Is It Too Late To Consider Globus Medical (GMED) After Recent Share Price Strength?

Globus Medical Inc Class A GMED | 0.00 |

- If you are wondering whether Globus Medical's current share price reflects its true worth, you are not alone. This article focuses squarely on what the numbers say about value.

- The stock last closed at US$96.22, with returns of 6.7% over the past week, 3.5% over the past month, 10.2% year to date and 20.3% over the last year, plus 66.2% over three years and 56.4% over five years.

- Recent attention on Globus Medical has centered on its role in the healthcare sector and how investors are reacting to its position within medical technology. That interest helps frame the recent share price moves as the market reassesses both the potential and the risks around the business.

- On our checks, Globus Medical scores a 4 out of 6 valuation score. This points to several areas where the shares may be pricing in less than the modelled value. Next we will look at how different valuation approaches arrive at that view and why a more complete way of thinking about value can matter even more.

Approach 1: Globus Medical Discounted Cash Flow (DCF) Analysis

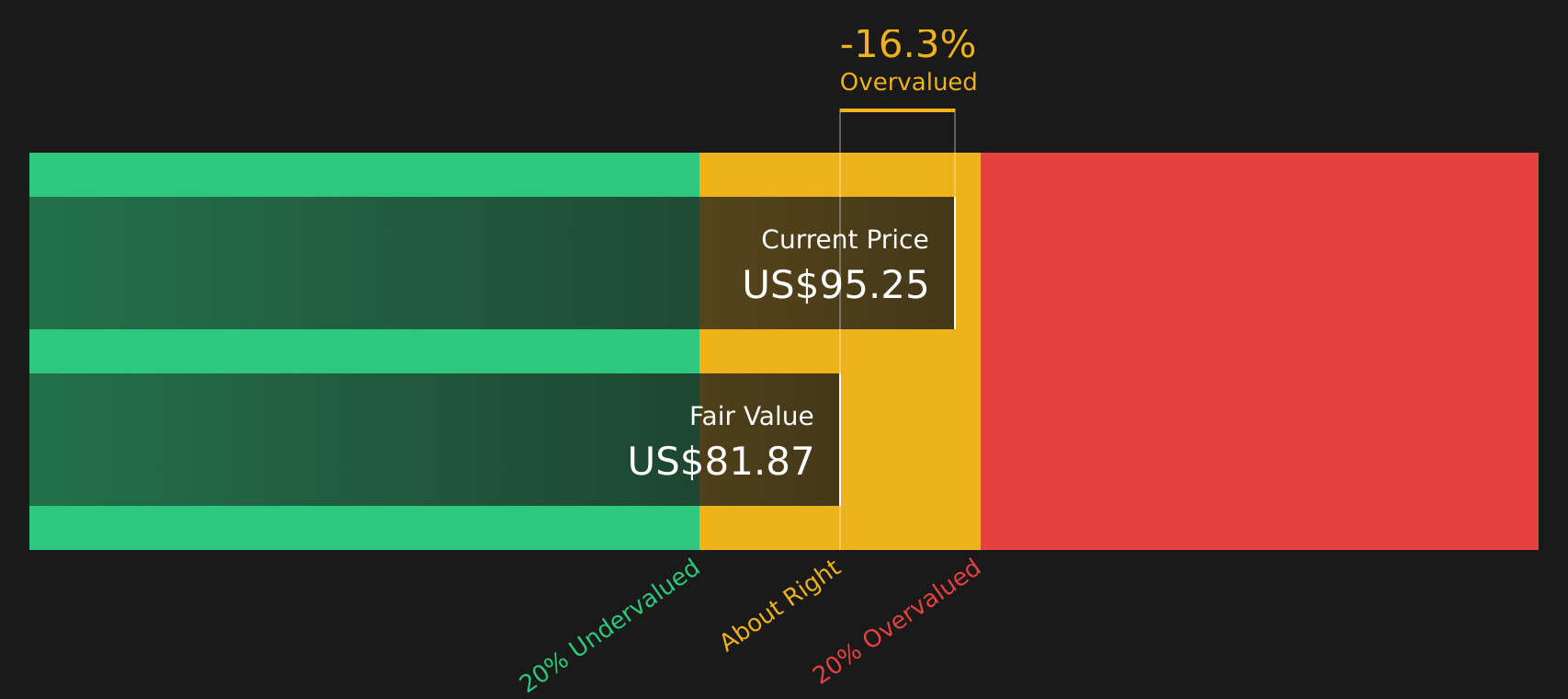

A Discounted Cash Flow model takes the cash Globus Medical is expected to generate in the future, then discounts those amounts back to today to estimate what the business might be worth right now.

For Globus Medical, the latest twelve month Free Cash Flow is about $603.6 million. Analysts provide forecasts out to 2027, with Free Cash Flow for that year modelled at $508.7 million. Beyond that, Simply Wall St extrapolates cash flows, with projected Free Cash Flow for 2035 of about $660.8 million based on the pattern in the forecast period.

Feeding these cash flows into a 2 Stage Free Cash Flow to Equity model results in an estimated intrinsic value of about $84.15 per share. Compared with the recent share price of $96.22, the model indicates the shares are about 14.3% above this estimate. On this DCF view, the stock appears to be overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Globus Medical may be overvalued by 14.3%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Globus Medical Price vs Earnings

For profitable companies, the P/E ratio is a useful way to connect what you pay for each share with the earnings the business is currently generating. It gives you a quick sense of how many dollars the market is willing to pay for each dollar of earnings.

What counts as a normal or fair P/E depends a lot on how quickly earnings are expected to grow and how risky those earnings are. Higher growth and lower perceived risk can support a higher multiple, while slower growth or higher risk usually points to a lower one.

Globus Medical currently trades on a P/E of 24.16x. That is below the Medical Equipment industry average P/E of 30.78x and also below the peer group average of 52.55x. Simply Wall St also calculates a proprietary Fair Ratio for Globus Medical of 22.17x. This Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it factors in company specific elements such as earnings growth, profit margins, risk profile, industry and market capitalization. Comparing the current P/E of 24.16x with the Fair Ratio of 22.17x suggests the shares are somewhat above this modelled level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Globus Medical Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply your own story about Globus Medical, linked directly to a set of numbers such as revenue, earnings, margins and a fair value that you can compare with today’s share price on Simply Wall St’s Community page. This is where millions of investors share their views, and where Narratives are kept up to date as new news or earnings arrive. You might, for example, align with investors who see Globus Medical’s fair value closer to US$118 based on stronger EPS potential, or with investors who anchor nearer to US$90 on more cautious assumptions. You can then decide for yourself whether the current US$96.22 price sits above or below the value that best fits your view of the company.

For Globus Medical, however, we will make it really easy for you with previews of two leading Globus Medical Narratives:

These give you ready-made sets of assumptions on growth, margins and fair value so you can decide which version of the future sounds closer to your own view, or adjust from there.

Fair value: US$118.00

Implied discount to this fair value vs the latest US$96.22 share price: 18.4%

Revenue growth assumption: 10.38% a year

- Assumes Globus Medical can lift margins through cost actions, automation and integration benefits, supporting higher earnings over time.

- Sees faster adoption of technologies like the Excelsius ecosystem and XR headset, with recurring software and disposables revenue playing a bigger role.

- Builds in a larger opportunity from aging demographics, international expansion and new indications from deals like Nevro, pointing to higher long term revenue and profit potential.

Fair value: US$90.00

Implied premium to this fair value vs the latest US$96.22 share price: 6.9%

Revenue growth assumption: 6.89% a year

- Assumes slower revenue growth as competition, pricing pressure and longer sales cycles weigh on both core products and enabling technologies.

- Highlights ongoing integration and execution risks around NuVasive and Nevro, along with higher operating costs, as reasons margins could stay constrained.

- Flags exposure to policy changes, reimbursement pressure and rival offerings as possible headwinds for surgical volumes and long run earnings.

If you want to see how other investors are stitching these moving parts together for Globus Medical, it is worth reading the full narratives behind each of these previews and then layering in your own assumptions about growth, margins and risk.

Do you think there's more to the story for Globus Medical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.