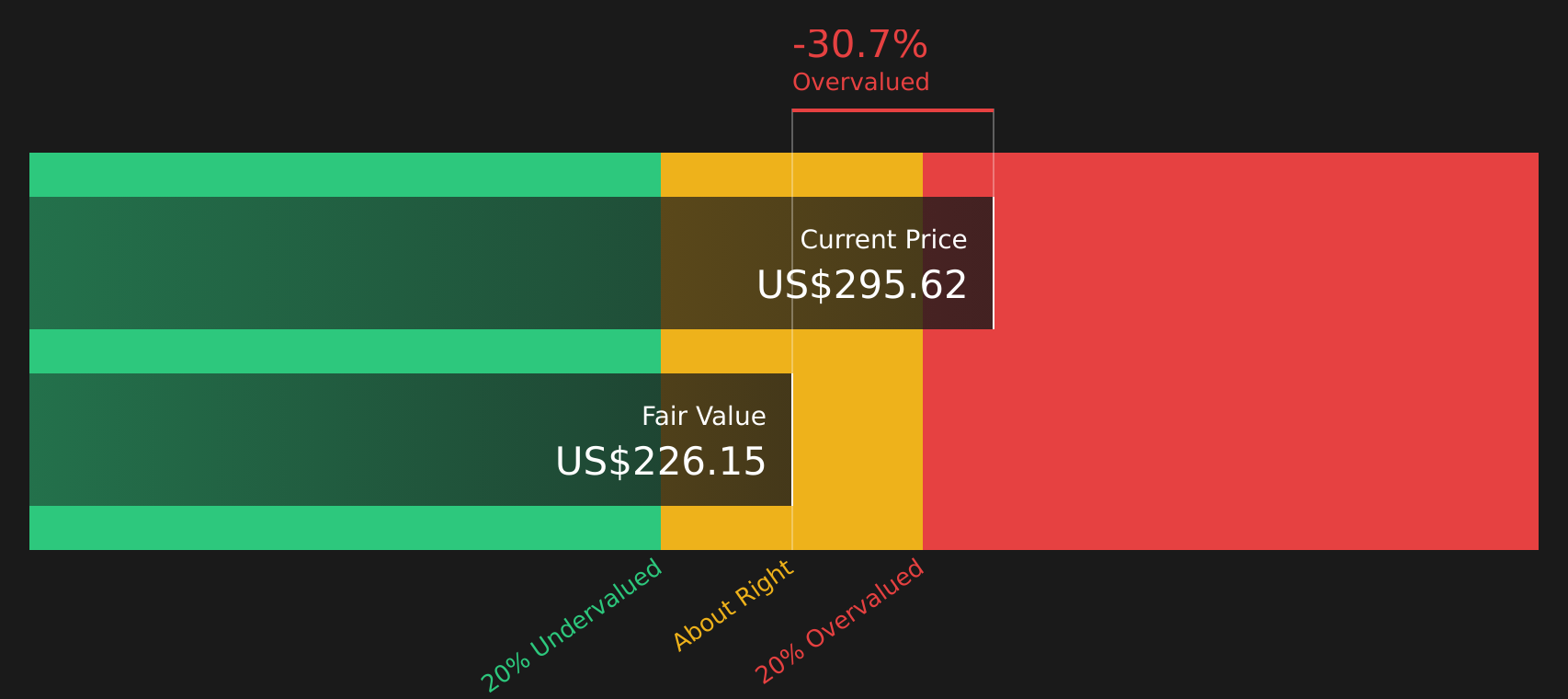

Approach 1: ESCO Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting its future cash flows and then discounting those back to a present value.

For ESCO Technologies, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow (FCF) is about $227.7 million. Analysts provide FCF estimates out to 2027, with Simply Wall St extrapolating further to build a 10 year path. On that basis, projected FCF for 2035 is $314.6 million, all in $.

Discounting those annual cash flows, plus a terminal value, gives an estimated intrinsic value of $181.39 per share. Compared with the current share price of about $318.83, the DCF output suggests the stock is around 75.8% above this estimate. This points to ESCO Technologies trading well above the level implied by these cash flow assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ESCO Technologies may be overvalued by 75.8%. Discover 55 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: ESCO Technologies Price vs Earnings

For a profitable company, the P/E ratio is a useful shorthand for how much you are paying for each dollar of earnings. It lets you compare ESCO Technologies with other businesses on a like for like basis using a single, familiar number.

What counts as a “normal” or “fair” P/E will depend on how quickly earnings are expected to grow and how risky those earnings are perceived to be. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually points to a lower multiple.

ESCO Technologies currently trades on a P/E of 66.22x. That is higher than both the Machinery industry average of 27.24x and the peer average of 29.41x. Simply Wall St’s Fair Ratio for ESCO Technologies is 29.75x, which is a proprietary estimate of what the P/E might be given factors such as earnings growth, profit margins, industry, market cap and risks.

The Fair Ratio aims to be more tailored than a simple comparison with industry or peer averages because it adjusts for these company specific drivers. Since the current 66.22x P/E is well above the 29.75x Fair Ratio, the shares screen as expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your ESCO Technologies Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and this is where Narratives come in. They give you a simple story behind your numbers by linking your view on ESCO Technologies to a financial forecast and then to a Fair Value that you can compare with the current price inside Simply Wall St's Community page. For example, one ESCO Technologies Narrative on the platform might lean toward the lower Fair Value of US$270 based on concerns about margin pressure and supply chain or regulatory costs. Another Narrative might lean toward the higher Fair Value of US$350 based on expectations for stronger recurring revenue from naval programs and electrification. As new information like earnings or guidance arrives, those Narratives and their Fair Values update automatically, helping you decide whether the current price around US$318.83 still fits your own story or not.

For ESCO Technologies, we will make it really easy for you with previews of two leading ESCO Technologies Narratives:

Fair Value: US$350

Implied discount to this Fair Value versus the recent US$318.83 price: about 8.9%.

Revenue growth assumption: 11.08%.

- Sees deeper involvement in U.S. and U.K. naval programs and the AUKUS alliance as a way to build larger, recurring revenue streams and stronger earnings visibility.

- Assumes ongoing R&D, electrification and grid modernization demand, and the Maritime acquisition together support higher margins and a larger addressable market.

- Uses analyst assumptions that earnings and margins rise over time, with the share price reaching US$350 if the business delivers on these growth and profitability targets.

Fair Value: US$270

Implied premium to this Fair Value versus the recent US$318.83 price: about 18.1%.

Revenue growth assumption: 11.21%.

- Focuses on pressure from higher supply chain, regulatory and labor costs, and on the risk that heavier exposure to government and utility contracts leads to more volatile revenues.

- Highlights the threat that automation and digital solutions could gradually reduce demand for ESCO Technologies more traditional hardware focused products.

- Applies analyst assumptions that, even if earnings grow, a Fair Value around US$270 is more appropriate, which is below the recent share price.

These two Narratives bracket the current US$318.83 price and show how different views on contracts, costs and long term growth can lead to very different Fair Values. The next step is to decide which story lines up more closely with your own expectations and risk tolerance, and then track how the thesis unfolds over time using the community tools on Simply Wall St.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for ESCO Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for ESCO Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.