Is It Too Late To Consider Fortinet (FTNT) After Its Strong Recent Share Price Run?

Fortinet, Inc. FTNT | 0.00 |

- If you are wondering whether Fortinet's current share price reflects its potential, the starting point is understanding what the stock might be worth relative to its fundamentals.

- Fortinet's stock recently closed at US$129.70, with returns of 0.2% over 7 days, 51.3% over 30 days, 66.5% year to date, 27.1% over 1 year, 89.0% over 3 years, and 201.1% over 5 years.

- Recent news around Fortinet has focused on the company's position within the cybersecurity sector and how investors are reacting to that theme. This context helps explain why the share price performance over multiple time frames is drawing more attention from both existing and new shareholders.

- Fortinet currently has a valuation score of 1/6, which raises questions about how different valuation methods judge the stock and sets up a closer look at those methods, along with a broader way of thinking about value later in the article.

Fortinet scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

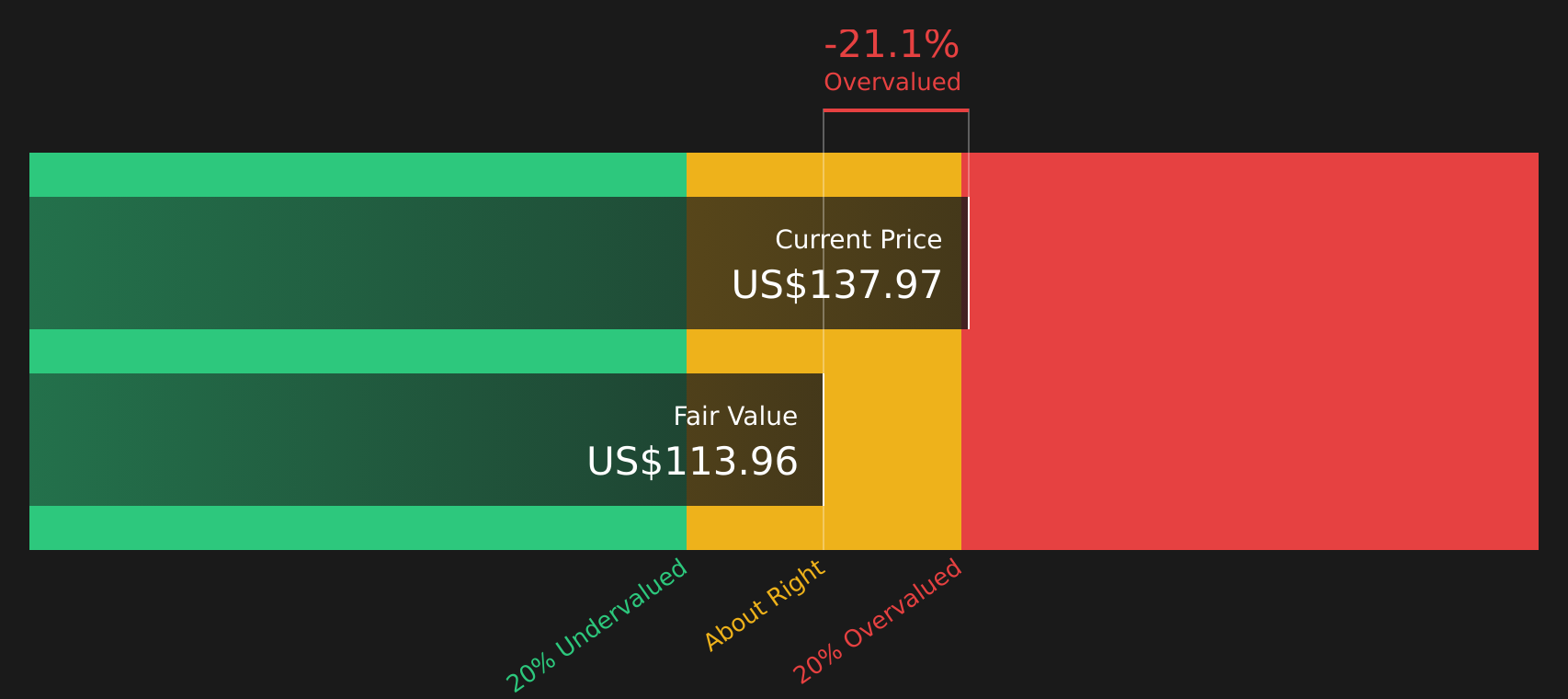

Approach 1: Fortinet Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash the business may generate in the future and discounting those amounts back to today.

For Fortinet, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s latest twelve month free cash flow is about US$2.43b. Analyst estimates and subsequent extrapolations point to projected free cash flow of US$4.55b in 2030, with intermediate yearly projections between those points provided by analysts and then extended by Simply Wall St’s model.

When these projected cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of about US$114.31 per share. Compared with the recent share price of US$129.70, this implies the stock is about 13.5% above the model’s estimate of fair value. On this measure, Fortinet screens as overvalued rather than cheap.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Fortinet may be overvalued by 13.5%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

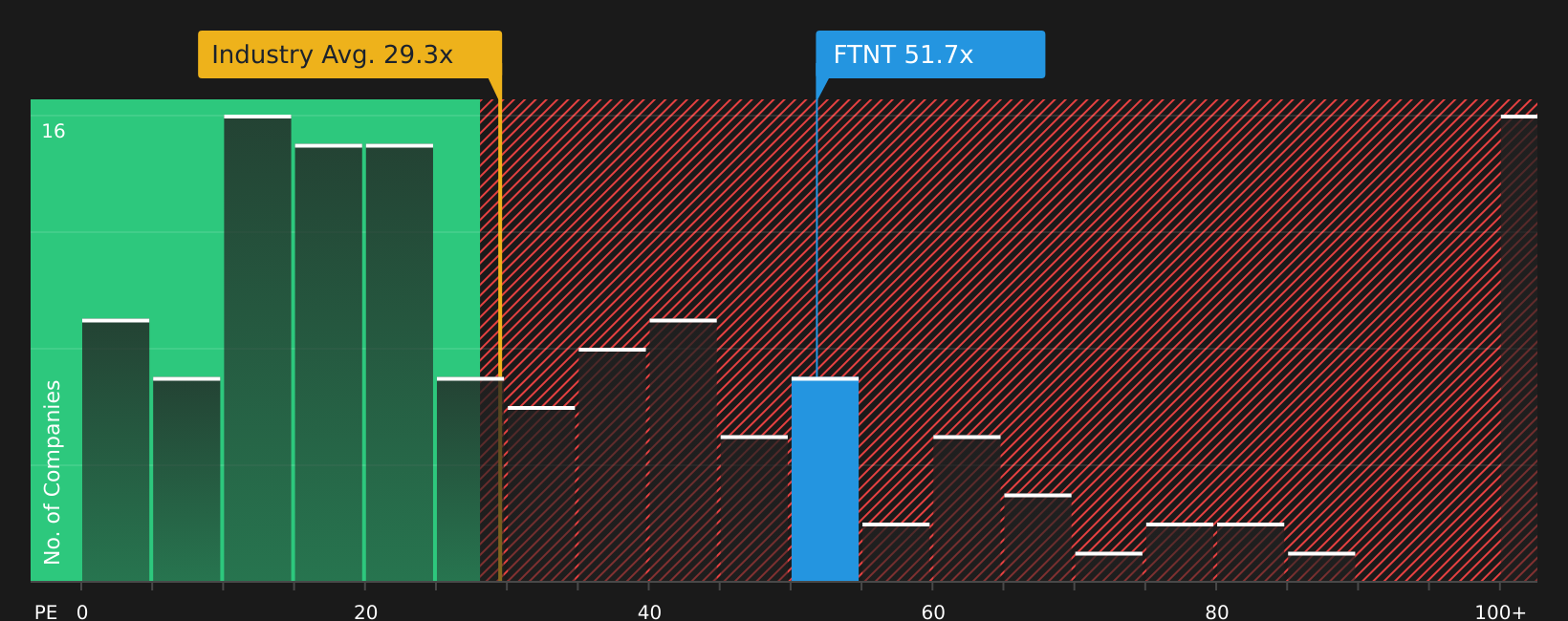

Approach 2: Fortinet Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for the stock to the earnings it is currently generating. It gives you a simple sense of how many years of current earnings are implied in today’s share price.

What counts as a “normal” P/E depends on how quickly earnings are expected to grow and how risky those earnings are. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually points to a lower one.

Fortinet currently trades on a P/E of 48.6x. That sits above the Software industry average P/E of 28.5x and below the peer average of 69.6x. Simply Wall St’s Fair Ratio for Fortinet is 33.4x. This Fair Ratio is a proprietary estimate of what P/E might be reasonable for the stock, given factors such as its earnings growth profile, profit margins, industry, market cap and risk traits.

Because the Fair Ratio is tailored to Fortinet’s own fundamentals, it can be more informative than a simple comparison with peers or the broad industry. Relative to this Fair Ratio of 33.4x, the current P/E of 48.6x suggests the stock is trading at a premium.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Fortinet Narrative

Earlier it was mentioned that there is an even better way to understand valuation. This is where Narratives come in, letting you attach a clear story about Fortinet to the numbers you care about, linking your view of its business, revenue, earnings and margins to a forecast and then to a Fair Value that you can compare with the current price to help you decide whether the stock looks appealing or stretched.

On Simply Wall St’s Community page, Narratives give you a simple tool to do exactly this, using the same framework that already powers millions of investor decisions. They update automatically as new data arrives, so when news, earnings or guidance are released, your Fair Value view adjusts in line with the latest information instead of sitting frozen in time.

For Fortinet, one investor might build a bullish Narrative that leans on high profitability metrics, a Fair Value around US$109.27 or US$110.39, and confidence in areas like AI security and SASE. Another might select a more cautious Narrative closer to US$77.37 that emphasizes hardware dependence, competition and regulatory risk. Comparing each of those Fair Values to the current share price can help you decide whether the opportunity fits your own expectations and risk tolerance.

Do you think there's more to the story for Fortinet? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.