Is It Too Late To Consider Interactive Brokers Group (IBKR) After Its Strong 1 Year Rally?

Interactive Brokers Group, Inc. Class A IBKR | 0.00 |

- If you are wondering whether Interactive Brokers Group stock still offers value at current levels or if you might be late to the story, this article walks through what the current price could imply for investors.

- The stock last closed at US$86.97, with returns of 6.9% over the past week, 8.1% over the past month, 29.4% year to date and 66.5% over the past year, plus a very large 3 year return that is around 4x and an even larger 5 year figure.

- Recent coverage has focused on Interactive Brokers Group as a major online brokerage platform, with attention on its role in global trading, margin lending and interest income as higher rates change how clients use leverage and keep cash with the broker. Investors have also been watching the broader shift toward digital trading platforms, which can influence how the stock is priced relative to traditional brokers and financial institutions.

- On Simply Wall St's valuation checks, Interactive Brokers Group currently has a valuation score of 3/6. The rest of this article will walk through the key valuation methods behind that figure, then finish with a broader framework that can help you judge whether the stock suits your own view of value.

Approach 1: Interactive Brokers Group Excess Returns Analysis

The Excess Returns model asks a simple question: after paying shareholders an appropriate return for the risk they take, how much extra value can the company generate on its equity base, and for how long?

For Interactive Brokers Group, the starting point is a Book Value of US$12.54 per share and a Stable EPS estimate of US$7.79 per share, based on the median return on equity from the past 5 years. The Average Return on Equity is 19.85%, while the Cost of Equity is US$3.65 per share. That leaves an estimated Excess Return of US$4.14 per share, which the model treats as value created over and above the required return.

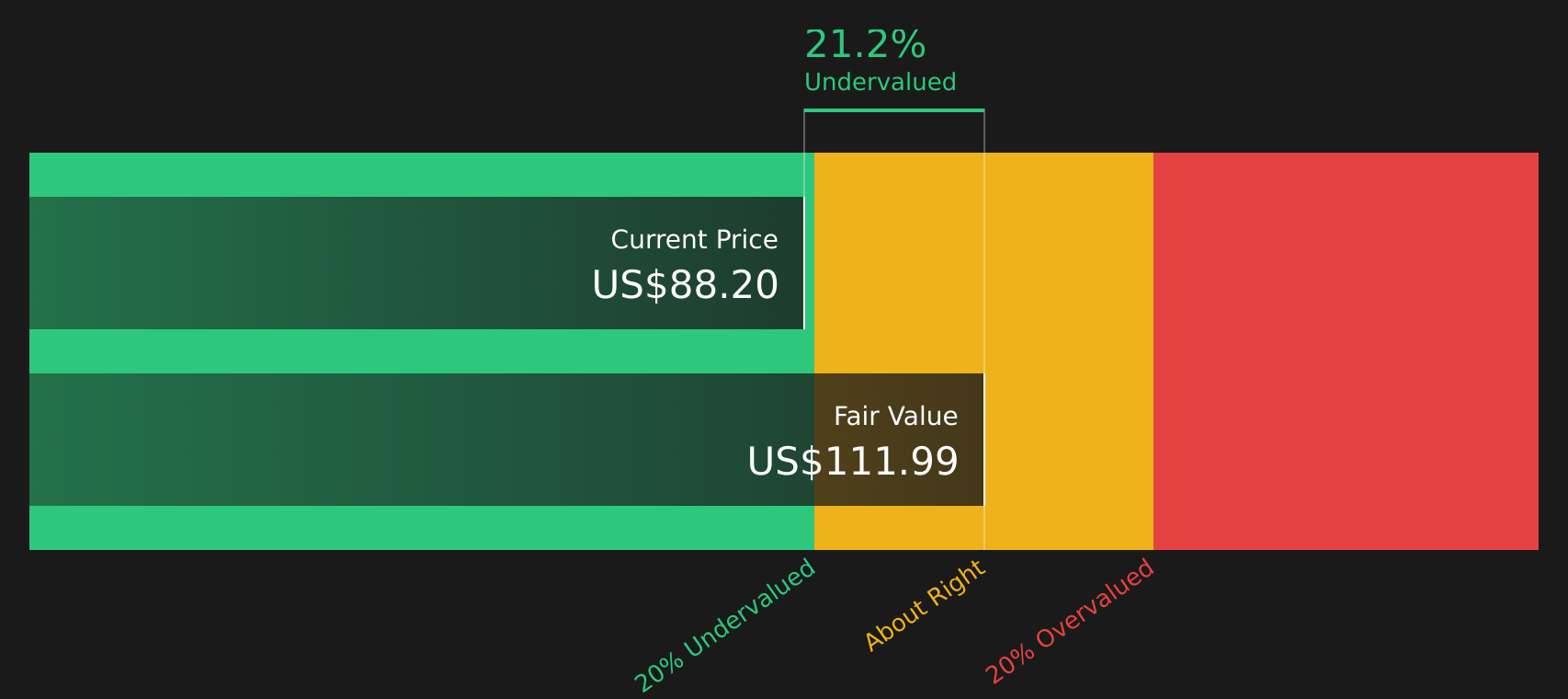

The Stable Book Value used in the model is US$39.22 per share, sourced from weighted future book value estimates from 2 analysts. Combining this with the projected excess returns produces an intrinsic value of about US$111.09 per share. Compared with the recent share price of US$86.97, the Excess Returns model suggests the stock is about 21.7% undervalued on this methodology.

Result: UNDERVALUED

Our Excess Returns analysis suggests Interactive Brokers Group is undervalued by 21.7%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Interactive Brokers Group Price vs Earnings

For a profitable company, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings, which is often more intuitive than focusing on sales or book value alone. A higher or lower P/E usually reflects what the market expects for future growth and how risky those earnings are perceived to be, so a "normal" or "fair" P/E should sit somewhere between high growth optimism and cautious risk pricing.

Interactive Brokers Group currently trades on a P/E of 37.33x. This compares with a Capital Markets industry average P/E of 39.53x and a peer average of 24.69x. Simply Wall St also calculates a proprietary "Fair Ratio" of 21.05x, which estimates the P/E that could be appropriate given factors such as the company’s earnings growth profile, profit margins, industry, market cap and risk characteristics.

This Fair Ratio approach goes further than a simple peer or industry comparison because it adjusts for the company’s own fundamentals instead of assuming that all brokers and capital markets stocks deserve similar multiples. Set against the current P/E of 37.33x, the Fair Ratio of 21.05x suggests Interactive Brokers Group may be overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Interactive Brokers Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives take that next step by letting you attach a clear story about Interactive Brokers Group, such as whether you lean toward a higher Fair Value like about US$86.00 or a lower figure around US$58.09, to the specific revenue, earnings, margin and P/E assumptions that sit behind those views.

On Simply Wall St's Community page, Narratives link this story to a full forecast and a Fair Value estimate, then line that up against the current price so you can quickly see whether your own view says the stock is trading above or below what you think it is worth.

Because Narratives update automatically when new information arrives, such as earnings results, changes in client balances or new analyst targets, your Fair Value view is kept current without needing to rebuild a model from scratch each time.

For Interactive Brokers Group, this means one investor might back a higher growth and higher P/E Narrative similar to the bullish Fair Value of US$85.00, while another might prefer a more cautious path closer to the bearish Fair Value of US$58.09, and both can see in real time how their chosen Narrative compares with the live share price.

Do you think there's more to the story for Interactive Brokers Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.