Is It Too Late To Consider Hubbell (HUBB) After Its Strong Multi Year Rally?

Hubbell Incorporated HUBB | 0.00 |

Before deciding whether Hubbell fits your portfolio, it helps to ask a simple question: what are you really paying for at today’s price of US$544.71 per share?

Recent performance has caught attention, with the stock showing a 13.3% return over 30 days, 17.6% year to date, 53.4% over 1 year and 202.0% over 5 years, alongside a 0.8% decline over the last 7 days that may have some investors reassessing near term risks.

Recent news coverage has focused on Hubbell as part of wider discussions around power infrastructure, grid reliability and capital spending on electrical equipment, which helps explain why investors are paying close attention to the stock. These themes provide useful background when weighing whether the current share price is reasonable relative to the company’s role in these areas.

Simply Wall St’s valuation model gives Hubbell a valuation score of 2 out of 6. The next sections will break down what different valuation approaches suggest about that score, and finish by looking at a more complete way to think about value beyond any single metric.

Hubbell scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

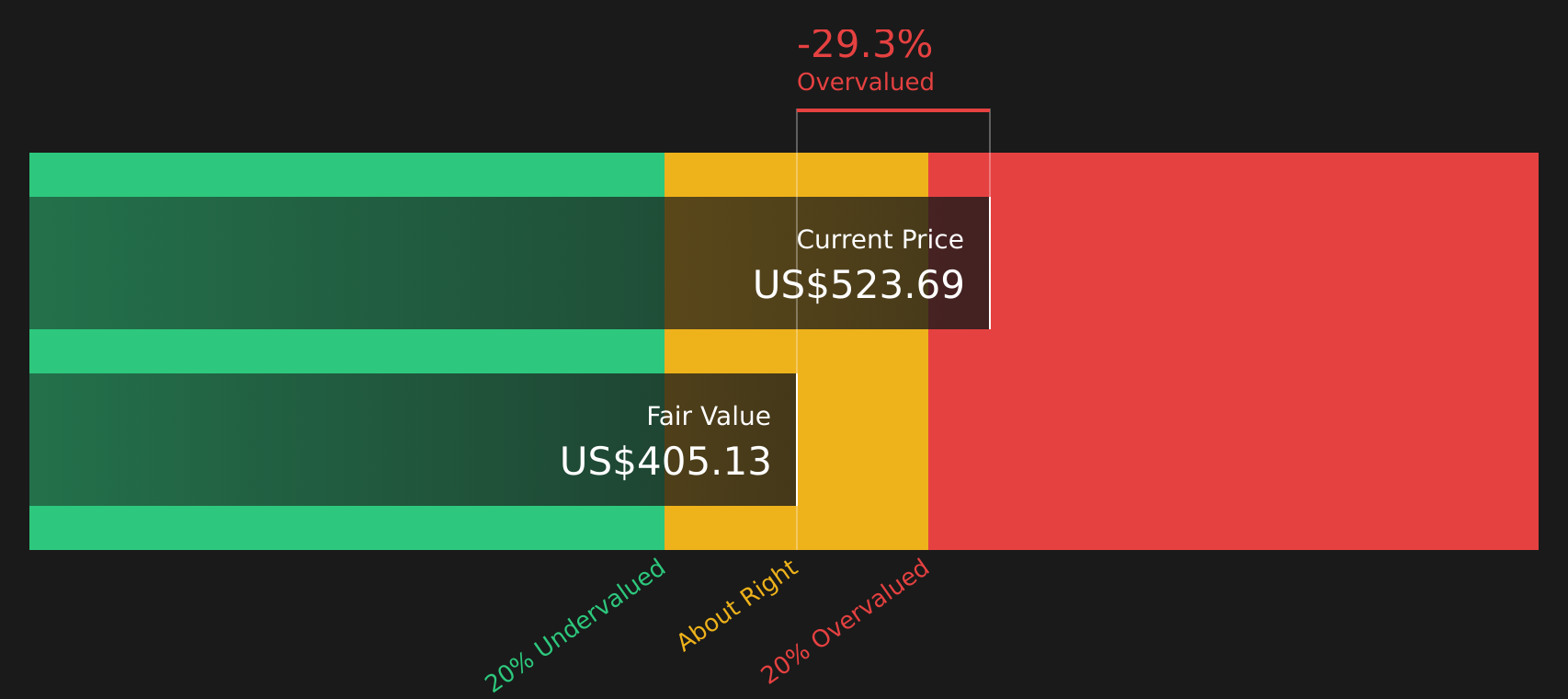

Approach 1: Hubbell Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company might be worth by projecting its future cash flows and discounting them back to today’s value, so you can compare that figure with the current share price.

For Hubbell, the model uses last twelve months free cash flow of about $855.9 million and applies a 2 Stage Free Cash Flow to Equity framework. Analysts provide explicit free cash flow estimates for several years, such as $1,024.1 million for 2026 and $1,194.0 million for 2028. Later years are extrapolated by Simply Wall St to build a 10 year path of cash flows in $.

When those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $368.90 per share, compared with the current share price of $544.71. That gap implies the shares are about 47.7% above this DCF based estimate.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hubbell may be overvalued by 47.7%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Hubbell Price vs Earnings

For a profitable company, the P/E ratio is a useful way to relate what you pay per share to the earnings that each share generates. Investors tend to accept higher P/E ratios when they expect stronger earnings growth and lower risk, and look for lower P/E ratios when growth expectations are more modest or risks feel higher.

Hubbell currently trades on a P/E of 32.6x. That sits below the peer group average of 45.8x, and a little below the Electrical industry average of 34.5x. On the surface, that might suggest the stock is priced more cautiously than some peers.

Simply Wall St’s Fair Ratio for Hubbell is 26.3x. This Fair Ratio reflects a custom view of what P/E might make sense given factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it blends these elements instead of relying only on broad peer or industry comparisons, it can provide a more tailored reference point. Compared with this 26.3x Fair Ratio, the current 32.6x P/E is higher, indicating the shares screen as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Hubbell Narrative

Earlier it was mentioned that there is an even better way to understand valuation. This is where Narratives come in, giving you a simple way to attach a clear story about Hubbell to numbers such as your fair value, revenue, earnings and margin assumptions, then link that story to a forward looking forecast and finally to a fair value you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are available as an accessible tool used by millions of investors. They help you see how different views on Hubbell’s future, such as analysts who see a Fair Value around US$535.77 or more bullish views near US$585.00, line up against the current share price so you can judge whether the gap between Fair Value and Price looks attractive or stretched for your own timeframe and risk tolerance.

Narratives also evolve over time, updating as new earnings, guidance or news arrive. For example, if you believe Hubbell’s grid modernization and data center exposure will support the higher US$585.00 view while another investor focuses more on tariff and cost inflation risks closer to US$479.00, you can each see how those different stories translate into updated forecasts and decide how comfortable you are with the assumptions behind them.

For Hubbell, however, we will make it really easy for you with previews of two leading Hubbell narratives:

One is a bullish view that leans into AI demand and 2026 guidance. The other is a more balanced take that sits closer to the current consensus. Looking at both side by side can help you decide which assumptions feel closer to your own.

Fair value in this bullish narrative: US$585.00 per share.

Gap to that fair value at the last close of US$544.71: about 6.9% below this narrative fair value.

Revenue growth assumption: 7.83% a year.

- Backs an integrated solutions model, cost control and the Systems Control acquisition as key supports for revenue and margin improvement, especially in transmission, substation, renewables and data centers.

- Assumes earnings reach about US$1.2b by around April 2029, with profit margins rising to about 16.2% and the P/E reaching roughly 33.5x, above the current US Electrical industry P/E used in the model.

- Flags risks around telecom weakness, utility destocking, the exit from residential lighting, competition in grid automation and tariff exposure, which could challenge the more optimistic case if they persist.

Fair value in this consensus style narrative: about US$535.77 per share.

Gap to that fair value at the last close of US$544.71: about 1.7% above this narrative fair value.

Revenue growth assumption: 6.42% a year.

- Sees solid organic growth and margin support from data center demand, grid modernization and acquisitions, with both Electrical Solutions and Utility Solutions contributing.

- Builds in earnings of about US$1.2b by around April 2029, margins of roughly 16.5% and a future P/E of about 31.7x, which is lower than the US Electrical industry P/E used in the model and close to the current share price.

- Highlights tariff and cost inflation, supply chain exposure to China, macro uncertainty and pricing execution as key factors that could pressure margins if not managed well.

Putting these side by side, you can see that both narratives use similar long term earnings figures but differ mainly in growth rates, margin paths and the P/E investors might be willing to pay. The question for you is which story, and which set of assumptions, feels more realistic for your timeframe and risk tolerance, and how that lines up with today’s US$544.71 share price.

To go deeper into the full assumptions, wording and risk sections behind each view, move from these previews to the complete community write ups. Then adjust the inputs until the narrative fits the way you see Hubbell.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Hubbell on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Hubbell? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.