Is It Too Late To Consider Jabil (JBL) After Doubling In The Past Year?

Jabil Inc. JBL | 0.00 |

- If you are wondering whether Jabil's current share price offers value or is getting ahead of itself, the recent performance gives plenty to think about.

- The stock closed at US$355.43, with the price falling 4.5% over the last week but rising 16.4% over the past month, 47.9% year to date and 113.3% over the last year, while the three year and five year returns are very large.

- Recent news around Jabil has focused on providing ongoing coverage of the stock for investors, keeping attention on how the market is reacting to its current positioning and prospects. That context matters when you compare the strong multi year share price performance with how the stock now stacks up on valuation checks.

- Even with that backdrop, Jabil currently carries a valuation score of 1 out of 6. The next sections will walk through what traditional valuation methods say about the stock and then finish with a broader way to think about what that score really means.

Jabil scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

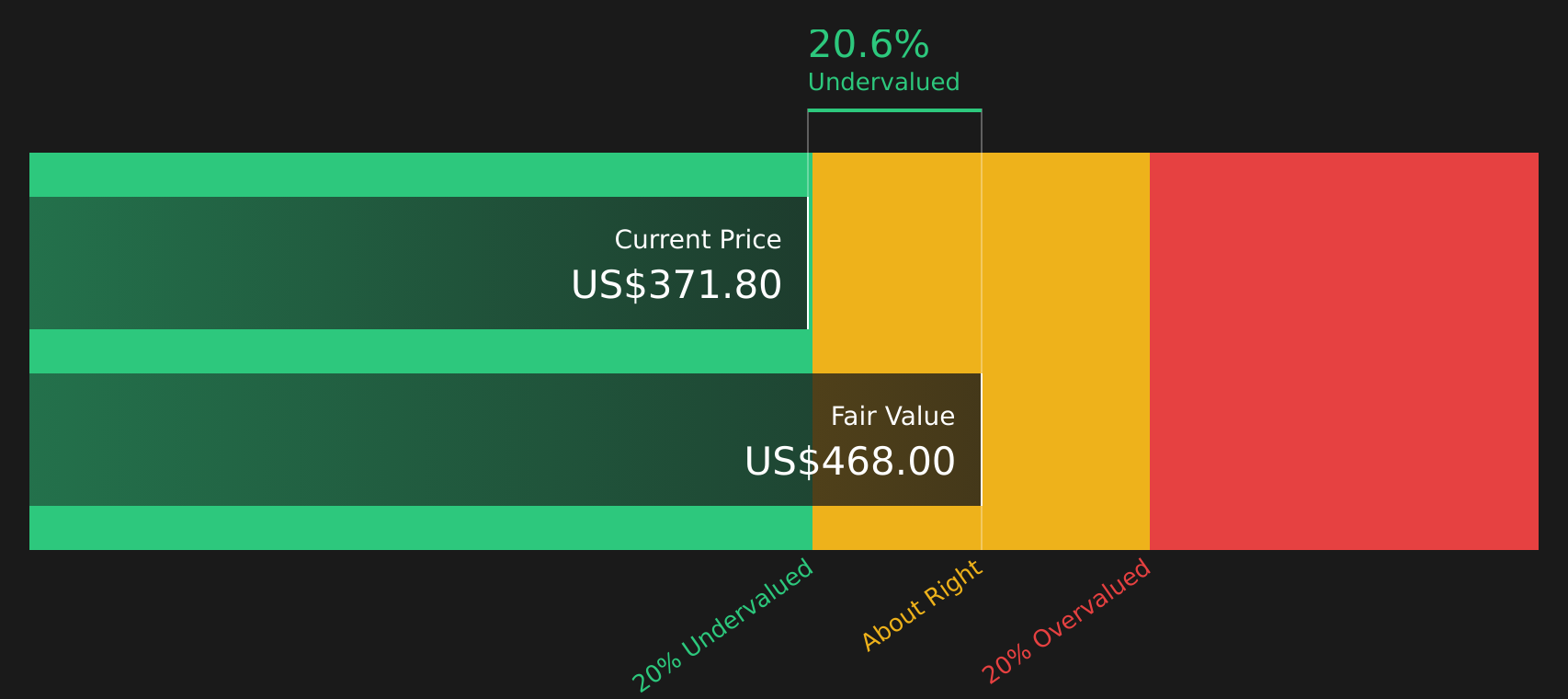

Approach 1: Jabil Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return. The aim is to convert a stream of future dollars into a single present value per share.

For Jabil, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow (FCF) is reported at $1,074.93m. Analyst inputs are provided for several years ahead, with projected FCF for 2028 at $2.03b, and further years extrapolated by Simply Wall St to build a ten year path of cash flows in dollars.

After discounting these projected cash flows, the DCF model arrives at an estimated intrinsic value of $353.86 per share, compared with the recent share price of $355.43. That implies the stock is about 0.4% above the DCF estimate, which is effectively a small gap that could be within normal modelling noise for this kind of analysis.

Result: ABOUT RIGHT

Jabil is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Jabil Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for each share to the earnings that company is currently generating. It gives you a quick sense of how many dollars investors are willing to spend today for one dollar of current earnings.

What counts as a “normal” P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth or more predictable earnings can justify a higher P/E, while slower or more uncertain earnings usually point to a lower multiple.

Jabil currently trades on a P/E of 46.35x. That sits above the Electronic industry average of 27.91x, though below the peer average of 57.98x. Simply Wall St’s Fair Ratio for Jabil is 38.47x, which is its own estimate of what a suitable P/E might be given factors such as Jabil’s earnings growth profile, industry, profit margin, market cap and company specific risks.

The Fair Ratio is more tailored than a simple peer or industry comparison because it attempts to adjust for those company specific factors rather than assuming all stocks in a sector deserve similar multiples. Compared with this Fair Ratio, Jabil’s actual P/E of 46.35x is higher, which points to the stock looking overvalued on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Jabil Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are a simple way for you to write the story behind your numbers by linking what you believe about Jabil’s business to a forecast for revenue, earnings and margins, then to your own fair value that you can compare with the current share price to decide whether the stock looks attractive or expensive right now.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. They update automatically when new information such as earnings releases or news about AI data center agreements, new markets like India or pharmaceutical acquisitions, or segment pressures and tariff risks is added to the platform, so your fair value stays aligned with the latest data without extra work from you.

For Jabil, one investor might build a Narrative that leans toward the higher analyst price target of US$354.00 by focusing on AI related demand, India expansion and the pharmaceutical opportunity. Another might land closer to the lower target of US$273.00 by focusing more on segment weakness, inventory issues and tariff uncertainty, and Narratives help you see clearly which story you are closest to and whether that justifies a different view from the current market price.

Do you think there's more to the story for Jabil? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.