Is It Too Late To Consider First Solar (FSLR) After Its Recent Share Price Surge?

First Solar, Inc. FSLR | 0.00 |

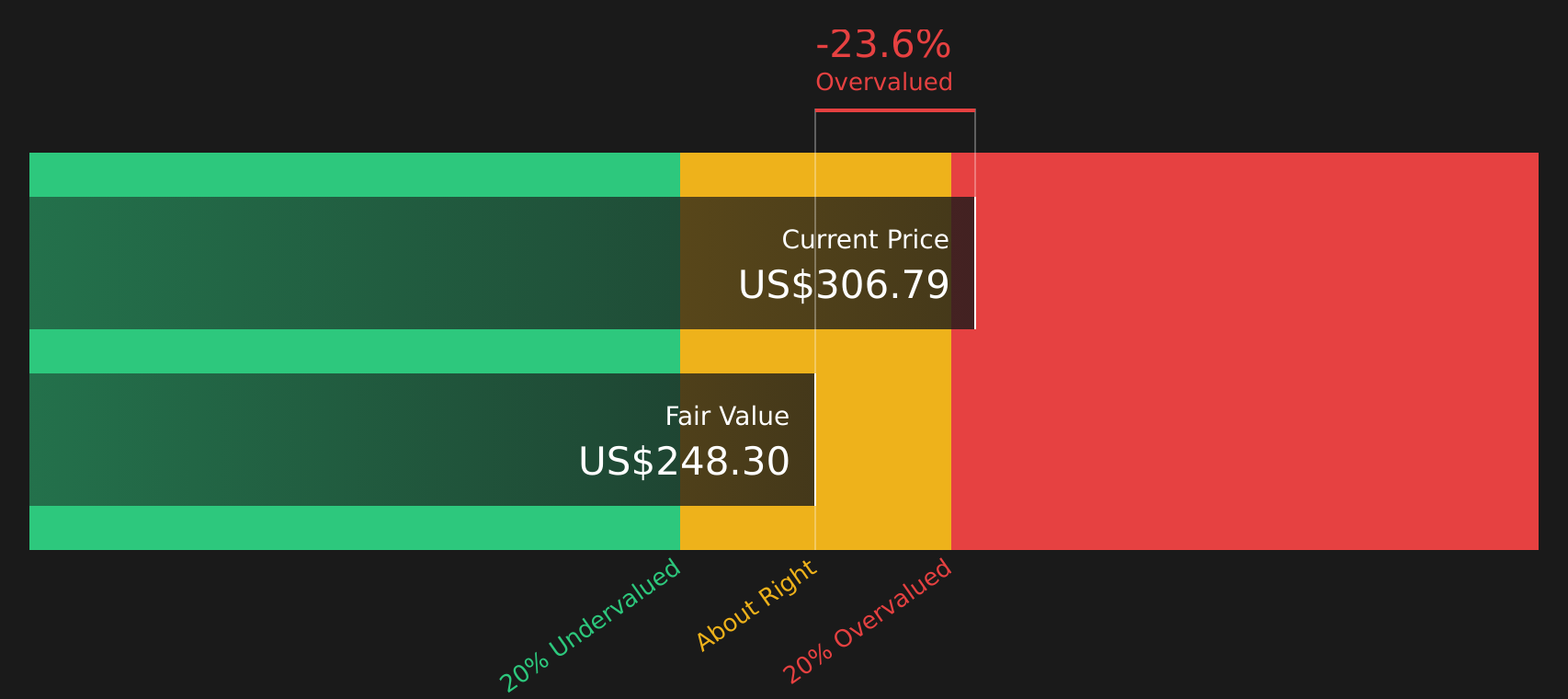

- If you are wondering whether First Solar at around US$306.79 is still sensibly priced or already baking in a lot of optimism, the valuation story is where things start to get interesting.

- The stock has seen sharp recent moves, with returns of 19.0% over 7 days, 61.0% over 30 days, 11.8% year to date, 94.1% over 1 year, 48.4% over 3 years, and 304.5% over 5 years. This naturally raises questions about how much is already reflected in the price.

- Recent coverage around First Solar has focused on its position within the semiconductor and solar technology space, regulatory support for clean energy, and shifting sentiment toward companies tied to energy transition themes. Taken together, these factors help explain why many investors are reassessing both the potential and the risks embedded in the current share price.

- First Solar currently has a valuation score of 3 out of 6. The sections that follow will walk through how common valuation approaches line up with that score, before finishing with a more holistic way to think about what the stock might be worth.

Approach 1: First Solar Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today, so you can compare that value with the current share price.

For First Solar, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s last twelve months Free Cash Flow is about $1.01b. Analyst based projections and subsequent extrapolations by Simply Wall St point to Free Cash Flow of $2.95b in 2030, with detailed estimates and extensions running from 2026 through 2035 in the model.

When all those projected cash flows are discounted back to today, the estimated intrinsic value from this DCF is about $247.93 per share. The current share price is around $306.79, which implies the stock is trading at roughly a 23.7% premium to the DCF estimate. Based on this method alone, the valuation appears to lean to the expensive side.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests First Solar may be overvalued by 23.7%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

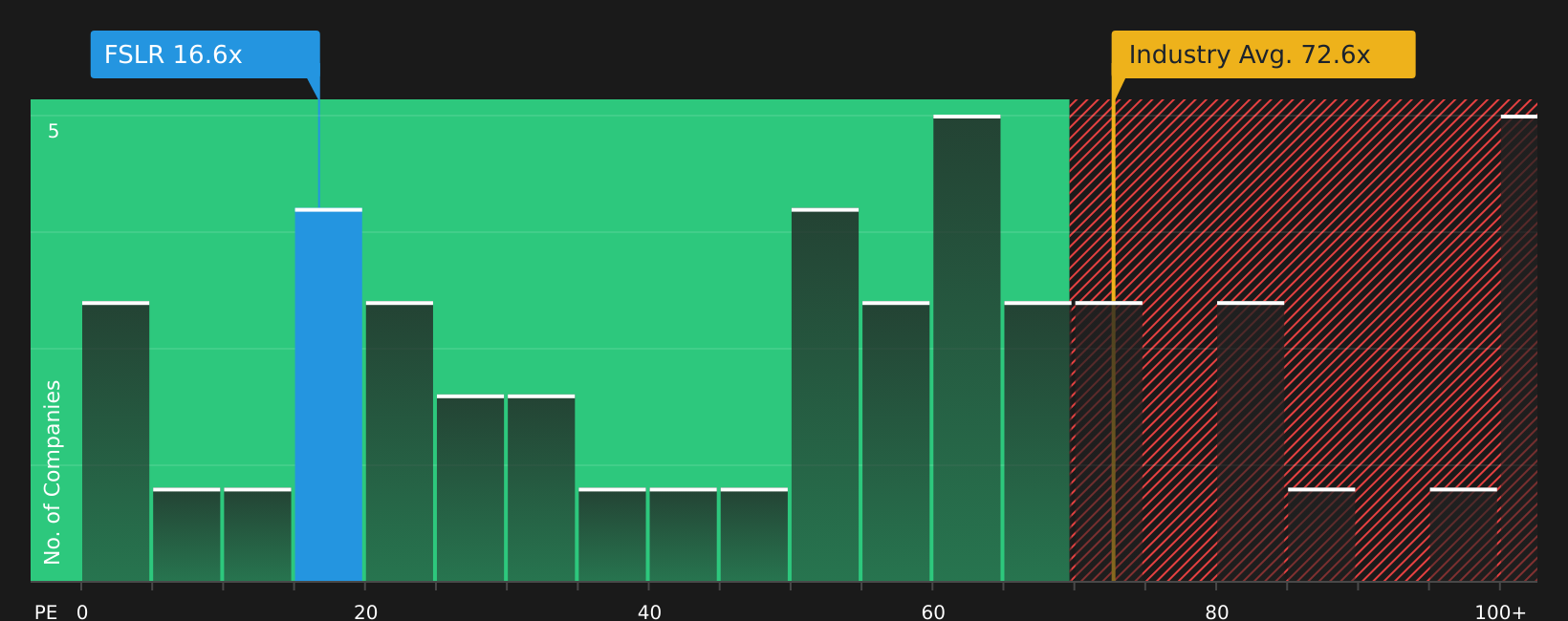

Approach 2: First Solar Price vs Earnings (P/E)

For a profitable company, the P/E ratio is a useful way to gauge how much you are paying for each dollar of earnings. It ties the share price directly to current profitability, which most investors watch closely.

What counts as a “normal” or “fair” P/E depends on how quickly earnings are expected to grow and how risky those earnings appear. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually calls for a lower one.

First Solar currently trades on a P/E of 19.80x. That sits below the broader Semiconductor industry average of 66.86x and well below the peer average of 114.07x. To go a step further, Simply Wall St calculates a “Fair Ratio” for First Solar of 40.37x. This proprietary metric aims to capture what P/E might be reasonable after considering factors such as the company’s earnings growth profile, profit margins, market cap, risk characteristics and its industry.

This Fair Ratio can be more informative than a simple comparison with peers or the industry because it adjusts for company specific traits rather than assuming all stocks deserve the same multiple. Comparing First Solar’s actual P/E of 19.80x with the Fair Ratio of 40.37x suggests the stock screens as undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your First Solar Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in. They give you a simple story that connects your view of First Solar’s business, its future revenues, earnings and margins, and your own fair value estimate, then compares that with the current price so you can judge whether it looks attractive or expensive.

On Simply Wall St’s Community page, Narratives let you see and build these stories yourself. They link a clear written thesis to a forecast model that updates automatically when new earnings, policy news or guidance is released, so your fair value view stays current rather than frozen in time.

For First Solar, one investor might build a cautious Narrative around tariff risks, modest revenue growth of 2.46% and a Fair Value near US$172.84. Another might focus on U.S. manufacturing expansion, assumed revenue growth of 18.80% and a Fair Value closer to US$313.00. By setting out these different Narratives side by side, you can quickly see which story and fair value aligns best with your own assumptions before deciding how the stock fits your plan.

For First Solar however we'll make it really easy for you with previews of two leading First Solar Narratives:

First up is a bullish view that treats today’s price as still leaving room for upside if policy support, technology progress and margins play out at the higher end of expectations.

Fair value in this optimistic Narrative: US$313.00 per share.

At the recent price of about US$306.79, this Narrative frames First Solar as trading about 2.0% below its implied fair value.

Revenue growth assumption: 18.80% a year.

- U.S. manufacturing build out, Section 45X credits and a non Chinese supply chain are expected to support premium margins and earnings compared with consensus analyst views.

- CuRe and perovskite technology, together with a large contracted backlog tied to AI, data centers and U.S. re shoring projects, are used to justify higher long term pricing power and strong utilization.

- The Narrative still flags heavy reliance on government policy, technology execution and a concentrated U.S. footprint as key risks that could pressure demand, pricing and earnings if conditions change.

On the other side is a more consensus oriented view where First Solar already sits closer to what many analysts see as fair value, with upside and downside more finely balanced.

Fair value in this more cautious Narrative: about US$281.65 per share.

Against the recent price of roughly US$306.79, this Narrative sees First Solar as trading about 8.9% above its implied fair value.

Revenue growth assumption: 12.54% a year.

- Expanded U.S. capacity and policy support are expected to keep demand and margins supported, with thin film technology and a sizable contracted backlog adding earnings visibility.

- Trade policy shifts, competition from low cost global producers and changing utility and energy company priorities are highlighted as potential headwinds for future revenue and profitability.

- Analyst targets around US$220.16 use earnings of US$3.2b by 2028 and a future P/E of 9.8x, but the wide US$100.00 to US$287.00 target range underlines how much uncertainty remains in the story.

If those two Narratives feel like useful starting points rather than final answers, the next step is to stress test their assumptions against your own views on policy risk, technology, demand and what you think is a reasonable multiple for the stock over time.

Do you think there's more to the story for First Solar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.