Is It Too Late To Consider Marex Group (MRX) After Its Strong Year To Date Rally?

Marex Group plc MRX | 0.00 |

- If you are wondering whether Marex Group's current share price reflects its true worth, this article walks through the key numbers that matter for value focused investors.

- The stock recently closed at US$53.12, with returns of 7.4% over 7 days, 23.6% over 30 days, 40.0% year to date, and 20.8% over 1 year. These figures put recent price moves front and center in any valuation discussion.

- Recent coverage has focused on Marex Group as a listed player in the capital markets space and on how its shares have traded since listing. This gives investors more visibility into trading volumes and price behavior. This context helps explain why some investors are now reassessing the balance between potential growth and risk in the current share price.

- Right now, Marex Group has a valuation score of 2 out of 6. The next sections will compare what different valuation methods say about that score and then finish with a broader way to think about what "fair value" really means for this stock.

Marex Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

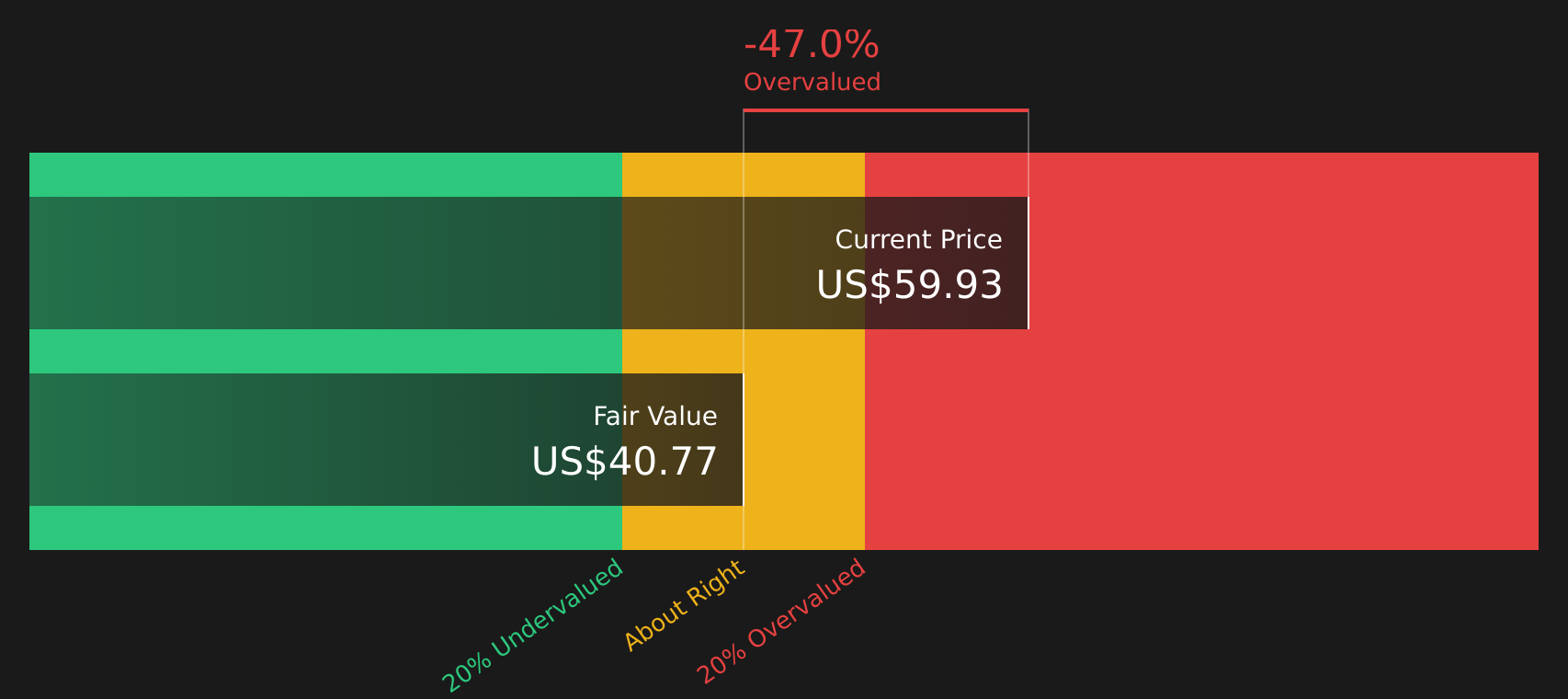

Approach 1: Marex Group Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to generate above the return required by its shareholders, then converts that into a per share value. It focuses on whether the business can consistently earn more on its equity base than the cost of that equity.

For Marex Group, book value is estimated at $16.26 per share, with a stable book value of $23.94 per share based on weighted future estimates from 2 analysts. Using the median return on equity from the past 5 years, the model derives a stable EPS of $4.16 per share. Against a cost of equity of $3.21 per share, this implies an excess return of $0.95 per share. The average return on equity used in this framework is 17.39%.

Putting these inputs together, the Excess Returns model arrives at an intrinsic value of about $33.39 per share. Compared with the recent share price of $53.12, this implies Marex Group is 59.1% overvalued on this measure.

Result: OVERVALUED

Our Excess Returns analysis suggests Marex Group may be overvalued by 59.1%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Marex Group Price vs Earnings

For a profitable company like Marex Group, the P/E ratio is a straightforward way to relate what you pay per share to the earnings that support that price. It is popular because it ties directly to the bottom line that ultimately matters to shareholders, earnings per share.

What counts as a “normal” P/E depends on how the market views growth potential and risk. Higher expected earnings growth or lower perceived risk can justify paying a higher multiple, while slower growth or higher risk usually goes with a lower one.

Marex Group currently trades on a P/E of 13.0x. That sits close to the peer average of 12.1x, and well below the broader Capital Markets industry average of 42.1x. Simply Wall St’s Fair Ratio for Marex Group is 14.2x. This Fair Ratio is a proprietary estimate of what the P/E could reasonably be, given factors such as earnings growth profile, industry, profit margins, market cap and specific risk characteristics.

Compared with simple peer or industry comparisons, the Fair Ratio is designed to be more tailored, because it adjusts for growth, risk, profitability and company size rather than relying on blunt averages. With the current P/E at 13.0x versus a Fair Ratio of 14.2x, Marex Group screens as mildly undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Marex Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a clear story for Marex Group that connects your view of its business to specific revenue, earnings and margin estimates. These are then turned into a Fair Value, which you can compare with the current share price to decide whether the stock looks appealing or expensive. Each Narrative sits inside the Community page, updates automatically when new news or earnings arrive, and captures very different opinions. For example, one investor sees Marex Group as worth around US$66.00 based on assumptions about future earnings and an 11.6x future P/E, while another sees closer to US$36.99 using a 6.6x future P/E and softer revenue assumptions.

For Marex Group however we will make it really easy for you with previews of two leading Marex Group Narratives:

Fair value in this bullish narrative: US$66.00 per share.

At the recent price of US$53.12, this view implies Marex Group is about 19.5% below that fair value.

Revenue growth used in this narrative: 61.69%.

- Analysts in this camp see Marex Group's automation, platform scale and client retention supporting higher margins and durable earnings quality.

- They expect earnings to grow to US$523.9m by about April 2029, with profit margins rising to 17.9% and a future P/E of 11.6x applied to those earnings.

- This view leans on continued benefits from capital raising, international diversification and expansion in derivatives and digital financial products.

Fair value in this bearish narrative: US$36.99 per share.

At the recent price of US$53.12, this view implies Marex Group is about 43.6% above that fair value.

Revenue growth used in this narrative: 1.74% decline.

- Analysts in this camp focus on the risk that lower market volatility, higher compliance costs and automation could weigh on Marex Group's brokerage and clearing income.

- They model earnings reaching US$513.4m by about April 2029, with margins rising to 18.9%, but apply a lower future P/E of 6.6x to reflect concerns about the durability of those earnings.

- This view also highlights exposure to commodity markets and competition from larger and more automated peers as potential constraints on long term growth.

If either of these narratives reflects how you see Marex Group's future, it can be a useful anchor for your own assumptions on revenues, margins and the P/E you are comfortable paying at today's price.

Do you think there's more to the story for Marex Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.