Is It Too Late To Consider IMAX (IMAX) After Its Recent 30-Day Pullback?

IMAX Corporation IMAX | 0.00 |

- Wondering if IMAX at US$36.51 is still a sensible entry or if most of the value is already on the table? This article walks you through what the current price may be saying about the stock.

- The share price has returned 0.2% over the last 7 days and 1.4% year to date, but is 9.0% lower over the last 30 days. Over 1 year and 3 years, the stock has returned 46.9% and 90.3% respectively, while the 5 year return sits at 74.5%.

- Recent headlines around IMAX have focused on its position in premium cinema formats and the ongoing appeal of large format theatrical releases. These themes help frame how investors are reacting to the stock in the short term and how they might be thinking about the long run opportunity.

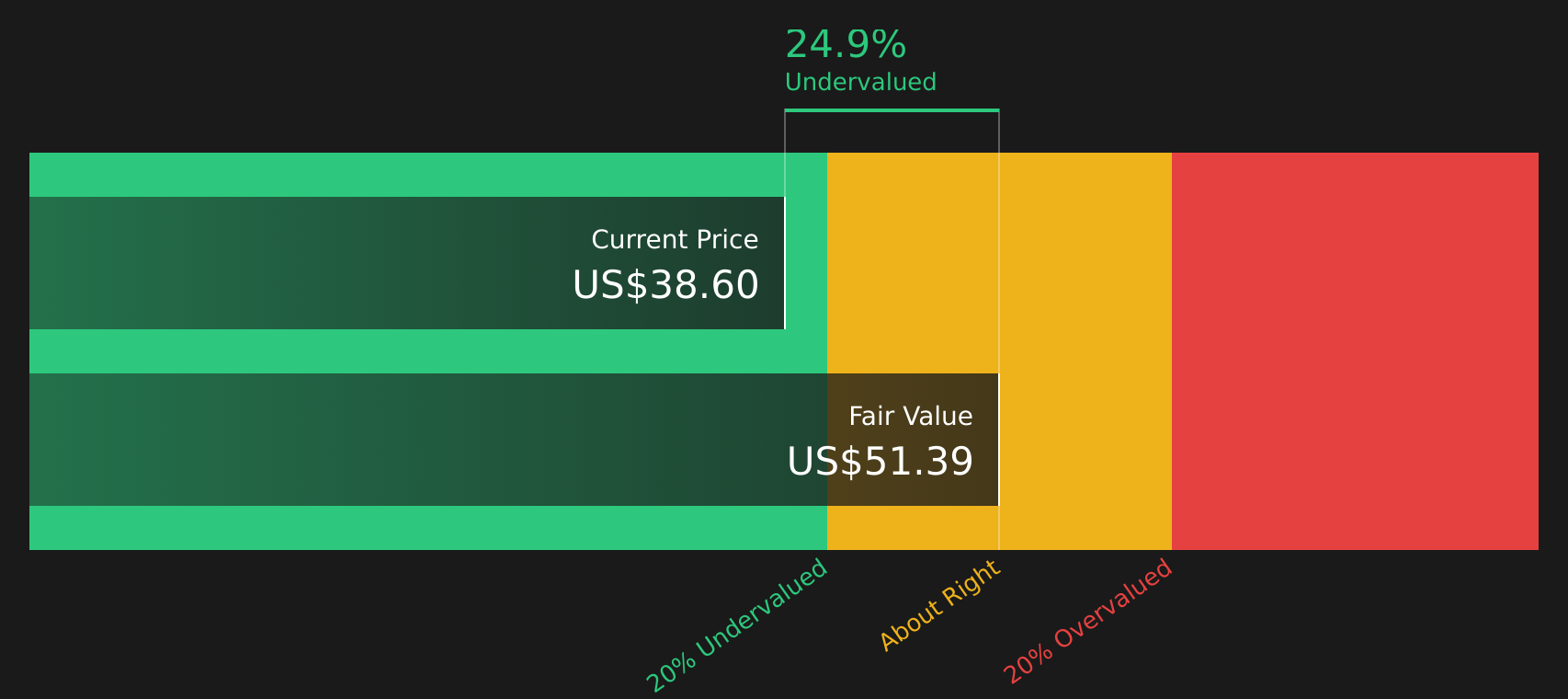

- On Simply Wall St, IMAX currently has a valuation score of 4/6, reflecting where it screens as undervalued on several checks. Next up is a closer look at the key valuation methods investors tend to rely on, followed by a different way of thinking about value that could be even more useful by the end of the article.

Approach 1: IMAX Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth today by projecting its future cash flows and then discounting those back to a present value. For IMAX, the model used is a 2 Stage Free Cash Flow to Equity approach. This looks at an initial period of specific forecasts, followed by a longer, more steady phase.

IMAX has last twelve month free cash flow of about $81.7 million. Analyst and extrapolated estimates used here project free cash flow reaching around $296.9 million in 2035. Simply Wall St applies discount rates to each year of projected cash flow, including interim figures such as $101.8 million in 2026 and $160.8 million in 2028, to reflect the time value of money and risk.

On this basis, the DCF model arrives at an estimated intrinsic value of $65.75 per share. Against the current share price of $36.51, this implies a 44.5% discount, which indicates that IMAX screens as undervalued on this method today.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests IMAX is undervalued by 44.5%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: IMAX Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it connects what you pay for each share with the earnings that business is currently generating. A higher or lower P/E often reflects what the market expects for future growth and how much risk investors see in those earnings.

If investors expect stronger growth and are comfortable with the risks, a higher P/E can be seen as normal, while slower growth or higher uncertainty usually calls for a lower, more conservative P/E. IMAX currently trades on a P/E of 54.6x, compared with an Entertainment industry average of about 29.0x and a peer average of 56.0x. This means the stock is broadly in line with its peers but above the wider industry.

Simply Wall St’s Fair Ratio for IMAX is 29.9x. This is a proprietary estimate of what the P/E could be given the company’s earnings profile, industry, profit margins, market cap and key risks. Because it integrates these factors, the Fair Ratio can offer a more tailored reference point than a simple comparison with peers or the broad industry. Set against the current P/E of 54.6x, the Fair Ratio indicates that IMAX screens as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 17 top founder-led companies.

Upgrade Your Decision Making: Choose your IMAX Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are worth introducing as a simple way for you to attach a story about IMAX to the numbers you are seeing, by linking your view of its future revenue, earnings and margins to a forecast, then to a Fair Value that can be compared with today’s price.

On Simply Wall St’s Community page, Narratives are available as an accessible tool used by millions of investors. They allow you to see how different assumptions translate into different Fair Values and help you judge whether IMAX looks expensive or cheap relative to your own view, rather than relying only on ratios like the current 54.6x P/E versus a 29.9x Fair Ratio.

For example, one IMAX Narrative built around a more cautious view ties together assumptions such as revenue growing around 7.2% a year, margins rising toward 19.4% and a Fair Value near US$41.09. A more optimistic Narrative uses higher growth expectations, different margin assumptions and a Fair Value closer to US$47.00. Both Narratives update automatically as new news or earnings data feeds into the platform, so you can see, in near real time, how changing inputs might influence whether you see IMAX as a buy, a hold or a sell.

Do you think there's more to the story for IMAX? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.