Is It Too Late To Consider Garmin (GRMN) After Its Strong Multi Year Share Price Run?

Garmin Ltd. GRMN | 0.00 |

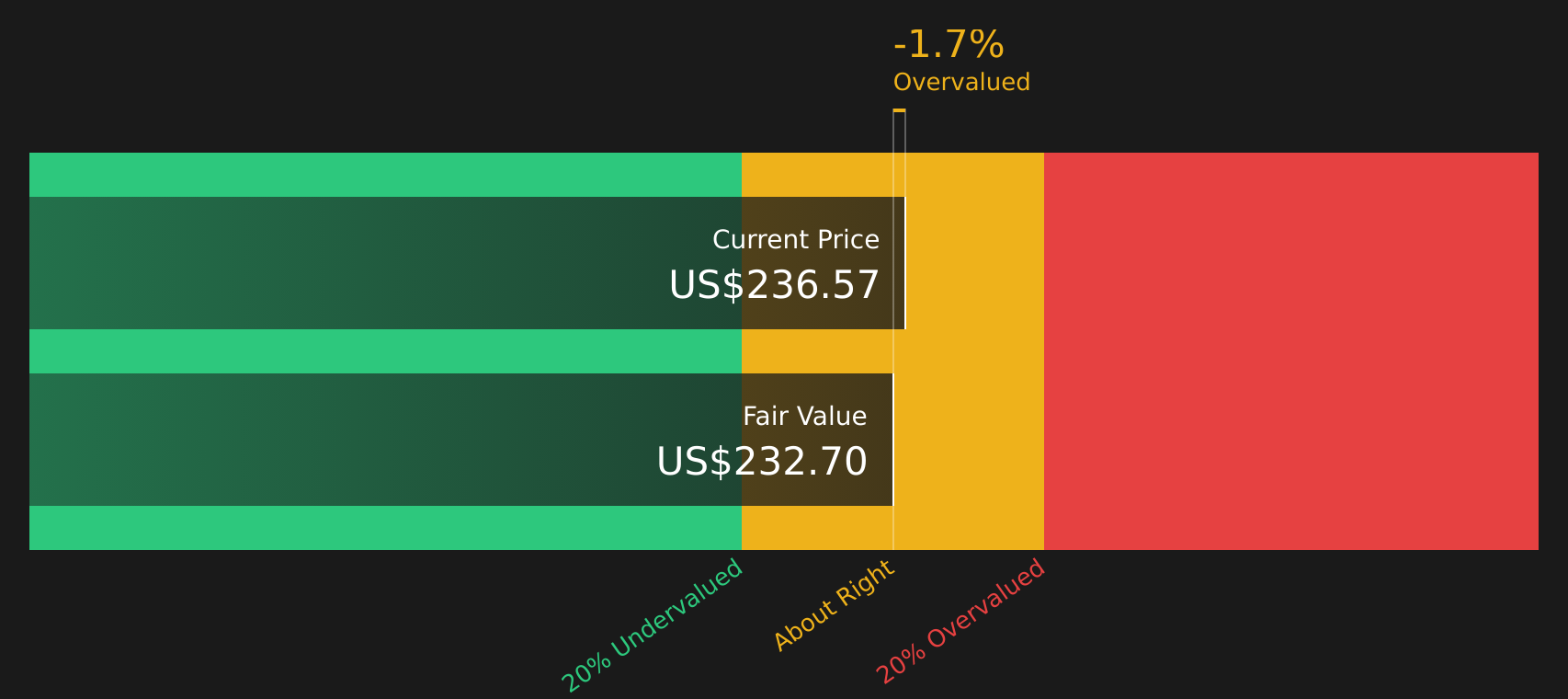

- If you are wondering whether Garmin at around US$236.57 is offering good value right now or if the strong run is already priced in, this breakdown will help you frame that question clearly.

- The stock is up 1.1% over the last 7 days, slightly down 2.6% over the last month, and has returns of 16.9% year to date, 15.9% over 1 year, 137.7% over 3 years, and 81.9% over 5 years, giving you a wide range of recent performance to consider.

- Recent coverage has focused on Garmin's position in consumer durables and its role in areas such as fitness wearables and navigation technology. This helps explain why investors are paying close attention to its share price. These stories give extra context for why the stock's shorter term moves look different from its longer term track record.

- Within that backdrop, Garmin currently has a valuation score of 1 out of 6. The next sections will walk through what different valuation approaches say about that score and outline a more complete way to think about value by the end of the article.

Garmin scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Garmin Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash Garmin could generate in the future and discounts them back to what that stream might be worth in $ today.

For Garmin, the latest twelve month Free Cash Flow is about $1.49b. Analysts and extrapolated estimates point to projected Free Cash Flow of $2.29b in 2030, with a ten year path that runs through discounted projections such as $1.47b in 2026 and around $1.56b in 2030. These projections are based on a 2 Stage Free Cash Flow to Equity model that uses analyst inputs for the earlier years and Simply Wall St extrapolations further out.

When those cash flows are discounted and summed, the model arrives at an estimated intrinsic value of about $232.50 per share, compared with the recent share price of around $236.57. That implies the stock is roughly 1.8% above the DCF estimate, which is a fairly small gap and within a margin where the shares can be seen as broadly in line with this cash flow model.

Result: ABOUT RIGHT

Garmin is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Garmin Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for each share to the earnings that share currently generates. This is often how many investors quickly compare stocks on value.

What counts as a “normal” P/E usually reflects how the market views a company’s growth prospects and risk. Higher expected growth and lower perceived risk can support a higher P/E, while slower growth or higher risk usually point to a lower multiple.

Garmin currently trades on a P/E of about 26.3x. That is higher than the Consumer Durables industry average P/E of about 12.3x, but below the peer group average of around 31.0x. Simply Wall St also provides a proprietary “Fair Ratio” of 23.9x, which is the P/E it would expect for Garmin given factors such as earnings growth, industry, profit margins, market cap and company specific risks.

This Fair Ratio can be more useful than a simple peer or industry comparison because it adjusts for Garmin’s own profile instead of assuming all Consumer Durables stocks deserve similar valuations.

Compared with this Fair Ratio of 23.9x, the current 26.3x P/E looks somewhat higher.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Garmin Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives bring this to life by letting you attach a clear story about Garmin to your numbers, linking your view of its future revenue, earnings and margins to a financial forecast and then to your own estimate of fair value.

On Simply Wall St’s Community page, Narratives are an accessible tool that helps you turn that story into a live model, compare your Fair Value with the current share price to decide whether the stock looks attractively or expensively priced on your assumptions, and then see those Fair Values refresh when new news, guidance or earnings are added to the platform.

For Garmin, one investor might align with a higher Fair Value around US$320.00 and focus on AI enabled services, subscription growth and premium wearables. Another might sit closer to US$220.00 and focus on competition, regulation and hardware pressure. Narratives let you pick which of those stories feels closer to your own view and keep it updated as fresh information arrives.

For Garmin however we will make it really easy for you with previews of two leading Garmin Narratives:

Fair value: US$262.43 per share

Gap to fair value: about 9.8% below this narrative fair value, based on the recent price of US$236.57

Assumed annual revenue growth: 9.35%

- Focuses on premium services like Garmin Connect+ and advanced wearables such as vívoactive 6 as key drivers for Fitness and higher margin subscription revenue.

- Highlights contributions from new aviation products, broader international exposure and Outdoor launches like the Instinct 3 series as important supports for future sales.

- Flags rising operating expenses, Marine and Outdoor challenges, trade policy shifts and currency swings as important watchpoints that could pressure margins.

Fair value: US$220.00 per share

Gap to fair value: about 7.5% above this narrative fair value, based on the recent price of US$236.57

Assumed annual revenue growth: 7.72%

- Emphasises pressure from smartphones, multipurpose devices and low cost rivals as potential headwinds for dedicated Garmin hardware and pricing power.

- Points to privacy rules, data regulation and reliance on cyclical aviation and marine sectors as sources of higher costs and revenue risk.

- Also recognises that health, outdoor, aviation and subscription services could still support margins and earnings quality, even if the stock already trades at a premium P/E.

These narratives give you two clear reference points, one that leans toward Garmin being closer to a higher fair value and one that frames the current price against a lower target, so you can decide which story fits better with your own expectations and risk tolerance.

Do you think there's more to the story for Garmin? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.