Is It Too Late To Consider Marathon Petroleum (MPC) After Its 60% One Year Surge?

Marathon Petroleum Corporation MPC | 0.00 |

- If you are wondering whether Marathon Petroleum at US$251.33 is still offering value or starting to look stretched, the headline numbers only tell part of the story.

- The stock has posted returns of 1.2% over the past 7 days, 8.1% over 30 days, 52.2% year to date and 60.2% over the last year, which naturally raises questions about how much of this is already reflected in the current price.

- Recent attention on large integrated refiners and fuels infrastructure companies has kept Marathon Petroleum in focus, particularly as investors compare long term energy demand with capital allocation plans across the sector. Broader debates around future refining capacity and the mix between traditional fuels and lower carbon projects also help frame how the market is thinking about the stock today.

- Marathon Petroleum currently has a value score of 3/6, and the rest of this article will break down what that means across different valuation approaches, with a more holistic way to think about valuation kept for the end.

Approach 1: Marathon Petroleum Discounted Cash Flow (DCF) Analysis

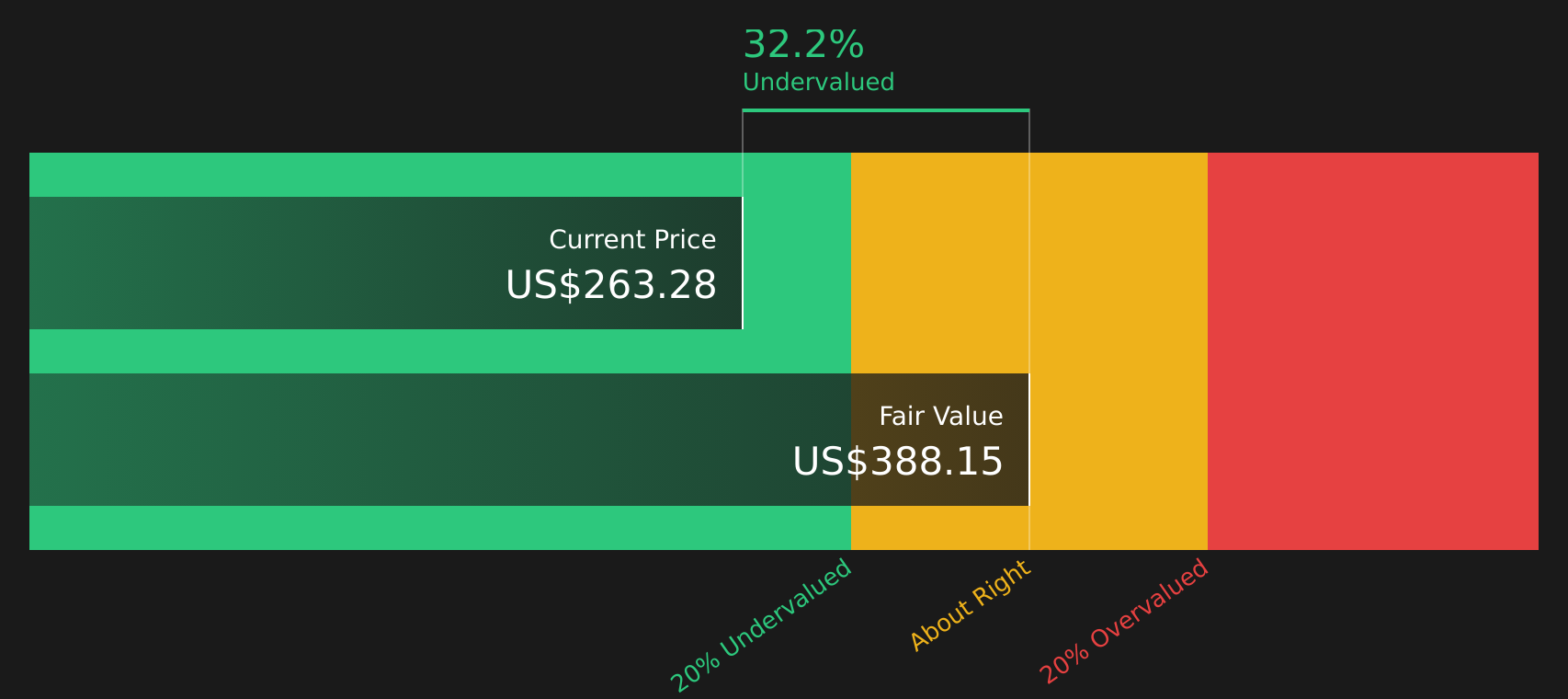

A Discounted Cash Flow model projects the cash Marathon Petroleum might generate in the future and then discounts those cash flows back to today to estimate what the entire business could be worth right now.

On this approach, Marathon Petroleum is modeled using a 2 Stage Free Cash Flow to Equity method. The company’s latest twelve month free cash flow is about $6.7b. Analyst and extrapolated projections suggest annual free cash flow in the $5b to $8.6b range over the coming decade, with an estimated $5.9b in 2030. Simply Wall St discounts those future cash flows back to today using its own assumptions to arrive at an estimated intrinsic value per share of about $418.02.

Compared with the current share price of US$251.33, this implies the stock is trading at a discount of roughly 39.9% to that intrinsic value. On this DCF view alone, Marathon Petroleum appears to be trading below that estimated intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marathon Petroleum is undervalued by 39.9%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Marathon Petroleum Price vs Earnings

For profitable companies, the P/E ratio is a useful cross check because it links what you pay for the stock directly to the earnings it is currently generating. Investors often look for a P/E that lines up with their view of the company’s growth potential and risk profile, with higher growth or perceived resilience sometimes supporting a higher P/E, and higher risk or weaker growth pointing to a lower P/E as more typical.

Marathon Petroleum currently trades on a P/E of 15.9x. That sits above the Oil and Gas industry average of 13.6x and is close to the peer group average of 15.4x. Simply Wall St also calculates a proprietary “Fair Ratio” of 22.8x for Marathon Petroleum, which is an estimate of what the P/E might be given factors such as earnings growth, profit margins, market cap, risks and the characteristics of the industry.

Because the Fair Ratio incorporates company specific fundamentals rather than relying only on broad industry or peer comparisons, it can give a more tailored reference point. Comparing Marathon Petroleum’s current P/E of 15.9x with the Fair Ratio of 22.8x suggests the stock is trading below that Fair Ratio estimate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Marathon Petroleum Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story about Marathon Petroleum to the numbers by connecting your view of future revenue, earnings and margins to a forecast and then to a Fair Value that you can compare directly with today’s market price.

Within the Community page, Narratives are set up as easy to use templates that reflect different viewpoints. For example, there is a more optimistic case that assumes earnings could reach about US$8.6b by 2029 with a Fair Value aligned to a higher price target of around US$318.81, and a more cautious case that assumes earnings nearer US$3.4b and a Fair Value closer to US$163.00.

By selecting the Marathon Petroleum Narrative that best matches your expectations and risk comfort, you can quickly see whether that Fair Value sits above or below the current share price. This can give you a structured way to think about whether to add, trim or simply watch, while the Narrative itself automatically refreshes as new earnings, news or analyst updates come through.

For Marathon Petroleum, we’ll make it really easy for you with previews of two leading Marathon Petroleum Narratives:

One reflects a view that the stock is broadly in line with analyst targets, and the other leans toward a more cautious fair value. Lining them up side by side helps you see which set of assumptions is closer to your own.

Fair value in this Narrative: US$256.83 per share.

Gap to that fair value versus the last close of US$251.33: about 2.1% below the Narrative fair value.

Revenue trend used in the Narrative: revenue is expected to decline about 4.8%.

- Analysts in this scenario expect earnings of about US$5.8b by 2029, with profit margins rising from 3.4% to 4.3%.

- The setup assumes the stock would trade on a P/E of 13.6x in 2029, with ongoing share count reduction of just under 5% per year for the next three years.

- This view treats Marathon Petroleum as broadly fairly priced around the consensus target, with the DCF fair value and analyst price target both close to the current share price.

Fair value in this Narrative: US$163.00 per share.

Gap to that fair value versus the last close of US$251.33: about 54.1% above the Narrative fair value.

Revenue trend used in the Narrative: revenue is expected to decline about 2.2% per year.

- This scenario assumes revenue falling and margins easing from 3.0% to 2.7%, with earnings in 2029 at about US$3.4b and a P/E of 15.4x on those earnings.

- It still factors in ongoing buybacks, with the share count expected to decline just over 4% per year, but sees less support from refining and Midstream returns.

- On this view, the fair value of US$163.00 sits well below the current price, so the downside case focuses on weaker refining conditions and softer returns from planned capital projects.

Neither Narrative is “right” on its own. The useful step is to decide which set of revenue, margin and valuation assumptions you find more reasonable given how you see fuel demand, project execution and capital returns playing out, then track how Marathon Petroleum’s actual results line up over time.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Marathon Petroleum on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Marathon Petroleum? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.