Is It Too Late to Consider Google After a 37% Rally in 2025?

Alphabet Inc. Class A GOOGL | 287.56 | +5.14% |

If you have been eyeing Alphabet stock and asking yourself, “Is now the right time to jump in, or should I hold off?”, you are definitely not alone. Alphabet seems to always be at the center of attention when it comes to Big Tech investors, and for good reason. Recently, the stock notched steady gains, climbing 2.6% in the past week and posting an impressive 5.2% over the past month. Even more striking, it is up a whopping 37.2% year-to-date. Looking further back, the five-year return stands at an extraordinary 223.9%. Clearly, Alphabet has rewarded patient investors with growth, but does that mean it is still a good deal today?

Alphabet’s share price momentum is not just the outcome of hype. Recent product breakthroughs with its artificial intelligence offerings and moves to expand its cloud business have played a role, boosting market confidence about future growth. Investors also seem to be reassessing risk, with sentiment turning increasingly positive as the company sidesteps regulatory challenges and continues to dominate digital advertising.

So how does Alphabet look if we drill down into its valuation? According to a multi-check valuation score, Alphabet earns a 2 out of 6, meaning it is considered undervalued by two of the six assessment methods used. That is decent, but not screamingly cheap. Next, we are going to break down exactly which valuation methods are used and how they apply to Alphabet. Stick with us, because there is a smarter, more comprehensive way to size up the stock’s true worth that we will uncover at the end.

Alphabet scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

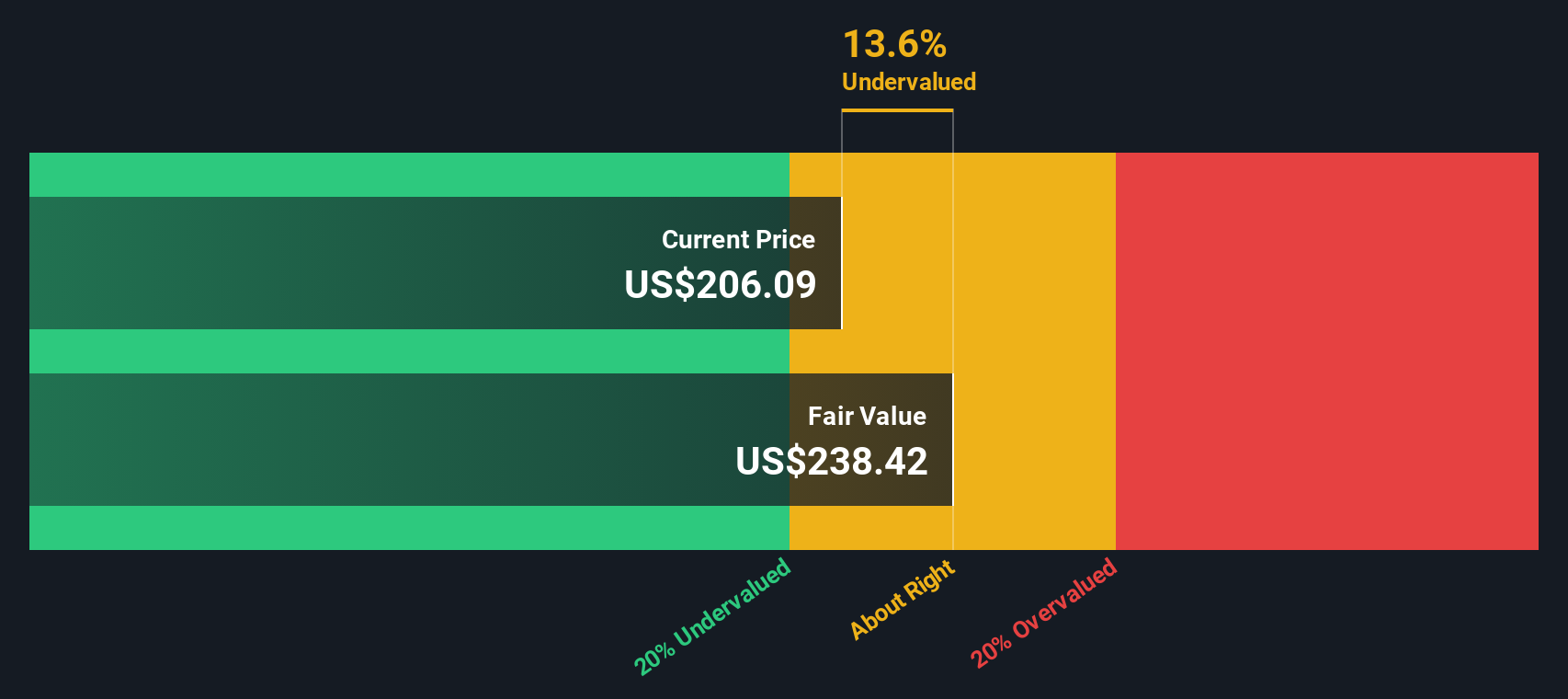

Approach 1: Alphabet Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and then discounting those cash flows back to today's dollars. This method aims to determine what Alphabet is fundamentally worth, based on cash flows it can generate for shareholders over time.

Alphabet's trailing twelve-month Free Cash Flow stands at $81.4 billion, a robust foundation for long-term valuation. Analysts have provided estimates up to 2029, predicting Free Cash Flow to reach $140.7 billion at that point. For the years beyond analyst forecasts, cash flow projections are extrapolated with conservative growth rates to simulate future performance.

After running these cash flows through the DCF model, the estimated fair value for Alphabet comes out to $244.50 per share. However, Alphabet currently trades at a price about 6.3% higher than this intrinsic value, suggesting the stock is a touch overvalued by this metric. While the share price is not excessively above its projected fair value, it does reflect a modest premium at this time.

Result: ABOUT RIGHT

Simply Wall St performs a valuation analysis on every stock in the world every day (check out Alphabet's valuation analysis). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes.

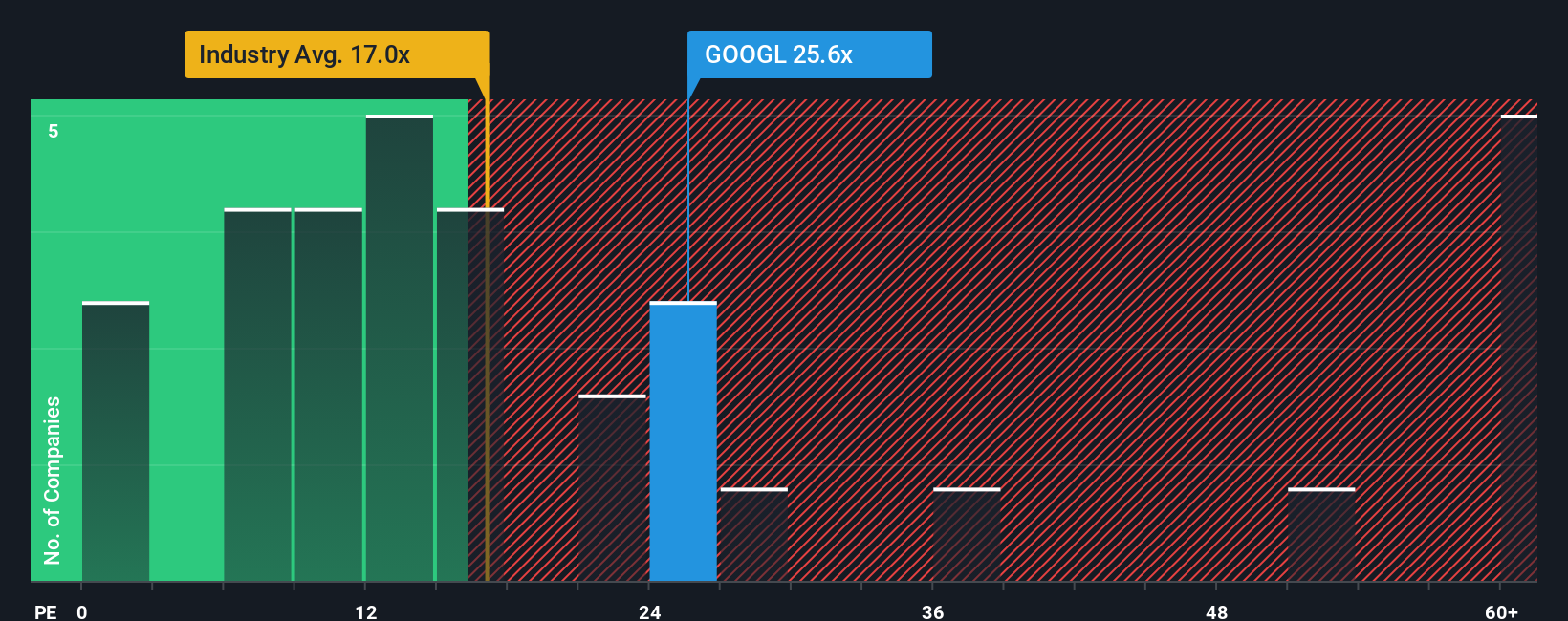

Approach 2: Alphabet Price vs Earnings

For established and highly profitable companies like Alphabet, the Price-to-Earnings (PE) ratio is a go-to valuation metric. The PE ratio compares a company’s share price to its earnings per share, giving investors a snapshot of how much they are paying for each dollar of earnings.

Interpreting a PE ratio, however, is more than just looking at the number in isolation. Companies with strong earnings growth prospects and lower risk profiles typically command higher PE multiples, as investors are willing to pay up for future potential and stability. On the other hand, lower growth or higher risk usually leads to a more modest PE ratio being seen as fair.

Alphabet’s current PE stands at 27.2x, which is higher than the broader Interactive Media and Services industry average of 15.5x, but well below the peer group average of 58.6x. To go a step further, Simply Wall St introduces the “Fair Ratio,” which is a tailored benchmark for what Alphabet’s PE should be today. This benchmark considers not just industry patterns but also company-specific factors like earnings growth, profit margins, market cap, and individual risks. Alphabet’s Fair Ratio is 41.8x. This approach is more informative than simply comparing to industry or peers because it normalizes for unique growth and risk factors that basic averages cannot capture.

Comparing Alphabet’s current PE of 27.2x to its Fair Ratio of 41.8x, the shares actually look below fair value using this lens. This suggests there could be room for upside if the market fully recognizes Alphabet’s strengths.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

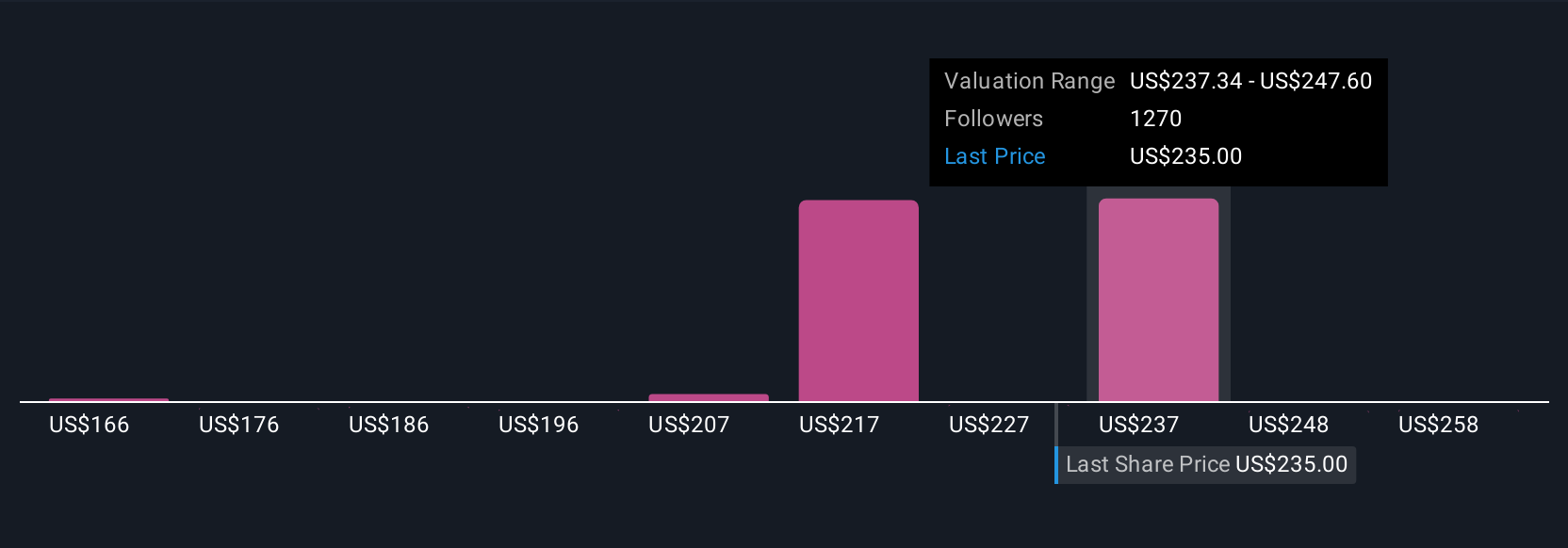

Upgrade Your Decision Making: Choose your Alphabet Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your unique investment story—a tool that lets you connect Alphabet's real-world business developments and your personal outlook with a clear financial forecast and fair value calculation.

Instead of simply taking the numbers at face value, Narratives allow you to build and share your own perspective on what drives Alphabet’s revenue, earnings, and margins in the years ahead. Available directly on Simply Wall St’s Community page, Narratives make it easy to map out your assumptions, quickly compare your fair value to Alphabet’s current price, and decide whether to buy, hold, or sell based on your evolving view.

A major advantage is that Narratives are dynamic. As new data or events like earnings reports, news, or product updates come in, your Narrative can be instantly updated so your fair value stays relevant and actionable.

For example, some investors believe Alphabet’s cloud and AI momentum will propel fair value as high as $268 per share. Others, concerned about regulatory risks or slower revenue growth, see fair value closer to $171. This demonstrates how Narratives help every investor weigh diverse scenarios and make more informed decisions.

Do you think there's more to the story for Alphabet? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.