Is It Too Late To Consider Golar LNG (GLNG) After Multiyear Share Price Surge?

Golar LNG Limited GLNG | 55.29 | +3.06% |

- If you are wondering whether Golar LNG is genuinely good value at its current share price, this article will walk through what the numbers are really saying about the stock.

- The share price sits at US$40.58, with returns of 6.4% over the last 30 days, 6.9% year to date, and a 3 year return of 90.6% alongside a 5 year return that is very large. Over the last 7 days and 1 year, the share price has shown modest declines of 0.8% and 3.2% respectively.

- Recent news around Golar LNG has focused on its position in the liquefied natural gas shipping and infrastructure space, along with ongoing industry interest in how LNG assets are being deployed and financed. This background helps frame why the share price has moved unevenly across different time periods, as investors respond to changing views on LNG demand and project economics.

- Right now, Golar LNG scores 1 out of 6 on our valuation checks, as shown in its valuation score. Next, we will look at what different valuation approaches say about that result and then finish with a way to think about value that goes beyond the usual models.

Golar LNG scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

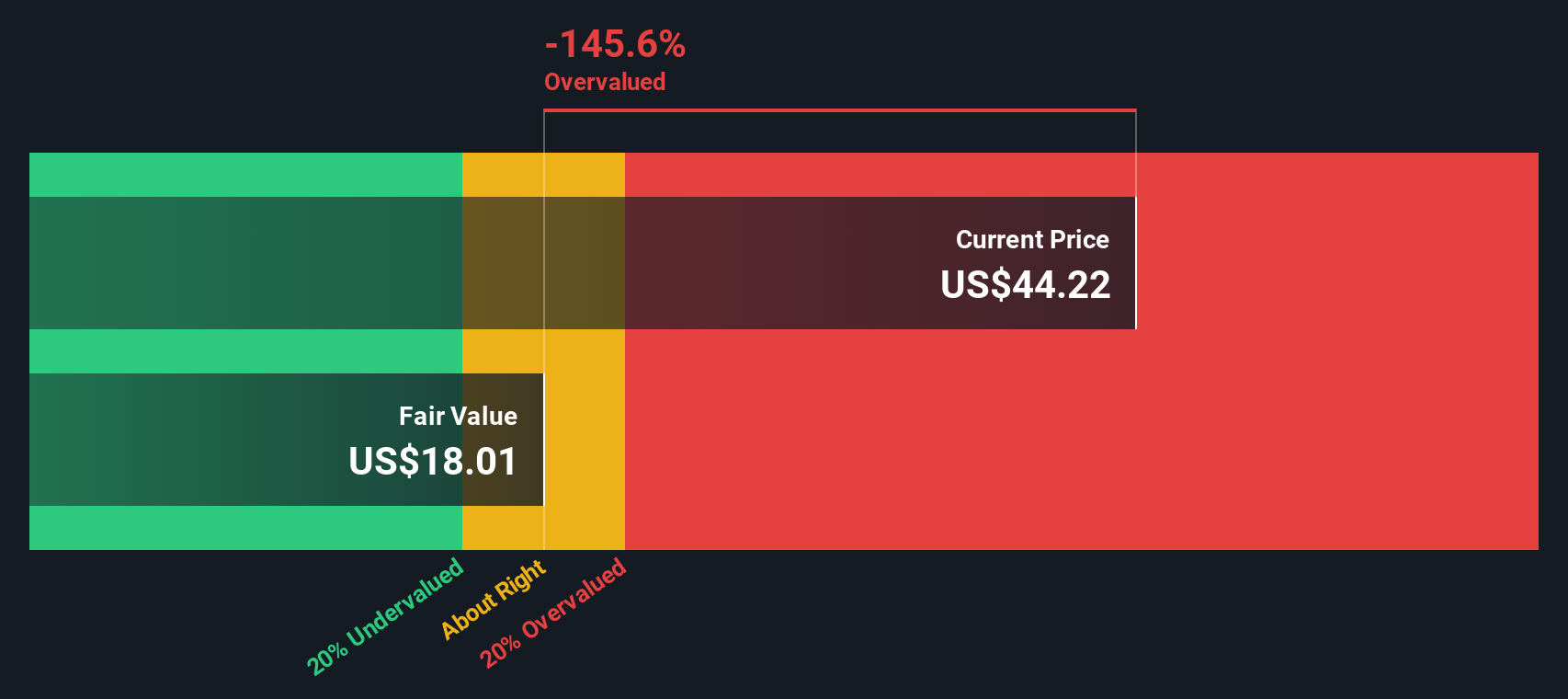

Approach 1: Golar LNG Dividend Discount Model (DDM) Analysis

The Dividend Discount Model looks at what a stock might be worth today by estimating all future dividends per share and discounting them back to the present. It is essentially asking what a fair price would be if your return came purely from dividends.

For Golar LNG, the model uses a current dividend per share of US$1, a return on equity of 4.24% and a payout ratio of 92.56%. That payout leaves only a small portion of earnings available to reinvest, so the implied long term dividend growth rate is low, around 0.32%. The growth input is calculated as the product of the retention ratio and return on equity, as shown in the model source.

Running these assumptions through the DDM gives an estimated intrinsic value of about US$15.06 per share. Compared to the current share price of US$40.58, this output suggests that, within this dividend-based framework, investors are paying a relatively high price for the current dividend stream.

Result: The shares appear expensive on this DDM basis

Our Dividend Discount Model (DDM) analysis suggests Golar LNG may be overvalued by 169.5%. Discover 865 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Golar LNG Price vs Earnings

For a profitable business, the P/E ratio is a useful shorthand because it links what you pay directly to the earnings the company is already generating. Higher expected growth and lower perceived risk tend to justify a higher P/E, while slower growth or higher risk usually point to a lower, more cautious multiple.

Golar LNG currently trades on a P/E of 69.47x. That sits well above the Oil and Gas industry average of 14.16x and also above the peer average of 31.71x. Simply Wall St’s Fair Ratio for Golar LNG is 19.74x, which is its estimate of a reasonable P/E given factors such as the company’s earnings profile, profit margins, industry, market cap and risk characteristics.

This Fair Ratio can be more useful than a simple peer or industry comparison, because it is tailored to the company rather than assuming all Oil and Gas names should trade on the same multiple. Comparing Golar LNG’s current 69.47x P/E with the 19.74x Fair Ratio suggests the shares are pricing in a much richer earnings multiple than this framework would indicate.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Golar LNG Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your own story about a company linked directly to the numbers you think are reasonable for its future revenue, earnings, margins and fair value.

On Simply Wall St’s Community page, used by millions of investors, a Narrative connects three things in one place: the business story you believe, the financial forecast that flows from that story, and the fair value you think follows from those forecasts.

That makes Narratives an accessible tool to help you decide if and when to buy or sell, because you can compare your Fair Value with today’s share price and see how your thesis stacks up against what the market is paying.

Narratives also update automatically when fresh information like news or earnings is added, so your view on Golar LNG is always grounded in the latest data. You can see, for example, one investor valuing the company at US$15 per share while another sees it closer to US$40 as they plug in different assumptions and stories about its LNG assets.

Do you think there's more to the story for Golar LNG? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.